Guys let’s not post block deal data here. @Administrator please take notice.

This data is available on exchanges for anyone to see. moreover, remember for every buyer there is a seller so a block deal does not mean much unless there is a fresh issue of capital or an insider is taking one side of the trade.

Indiabulls Real Estate arm gets Rs 701 cr refund from DDA

Indiabulls Real Estate today said that its subsidiary firm has received Rs 701 crore refund from the Delhi Development Authority (DDA) following a judgement from the Supreme Court of India.

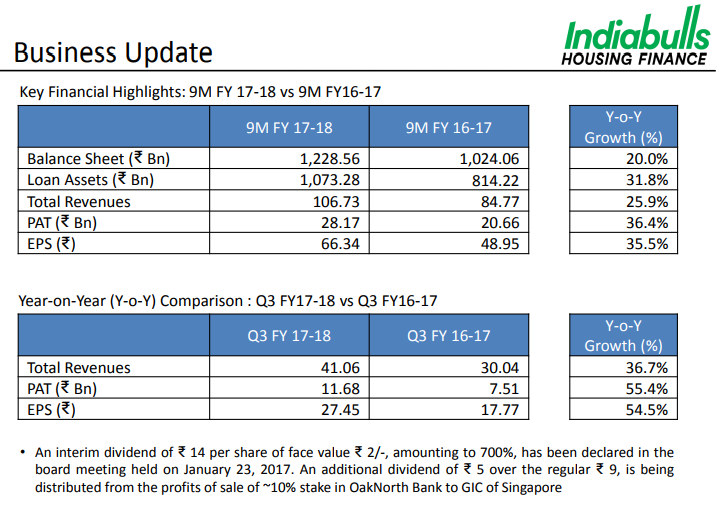

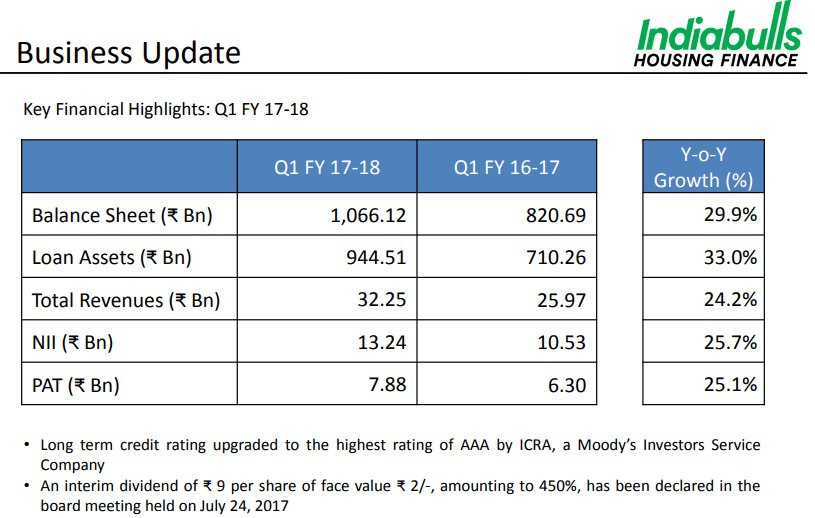

Indiabulls net jumps 25% to Rs 751cr as loan-book grows 30%

Indiabulls Housing Finance today reported a 25 percent rise in net profit at Rs 751 crore for the December quarter and said it has not been affected by the note-ban at all.

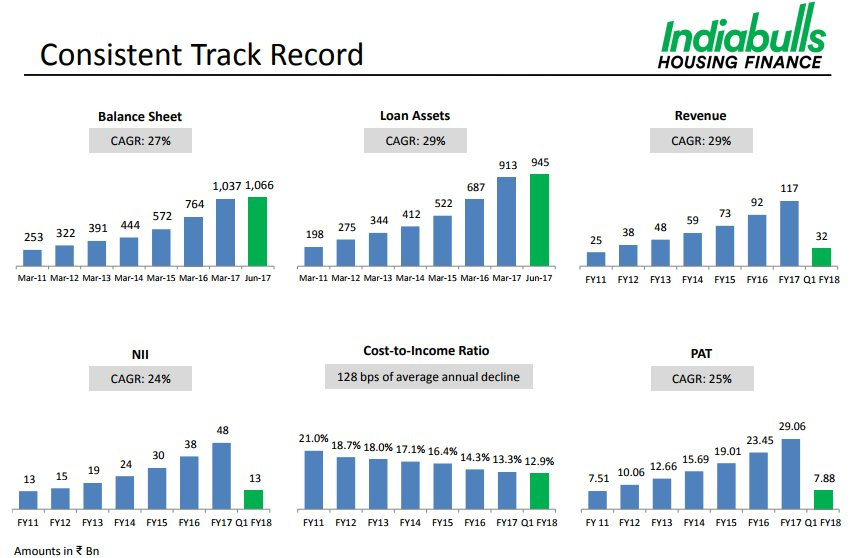

The leading standalone mortgage player also crossed the Rs 1 trillion balance sheet milestone during the quarter on the back of a healthy loan book growth of 30 percent.

