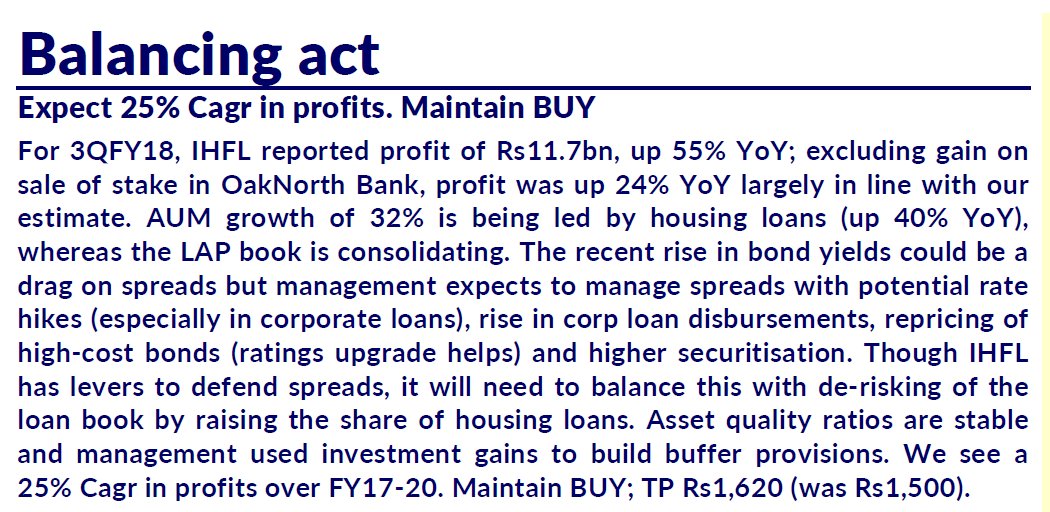

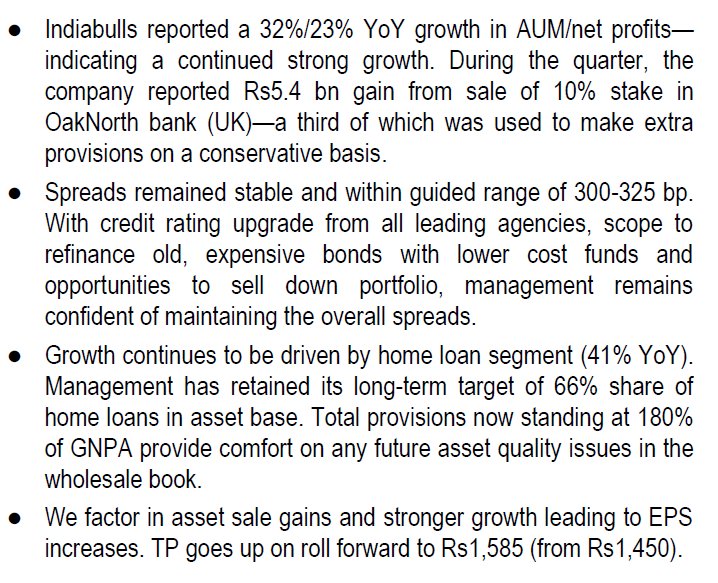

Only other company to have shown an impressive sales performance for the quarter after PNB HF at 24% on an Year on year comparison. Other companies had an improvement in bottom line but the sales growth was only around 12% such as Dewan, Gruh and CanFin Homes.

CLSA on Indiabulls Housing Finance

Maintain buy and increase target price to 1620 from 1500

See 25% CAGR in profits over FY17-20.

Rs 32.46 cr Block Trade: NSE :

Indiabulls Housing for ~232000 shares, at Rs 1399

Yesterday👆

Some important points from Q3FY18 concall about the business going forward. Most important takeaway for me …as to why they will probably be able to maintain their spreads despite rising interest rate scenario. Along with, i was also curious whether banks due to the lowest cost of funds might probably take away this lucrative housing pie gradually away from NBFCs. Management answered these questions in a very lucid way to allay these fears.

I think this company is best placed among its peers to exploit the housing/lap/construction finance opportunity in NBFC/Banking space.

Few salient points

-

For 32 quarters now, we have been compounding profits between 20% and 25%.

-

Post stake sale, Indiabulls will continue to hold the stake of 20% in the UK Bank and will remain as the single largest shareholder with two nominees on the board. Valued 1500 cr.

-

Used one-third of the stake sale gains and created an additional provision of Rs. 180 cr as a countercyclical provision.

