Would like to caution investors on buying IndoCount at current levels. As a cyclical stock, you should not look at earnings in the rear view mirror but rather looking forward. Although it looks cheap compared to a cyclical high, this stock is trading at 2.7x book for a business that has frequently seen negative OPMs in the past, and thus is only a buy if you expect current margins to improve.

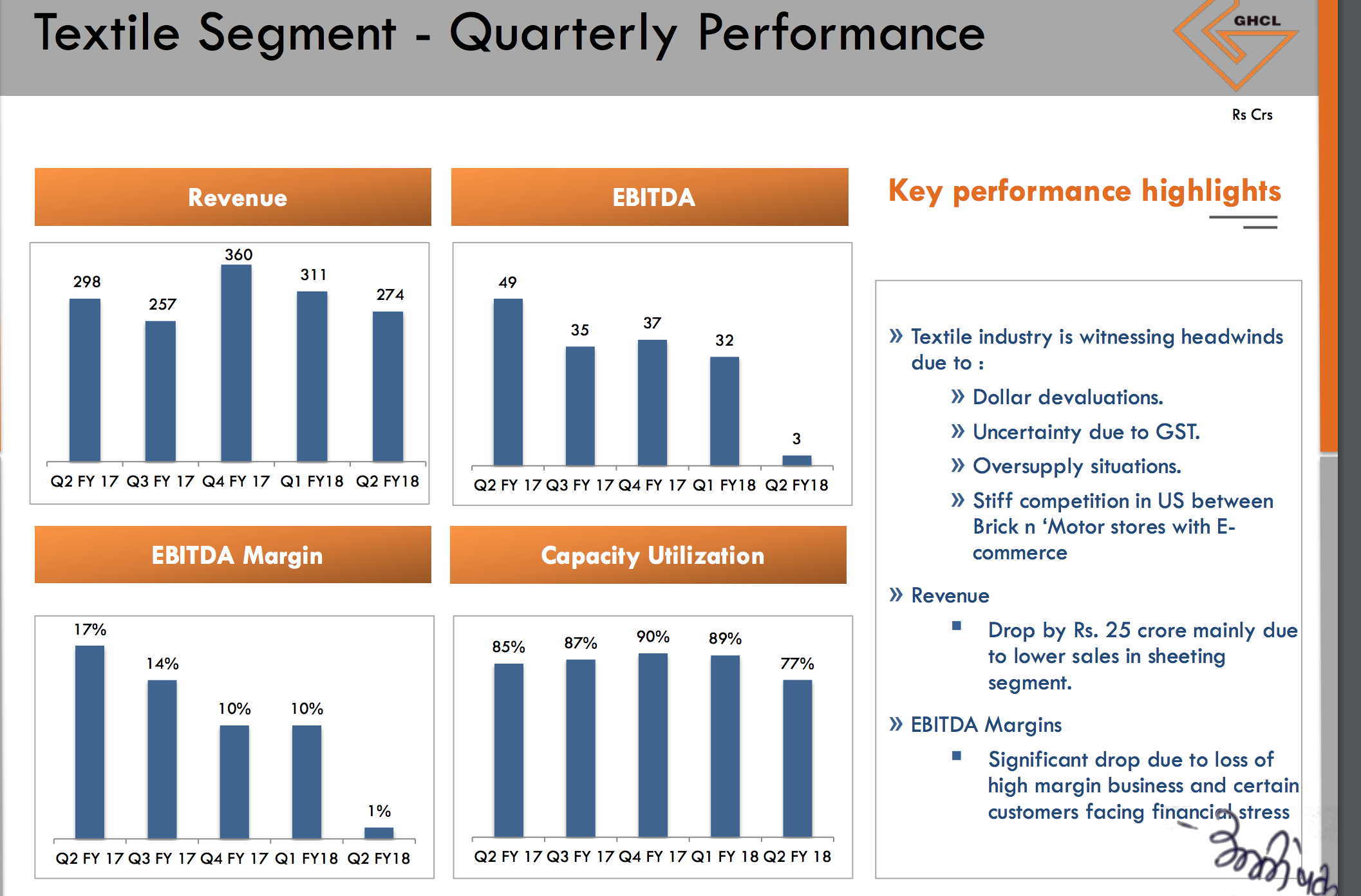

To track the cycle of the textlie cycle, we can look at GHCL’s earnings, which just came out. GHCL is very similar to ICIL in terms of its product mix (spinning and home textiles).

If you look at ICIL margins over the same time period (excluding Q2 results as they are yet to be seen), you will see that the drop in margins for both companies usually moves hand in hand. A look at GHCL Q2 concall confirms the hypothesis of 1) high oversupply in India 2) competition from China and 3) increased pressure from vendors due to their poor health.

Although there were some GHCL specific factors, most of it can be attributed to general industry conditions, and GHCL management does not see a revival for a couple of years, as is observed in most cycles. Thus there is a strong downside potential for this business to ~1-1.5x P/BV or even lower depending on how margins play out.

Disc. Short position on ICIL using futures/puts. May change anytime without updating post.

Indo Count turned around because of a change of business focus.

It is grossly inaccurate to call the home textile business ‘cyclical’ without clarifying what that means. Further, the comparison to GHCL is also not valid given that different business models and future prospects. The management of GHCL has confirmed that they do not intend to go into the brand label business.

To understand what is happening with the home textile sector we need to look at the fundamentals. Welspun and Trident (and even Indo Count) have not performed as bad as GHCL’s textile division which has apparently reported losses due to issues with a few customers. I strongly believe that the issues plaguing the home textile sector and still not clear (reported reasons do not hold up to scrutiny) and that Indo Count’s stock price has significantly over reacted vs. other players.