“Our loan book clipped at 30 percent, driven primarily by the affordable housing sector loans, registering a net growth of a little above Rs 6,000 crore during the quarter as we did not see any impact of the note ban which dominated most of the reporting period,” company Vice-Chairman and Managing Director Gagan Banga told PTI in a concall.

This is in sharp contrast to the banking sector which saw a massive contraction in their lending business following the note ban. According to Crisil data, while public sector banks saw their loan book shrinking by a negative 15 percent, their private sector peers saw this at a negative 11 percent.

He said the company has crossed the Rs 1-trillion balance sheet milestone during the quarter at Rs 1,02,406 crore and expressed the hope they will be able to better the Q3 showing in the March quarter by an incremental loan growth of Rs 10,000 crore.

In the December quarter, disbursals rose by Rs 9,000 crore, Banga said, adding they have set a target of crossing the Rs 1.5-trillion milestone by 2018-19.

“We plan to add at least Rs 25,000 crore incrementally to our balancesheet annually over in next two years.” Describing the December quarter profit as the highest ever at Rs 751 crore, which was up 24.7 percent, Banga said this was boosted by a 30 percent growth in the net interest income at Rs 1,261

crore.

Profitability was also helped by a fall in the cost- to-income which dropped to 13.8 percent from 14.3 percent, while the credit cost remained stable at 74 bps of loan assets, which is within the guided

range of 70-80 bps for the full year.

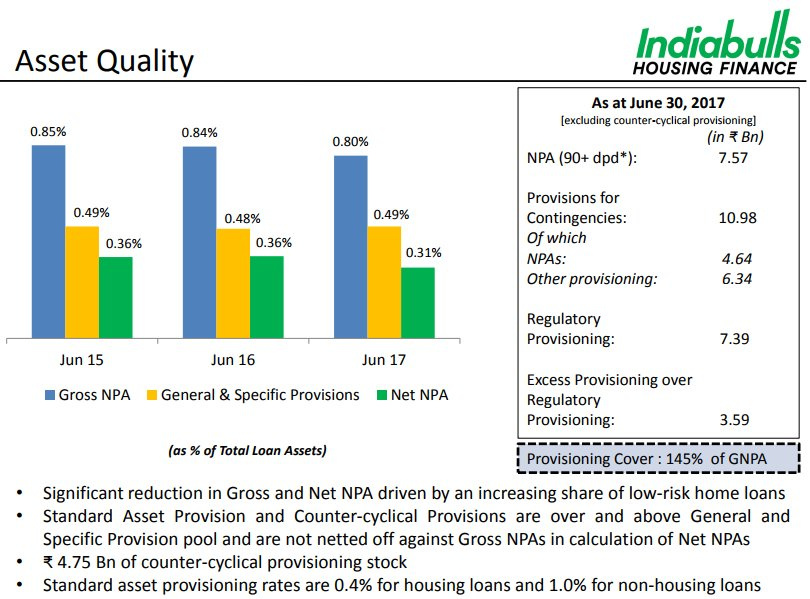

Despite challenging market conditions, the company could maintain stable asset quality as its gross NPA and net NPA stood stable at 0.85 percent and 0.36 percent respectively during the quarter.

Historically, most of the bad loans for the company has been coming in from commercial property side, which was the case in the reporting quarter as well, he said.

Almost 60 percent of the loan book is retail home loans, and the rest is equally spilt between loan against property (LPA) and commercial properties, Banga said.

Excellent results despite demonetization in last quarter!!!

Wondering what else would it take for it to close the valuation gap with Gruh and CanFin. Both are smaller in size vs IBulHsgFin. Is market expecting even faster growth from Gruh and CanFin? I hope not.

With solid dividend yield of ~5% and consistent growth in business maintaining NPA numbers in reasonable range - it should trade at higher P/B multiple from current levels.

Disclosure: invested since last 2.5 years.