-

GNPA and NNPA were down to 77 bps and 31 bps respectively from 85 bps and 36 bps same time last year. In computing NNPA, only provisions against substandard assets are deducted. Standard asset provisions and counter cyclical provisions are not deducted while computing net NPA.

-

In Q3FY18 we have disbursed a total of Rs. 12275 cr, a growth of 35% over last year same quarter in which we have disbursed Rs. 9098 cr. The disbursals break into Rs. 7090 cr of home loans, Rs. 2040 cr of LAP and Rs. 3150 cr of corporate mortgage loans. So on an incremental basis we would be getting roughly 8.9% on home loan; around 11% on LAP; just under 10% on LRD; and around 15% on construction finance. So overall, we will be getting roughly about 10.3%.

-

Asset yields will either stabilize or start going up if the bond markets are not to cool off.

-

CAR is at 21.35%.

Floating lending/asset base

We are floating rate lenders, so a large portion of our borrowings also has to be floating rate apart from let us say a year or two, we cannot take a longer-term call on interest rates and therefore we have to necessarily swap it out. The flexibility that one enjoys today is that our lenders cut across bank’s mutual funds, insurance companies provident funds, FPIs, etc., and each of the sources of money have been gaining in size besides banks. So while we are getting the benefit of an upgrade of our credit ratings, we were also in parallel diversifying.

On the asset side also, rather than become a single product company, we have been harping on for years that we would want to maintain spreads at 300 bps and therefore we will never become a 90% home loan company. We will stop at 66%. So, the big point being that flexibility is critical and we do not wish to go anywhere close to losing or closing out the variable liability side pricing opportunity.

Cost of funds and spreads going forward

- All of the four leading rating agencies in India rate IBHFL at the highest long-term credit rating of AAA. IBHFL is also only the second private non-bank lender on standalone strength to have received a credit rating of AAA by CRISIL.

- Corporate and sovereign yields have gone up by 45-50 basis points from mid-2017 levels. However, specific to IBHFL, due to the rating upgrades, lower bond pricing for fresh issuances combined with re-finance of stock of earlier issued bonds, this rating upgrade has enabled us to offset most of this macro rise in rates. Alongwith, our diversified liabilities profile accords us flexibility and provides us multiple options to efficiently manage our cost of funds.

- Due to stronger INR, We have been able to borrow foreign currency loans on a fully hedged basis from local banks almost at par or lower than bonds.

- Banks have had reduced their MCLR by 10-15 basis points last quarter which has been fully transmitted to us and that also helped us manage our cost of funds.

- Re-financing of ECB loans on maturity at lower cost is helping us bring down the cost of funds on our stock of borrowings.

- Further, portfolio securitization continues to remain strong and the large requirements for pools from banks in Q4 will have a favorable impact on the cost of funds as it did in Q3.

- We should be able to continue to maintain our spreads between 300-325 bps even in a rising interest rate scenario. Overall incremental spreads has come up to 280 bps, so it is very much within the guided range of 275-300 bps. In an increasing interest rate environment, we will definitely be increasing our cost of funds at a pace much-much slower to our peers. Our incremental cost of borrowing are still much lower than the stock of borrowings. So even in rising interest rate environment, our cost of funds will continue to decline. And thus, we should be able to maintain our spreads. This will happen as we refinance bonds on maturity gradually (18-24 months).

- Spreads we are reporting would have come down in a stable interest rate scenario. This is quite counter intuitive but generally speaking, in a rising interest rate environment in the first 6-12 months, lenders in the current structure that Indian interest rates operate in and the way that they get transmitted actually make more money. Our bond funding costs (yields we offer to lenders) will continue to be flattish for a period of time on a stock basis because our incremental costs are still lower. So just to put some numbers in perspective, our stock of borrowings was 792 bps; as on 23rd of January our incremental cost was 765 bps. So as of 31st of March, our stock of borrowings would have actually reduced. And in all probability, MCLRs for banks would have gone up.

- At least for the next 18-24 months, irrespective of what happens to interest rate, we will either be going lower in a flattish or growing slower on our cost in a rising interest rate environment. We stay confident to continue to grow earnings between 20%-25% in fiscal 2018 and further up until fiscal 2020. The affordable housing opportunity is a multi-decade opportunity and it presents a very-very unique proposition of Indiabulls first getting to Rs. 2 trillion by FY20 and then getting to at least two times to three times of that size over the next four years to five years.