I’m very confused by this this statement. Q4FY17 and Q1FY18 margins for Indo Count and GHCL are similar (infact, GHCL has slightly higher margins as you can see from the photo above).

By cyclical, it simply means that too much supply has been added of subsitute goods (GHCL’s bedsheets v/s ICIL’s bedsheets), and thus given higher production, prices will have to decrease for market to absorb all the supply. No player has an established consumer brand in the US (I actually live here, and can confirm).

The textile market has clearly not been growing at the rate of these co.'s earnings, but rather that India has been gaining market share due to cost competitiveness and subsidies. However, the overall market has been fixed so when all these players have expanded capacity more than market demand, clearly theres going to be a price drop.

I don’t know why Trident/Welspun have shown good profits in recent quarters (might be a different sales mix) but apart from ICIL and GHCL, Vardhman Textile has also showed a dip in margins. I expect ICIL to mirror GHCL’s results broadly (I don’t see any counter factual to this data point), and detriorate in margins in Q2

I believe that ICIL’s FY2018Q1 operating margin is 15%, while GHCL’s textile division’s is less than half of that. My broad point was that GHCL reported a loss, while ICIL did not.

I understand a cyclical industry to be one that varies (directly or inversely) with the business cycle, and the home textile industry does not satisfy this criteria. My point is that there is a significant difference between commodity industry and a cyclical industry.

I highlighted ‘different business models and future prospects’ as a difference between GHCL and ICIL. This is clearly evident from a cursory analysis of the companies’ textile divisions. Equity valuations are forward looking, however uncertain the future may be, and the future of ICIL is to offer a portfolio of brands (like Welspun where a significant percent of sales 30%? or so comes from branded products). GHCL has no intention to do this.

@sarangg

Keeping in mind your points (which I agree to a large extent), I can understand that ICIL stock has dropped. However, aren’t you finding the valuations attractive ? The stock has almost reduced 50 percent from its high. I also consider that this has happened when the market has gone up quite nicely.

I don’t deny that ICIL can drop further in case markets correct by 10 percent from current level.

However, at the same time, I think around 100-110, this stock is good for adding in small quantities. It is quite possible if the company offers positive news (the management of ICIL always remains upbeat) in terms of actual performance, the stock could jump by 20 percent from current levels.

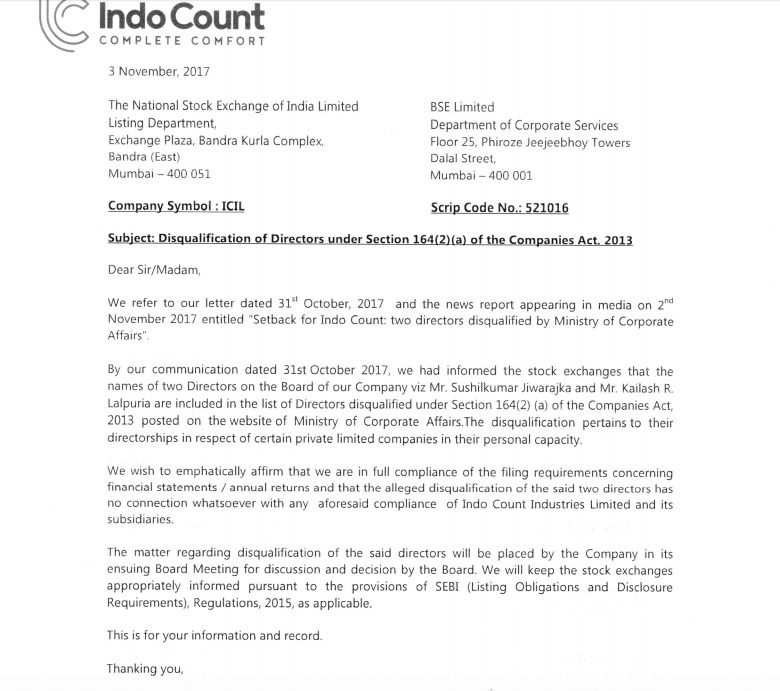

Section 164 (2) (a) of Companies Act 2013, enforced on 1 April 2014, allows for disqualifying directors of a company that hasn’t filed financial statements or annual returns for three consecutive fiscal years.

I couldn’t understand how they disqualified the directors under Section 164 (2)(a). Indo count is disclosing the financials and other reports every quarter. Anyways I will wait to hear it from the company.

Quite surprised. SEBI (or exchanges) did lot of damage to JKumar and many other companies few weeks back by adding them to list of Shell Companies. After that, they changed their decision those companies.

Now, blocking directors of Indo Count and not offering the correct reason for blocking them. Something very strange is going on with SEBI and Exchanges.

This is have a long term impact on valuation of IndoCount.

Why will it have a long term impact on the valuation of ICIL?

Lalpuria will still be employed by the company, and will still collect a salary. Unless I understand the situation wrong, he is just barred from being a Director on the Board of Directors. As such a BoD has little say in how a company is run, and is theoretically a shareholder sponsored body to monitor the goings on of the company. Given the lack of independence of Indian BoDs, this is all the more true.

I’m just curious to know how those investors arrived it ? Hope you know the Hawkins saga One of my friend told me about it few days back. Reminding here would be very much appropriate. Hatching on rumors is futile ! So lets wait for the results.

Textile companies have very low margins and are asset heavy, many evils stem from these weaknesses. As a minority investor it is self defeating to purposefully invest in such companies when there are so many options available.