1 Like

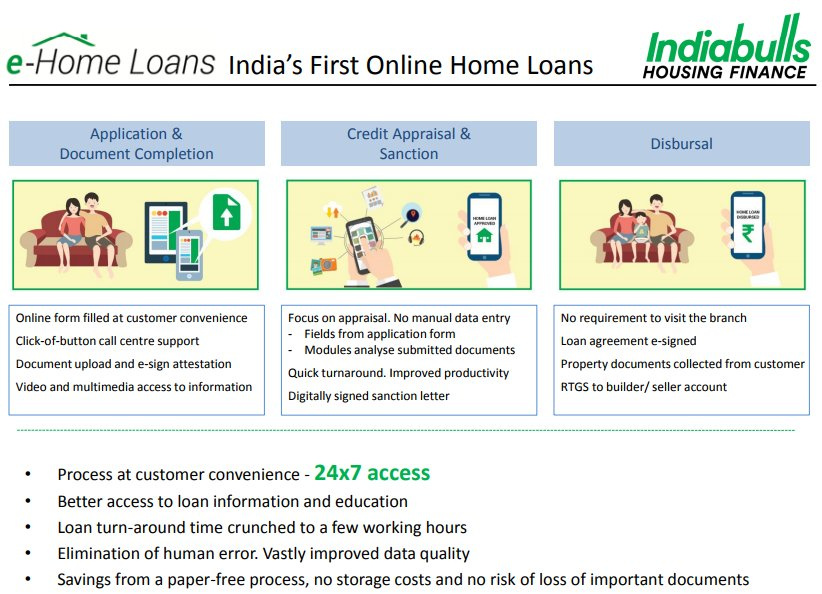

Excellent results. They have uploaded a nice presentation on BSE and it seems they are already ahead of it’s competitors in terms of technology usage.

Is it odd that nobody is mentioning the 40% stake they bought in Oaknorth - a UK bank - for 663 Cr

The bank’s pre-money BV was USD 31 M, and IBHFL invested USD 100 m

Interestingly, the investment was found and approved by a committee headed by KC Chakraborty - one of IBHFL’s independent directors.

The story is: it’s an SME focused bank and IB’s LAP expertise can help it grow.

2 other banks’ cases studies were furnished in the presentation - to talk of how the road to greater value will be achieved.

IndiabullsHousingFinanceLimited.pdf (1.0 MB)

Question is: Why did they buy into a bank in the UK?

Also, they bought this stake a month after the 4000 Cr QIP ended.

According to the co-founder’s profile, the bank has broken even from Sept 2016. Rishi Khosla - Wikipedia

and in September 2016, announced that it had broken even, becoming the

first completely new bank in the UK to achieve this in under a year.

It’s seem to be a investment made to diversify the Indiabulls portfolio.

Mr. Gehlaut said that he will be investing in this company from his personal capacity also. Indiabulls Housing declines 17% on OakNorth Bank deal | Mint

“Sameer Gehlaut, chairman of the company, will be investing in his

persona| capacity up to 10% stake in OakNorth Bank at the same

valuation,” the statement added.

It will be interesting to check if he did that or not.

They bought the bank to strengthen their case to become a deposit taking NBFC in India as they perceive deposits to be a stable and cheap source of funding for their core home finance business. Looks like a long short to me. Their funding costs are going down anyway.