Securitisation resulting in higher ROEs and lower BS risk

- We continue to remain keenly focused on capital conservation and sold down as much as Rs. 7620 cr of loan assets in 9MFY18 compared to Rs. 4200 cr in the whole of last year.

- Selling down loan assets is an extremely capital efficient structure and it also helps us maximize our ROE.

- In the fourth quarter, it will also be a huge enabler in bringing down our bond yields since we have a big stock of what qualifies for bank as priority sector loans, which becomes a very desired commodity in the fourth quarter.

- Plans are to securitize 35% of the loan book for FY18. (incrementally). Priority sector asset securitization is very beneficial as the investor gets lower yields on the same but has to buy as they have to attain their targets in priority sector lending.

Why banks are not competitive in exploiting housing finance pie despite lowest cost of funds

Home loan rates have not gone up till now but some HFCs have already raised the prime lending rate for their commercial portfolio. Banks are not making some killer kind of returns in even the core home loan business. With their cost-to-income ratio, whatever gains they have on cost of funds gets offset in a flattish interest rate regime. They make about one-third of the spreads or the ROA that housing finance company with a AAA rating and with good cost-to-income ratio makes. Maybe in a rising interest rate scenario, that one-third will get reduce to half of the ROA that we are making. But they would still continue to be at a disadvantage, which is why you do not see the midsized private banks - which otherwise are gaining massive share on the corporate side and are also gaining almost growing their retail books in triple digit - are not venturing into home loans.

So given this entire macro and our discussions around where home loan yields are, if government securities continue to be in the handle of 7.5%, sooner than later you will see transmission across the board, across home loans, LAP as well as corporate loan.

Impact of RERA on construction finance

In construction finance the competitive environment from banks is very-very benign. The likes of SBI have gaps around commercial real estate, so they cannot really build even double-digit on percentage basis exposures to commercial real estate. RERA from a construction finance structure does not make it more or less bankable. A typical construction finance structure was anyways tighter than what the RERA guideline allows. The other impact of RERA is that land would not be transacted anymore. There would be more JV models. Though JV models require a certain sense of understanding of how to create security, which is not really the forte of banks. Banks are extremely good at doing standard kind of stuff. Here you have to take the land as security, take development rights as security, pledge the shares and all of that. So this is actually a blessing for housing finance companies given the specialization that they have. There is no concentration risk in this segment.

PMAY scheme

Started pushing the scheme from September-October onwards and it is gaining good traction.

Disc - Invested. Not a buy/sell recommendation. Please do your own due diligence.

10 Likes

I just checked the yields for some years back there were as high as 9% sometime in 2013 and 8% most of the times in 2012 to 2014…even in those periods HFC’s has done well…I have a basic question will the cost of borrowing wont be more? if yes they will pass to consumer by raising the home loans rates? I still think india urbanization will be on a rapid rise…so wont be all the HFC’s will be in multi year bull run? please share your views

P.S…Invested heavily in Indiabulls HSG and DHFL

Please check my last post again. You will have your answer. In gist…they have diversified there asset pf in order to maintain higher spreads and nim. Companies in plain vanila housing finance might not be able to compete and preserve their margins once interest rate cycle reverses and competition intensifies. That’s why they said they will stop housing finance at 66% of pf.

Second, cost of borrowing if increases… is for everyone. So lending rates will increase as well across board.

My point staying with larger players is that there cost of borrowing is among the cheapest. And with focus on e-lending, cost to income is improving significantly. So, going fwd, despite interest rates increasing, they will be able to preserve their spreads, margins and return ratios in an increasingly competitive environment.

Moreover lap and construction finance are considered risky domains; indiabulls specializes. Inn these due to it’s superior relationship with tier 1 builders. So going fwd, i believe bigger companies with domain expertise will exploit the pie much better and with longetivity. Dhfl is okay, but overall i like indiabulls due to it being much more tech savvy and better return ratios and npa, and div yield.

4 Likes

Huge Positive news i think for all NBFC…this will ease further pressure on bond yields  )

)

Intern Divided 10 declared ex date is May 2nd

2 Likes

Some key points from Q4 FY18 concall. Mostly on the business side (left numbers)

We have already bought down the cost-income ratio from 21% to 12.5% and this will continue to decline to a single digit over the next couple of years.

Driven by increasing share of home loans, the ratio of risk weighted assets to loan book is up to 78% at the end of fiscal ‟18 from 86% last year. Risk weighted assets to loan book is a strong indicator of risk being underwritten and declining ratio is also indicator of frugal capital utilization.

