I pay 18-24% while I take a credit card loan.Being a son of a financier myself I had seen loan sharks charging more than 60% at times.They charge such high rates coz it’s undocumented loan and it comes at a risk of not getting paid back.I think this is where microfinance companies come in.And a loan shark doesn’t disburse any loan in the middle a loan getting paid back,but MFIs do in the middle of d loan term too.I think good MFIs are gold mine for an investor ,especially after the AP fiasco.They had learnt the lesson and changed course.

4 Likes

Do you have any data to substantiate that significant % of loan receivers ( in 18-22% interest band) have historically defaulted on loan repayment in last 10 years?

Suru, my first request is I do not have interest in arguing.

second thing is please do not depend too much on data (of course,people here prefer data for everything).

Please understand the business model and how they operate. If you are still convinced, invest in MFI stocks.

Thank you.

3 Likes

Thanks for the link Vivek bhai… Pretty informative.

Thanks for sharing. Very interesting .

India Value Fund Advisors Managing Partner Mr. Vishal Nevatia on MFI and other sectors. Good interview.

2 Likes

Part 1 of the interview.

1 Like

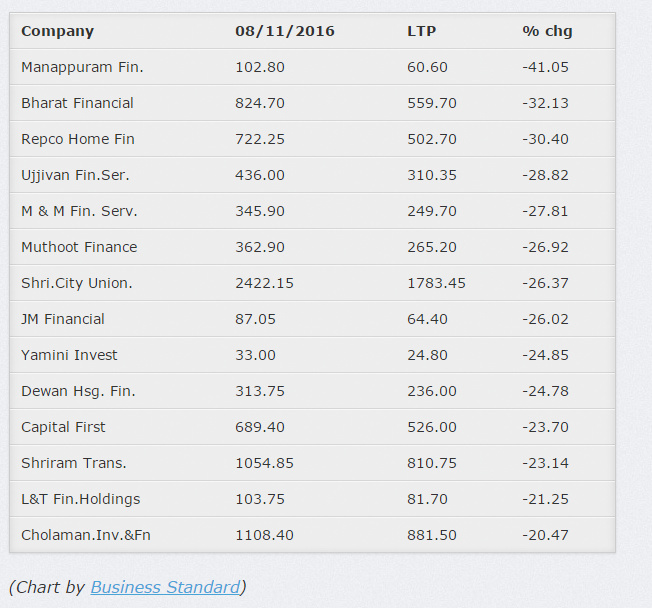

Above chart is outdated now. Current prices have increased. Please check.

I know…It was to showcase which MFI have been most impacted immediately post demonetization. It does not show current prices.

i differ on the view provided by you. I was an auditor of a small unlisted MFI which lend money to Mumbai based ( urban) low income people and Self Help Groups. From the excel data i was presented from their Information System ( Octopus MFI ) revealed some astonishing facts. While I was the same pessimist like you that these people would be less prompt than people who visit banks but strikingly the data was really low on defaults of payments of installments. Maybe the bet on rural MFIs would be different but what i could garner is that people who are illiterate and not into the formalized banking network would not necessarily mean they would default. I had verified loan documents and the purpose of 70% of the loans of MFI was business and was surprised with the prompt payments these marginal people would make on weekly or fortnightly basis. Though , yes you are right that frauds can easily happen and I myself came across some stray cases of flaws especially negligence in loan documents were presrent , but we as auditors ensured that such cases were highlighted to the senior management . Provisioning in MFI is quintessential and also checking of loan documents. A good and ethical management + ethical auditors might make NBFCs a better investment opportunity thank Banks

16 Likes

Looks like BFIN will get acquired by IIB. Rumors seem to be getting stronger. Just wondering what this means for the sector. Also could this mean an end to the concept of “microfinance institutions”. Will the responsibility of lending in rural areas be taken over by banks (conventional and SFBs)? Views invited please.

Is this good decision by govt going to affect MFIs in the long run? http://economictimes.indiatimes.com/news/economy/policy/government-planning-an-easy-credit-scheme-for-rural-households/articleshow/58250161.cms

''The aim is to reduce their dependence on local moneylenders and microfinance companies who charge usurious interest rates as against 11 per cent by banks. ‘’

I have the following points to say in relation to the news

- Looks like the idea is being muted by Ministry of Rural Development.

- I will like to imagine that idea has not been vetted by Ministry of Finance.

- I would think that there are people in GoI executive & RBI who know that idea of Microfinance had been thoroughly discussed, debated and tested all around the World & a noble prize in economics was awarded just because it is only/best way to provide credit to poor.

- This will be sub-prime lending by GoI.

- I will argue that it will be impossible for GoI to recover this money because of political reasons and the size of infrastructure needed to process such amount of loans.

- The memory of sub-prime crisis in USA are still fresh and we may be looking at our own if this goes through.

- The amount talked about in the article in very big 8.5 L cr. If this goes through it could be very bad for whole economy not only microfinance sector.

5 Likes

Nothing impossible for Modiji as his prime objective is to strengthen rural and poor people. He will squeeze MFI charging higher interest rate.

He did in drug and medical device price control.

मेडिकल के क्षेत्र कैसे हो सकता है बेहतर, बताया नरेंद्र मोदी ने

http://bz.dhunt.in/2cTTl?s=a&ss=pd

via Dailyhunt

Other side to look at it would be that rural economy and consumption might get a boost and that inturn might help the economy. The amount would be 60000Cr /yr as said in the article.

1 Like

And once they start taking loan and enhance their living standard, taking credit will be part of their life! Govt may help creat a habit, others may reap benefit for life!

The above article is quite interesting. It talks about the two fundamental events that have impacted main players in the sector:

- Demonitization

- UP loan waiver

a. Many value investors like Shyam Shekhar, Samir Arora, etc. Are very sceptical about the business model due to the recent events.

b. Recent results of major players like Bharat Financials and Ujjivan is not encouraging

c. Long term trends like digitalisation can act as a disruptive force as banks will understand the consumer behaviour better and improve their reach to customers

It would be good if some knowledgable members can discuss more risk apart from political risk for the sector.

They say they do not give loan to farmers and check credentials so what happened? It is all about herd behaviour. They take loan in herd by watching their uncle, aunt and neighbours etc and default together. we have talked about political interference which comes at village level too. One influential guy(mukhia etc) can create enough trouble for the whole village/area. Those who can afford also default happily and these days no one can take coercive action. Whole MFI biz is like the concept of unstable equilibrium where one push is enough to create havoc. They will recover from this crisis for sure but not faraway from another one.

2 Likes

from an article quoted in this thread

“If there is a sharp growth in lending amounts, and no concurrent growth

in the physical outreach of branches and employees, then it is most

likely that the credit checks of identity, pipelining and utilisation

may be short-changed.”

Any one tracking growth in lending vs growth in staff among different MFI/MFI-SFCs for thew past 2-3 years?

Disc: invested in Satin and Ujjivan 3-4%