2 Likes

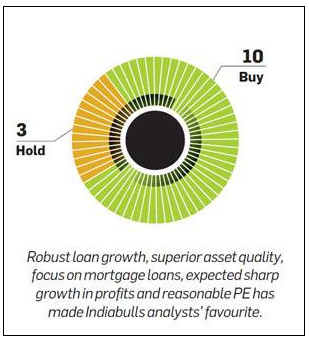

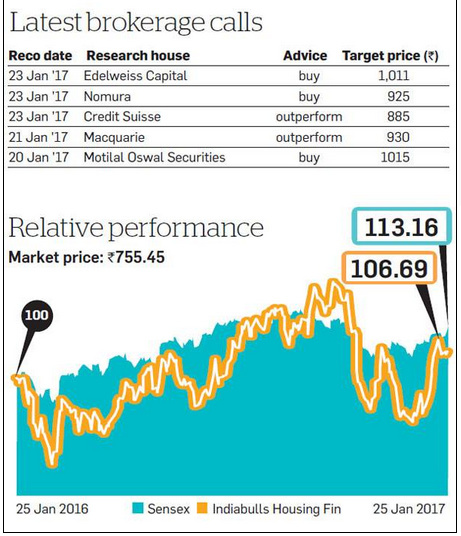

Stock pick of the week: Why analysts are bullish on Indiabulls Housing Finance

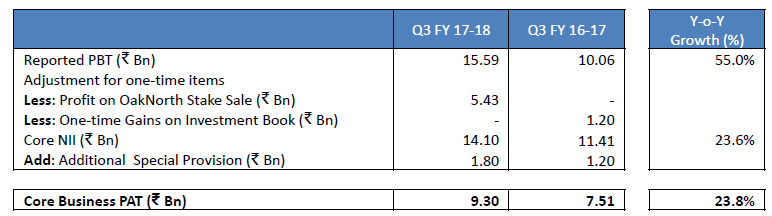

Despite demonetisation blues, Indiabulls Housing Finance was able to maintain its high growth momentum in the third quarter of 2016-17 as well. Though there was some disturbance in its loan growth immediately after demonetisation, the company bounced back sharply within a few days and was able to report a 31% loan growth compared to the same period last year. Fall in funding cost, triggered by demonetisation, helped Indiabulls Housing improve its spread. And, with a net profit growth of 25% year on year, Indiabulls Housing has beaten the Street expectations by a wide margin.

The company has been able to maintain a high growth because of its focus on the fast-growing affordable housing segment. Analysts are hopeful that Indiabulls Housing will be able to maintain this growth momentum in the coming years as well. This is because government initiatives such as ‘housing for all’, additional tax sops for the affordable housing segment, etc., are boosting the affordable housing segment, etc., are boosting the affordable housing segment and increasing financing opportunity for companies like Indiabulls Housing.

There was also a fear that housing finance companies’ asset quality would deteriorate due to demonetisation, but Indiabulls Housing came out unscathed and was able to maintain its high asset quality: Gross non-performing assets (NPA) of 0.85% and net NPA of 0.36% (as of December 2016). Since the management continues to give high importance to asset quality, it may remain strong in the coming years. To maintain its high asset quality, the company wants to increase the mortgage loan share to 65% from the current 55% by 2019-20 and bring down loan against property (LAP) and developer loans share. This focus is visible in its third quarter numbers: While mortgage loans grew 35%, LAP and developer loans grew at a slower pace of 23%.

2 Likes

Presentation of the company looks very interesting…

The way they are using Technology for cost benefit is really good. But Bajaj Finserv and many other companies are doing similar. Then do they have an edge on others.

Indiabulls Housing Finance Q4 2017 Earnings Conference Call Presentation…

Reasonably confident that the home loan book will continue to grow at 30-35 percent

Indiabulls Housing Finance aiming for over 30% loan book growth: Gagan Banga

the company has been able to maintain their GNPAs at 85 basis points for the last three year and as of now, there is no concern on existing books, said Gagan Banga, VC & MD, Indiabulls Housing Finance.

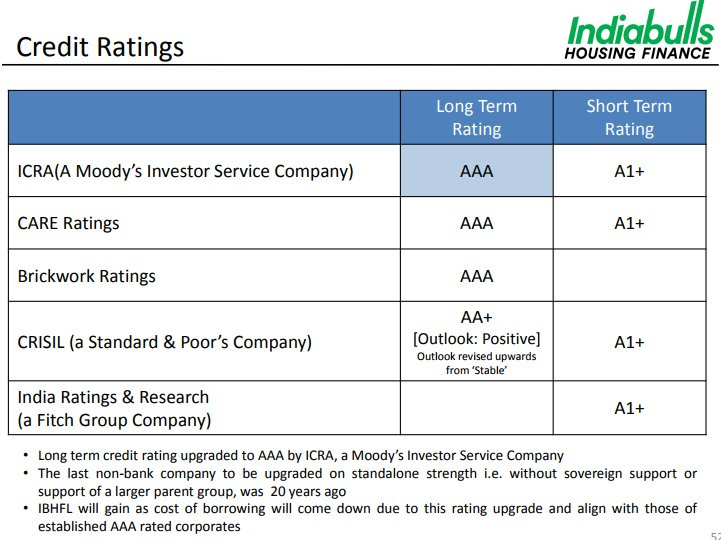

Company has got the highest possible credit rating now it can raise funds at NBFC rate4ff34561-4a62-4465-ab21-6b4637014350.pdf (349.9 KB)

Interesting article on outlook of Housing Finance as a sector -

Key point - "Jefferies has made a case for higher pressure on spreads of HFCs, with the likely bottoming out of bond yields. Spreads of most HFCs have been generally inversely correlated to bond yields. HFCs had benefited from falling bond yields in the last few years. Bond yields have now rebounded nearly 60 basis points from the recent lows in September to cross 7.1 percent levels on increasing concerns surrounding fiscal slippage and supply of paper, which means little or no scope for further reduction in funding costs of HFCs with higher share of borrowings from NCDs. If bond yields rise, HFCs with shorter duration liabilities or higher mix of NCD funding could see greater pressure on spreads.

Another reason is competition from PSU banks due to recapitalization."

1 Like