Another big positive for the year was that we crossed the landmark of selling over Rs 100 billion of loan assets to banks. This was the highest ever sell-down recorded for a financial year by Indiabulls Housing. We are focused on capital conservation and selling down loan assets is extremely capital efficient, freeing up capital while retaining spreads, making the transaction highly ROE accretive. We have gotten to 30% ROE – Thanks to an active sell-down strategy. As we move towards fiscal 2020, portfolio sell-down will contribute to an increasingly larger proportion of a funding mix, and from the current 10-11% we hope to see that rising to almost 20% level.

We have increased rates effective from 1st April 2018. Our PLR has increased by 20 basis points for Home Loans. WIll maintain guided range of 300-325 basis points.

We have effectively proven yet again that we continue to be a transmission vehicle with the ability to almost immediately pass on any rise in our input cost of funds. There was much concern last quarter on how our loan spreads will hold up with the upward movement of interest rates. I had made the point that even with appreciable height in interest rates due to tailwinds from our upgrade, rating for our incremental funding cost will be lower than the funding cost from the stock of borrowing. True to this, our cost of funds for Q4 on stock of borrowings was down by 17 bps to 7.75%, the yield on our stock of loans was at 10.86% resulting in a spread of 311 bps.

We

made considerable investments in IT and are now well underway to launch a comprehensive Indiabulls Integrated Home Loan Technology Platform in fiscal ‟19. Various modules of this platform will go live from Q2 fiscal ‟19 onwards. A few clear financial outcome that we target through this technology initiatives are, long-term sustained loan book growth of around 25%, enhanced fee generation to 2% level from 1.6%, operating efficiencies resulting in cost-income ratio going to single digits, reducing our credit cost to under 50 basis points.

Our balance sheet and loan book will compound at 25% going past first Rs.2 trillion by fiscal ‟20 and then double from there to Rs.4 trillion by fiscal ‟23. Our earnings should compound at over 22% growing to Rs.55 billion by fiscal ‟20 and then Rs.100 billion by fiscal ‟23. Our target for cost-income is sub-10% in fiscal ‟20 and 8% by fiscal ‟23. Annualized credit cost should slip to 50 bps by fiscal ‟23.

There is reasonable commission fee on LAP and commercial loans. They also earn insurance commission on their sales, which helps them with delinquencies (risk management exercise) as well when something wrong happens to the borrower.

Tax rate - 25-26% going forward

95% of the construction finance portfolio comes from top 6 cities. Average ticket size will be ~200-300 cr (sanctioned amount, disbursed could be lower). Did 60 loans this year (50 done last year).

Write-downs average rate - 7.5%. FY19 will be very strong from the perspective of priority sector write downs as guidelines have changed for foreign banks.

Banks are completely absent from construction financing segment. Spreads here should improve going forward.

Anytime over the next 18-months they will raise capital. Between 7x-8x gearing.

4 Likes

@Mridul can you pls help me understand how IBHF calculates their NII? I was trying to calculate using what they have published in their Financial statements but it doesn’t match with the figures they have presented in their investor presentation.

Do they include fee income in their NII?

Do they include a part of their Other Income as well?

My limited understanding is that NII shd only include the interest they earn on their stock of loans - the interest they pay on their borrowings. Is there more nuance to how NII she be calculated?

I would very much appreciate a bit of help ion this from anyone in the know.

Fee income is counted as other income

Please put down your calculations here.

It has become cheaper than DHFL atleast on a PE side…there has been continous selling in this after the results…i dont see the results were bad…any comments from other boarders appreciated

1200 is crucial support. If this is not broken on volume basis, we can then deduce that current weakness would be periodic consolidation which is normal. 1175-1200 is the key levels to watch out for. Also acknowledge that their has been good delivery percentage at these levels.

1 Like

Would be great if anyone who did sufficient research on IBHFL can update on what are the risks involved and what is keeping it available at a good PE even with good results and good dividend.

I read this: https://www.livemint.com/Companies/H4eR9HViNHwir9Va1ZyjTL/NCLT-reserves-order-on-Indiabulls-insolvency-plea-against-S.html

but don’t think this is such a big issue.

Informative speech by Gagan Banga Vice Chairman, MD and CEO of IBHFC on the future of HFCs in general and his company in particular.

2 Likes

Companies in housing are valued by their book value I think. That’s because the quality of earnings are directly dependent on how good their loan book is.

If there are higher NPAs, more provisions will need to be created, eroding the book value and bringing P/B ratio down subsequently.

PE ratios are insignificant.

1 Like