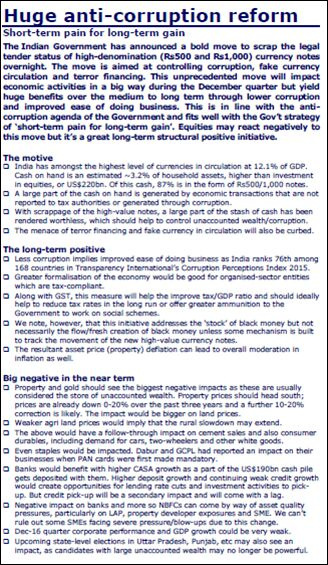

Are we going to see a big red Wednesday after the PM’s surgical strike on Rs 500/1000 bills…

Who cares? Good for India, good for economy, good for people. Everyone should celebrate this bold and historic decision.

7 Likes

Yes agreed. It is definitely a historic decision. However it may impact the sales, though for just few days or weeks, of the companies in B2C segment. However in long run, it will boost the organized sector…though real estate and jewellery stocks may be dumped for medium to long run

Will Modi s next target be gold? As lot if people hoard gold instead of cash?

Some possibilities:

- Real estate prices might come down and have a positive effect on housing for all

- Modi has been opening up bank accounts for everyone, this seems to be falling in place now and people might start using these accounts in a more serious sense

- UP elections can get interesting as money distribution is not going to be easy

- Income tax getting slashed in the next budget

4 Likes

in the long term this is a welcome step. more white money, affordable housing , more mutual fund inflows. also more finacial inclusion means more work for banks and nbfc.

will have to wait and watch how manappuram and other gold loan companies respnd to this. this move may affect the purchase of gold to a large extent and hence the way gold loan nbfcs function

High Interest rates could be history. The question could be how much lower we may go. Sub 5%?

Companies running with high leverage (especially Banks, NBFCs) might be gainers. Financial services investing in equity markets may be gainers in long term as people move away from real estate and gold. Tax rates may reduce leading to more consumption by tax payers.

1 Like

Right now its looking very bleak. Can some mature investor sooth the nerves.

My view wrt 500,1000 notes’ ban and potential trump win:

real estate is out.

gold is a hedge against inflation. It is going to be neutral.

Interest rates will be down due to low inflation.

Indian debt and equities are the best. Keep holding. Stocks will come back.

I have 50% cash which i will be looking to deploy.

2 Likes

It will be good to know analyst thought process on NBFCs and MFIs.

NBFC, MFI are good. I have issues buying for more than 3-4 times book value but till 3-4 times book value, they look good (have bought Arman fin. Today as well).

Housing finance companies and other housing related stocks got hit disproportionately yesterday due to expected fall in real estate prices.

In the long run lower prices and better transparency should be good for the sector. In a recent survey by Mint, most people would buy a real estate if the prices drop by 10%. This indicates that demand for loans will increase with a modest drop in prices. Moreover, a 10% drop isn’t enough for the borrower to default on their loans as loan to value ratio is usually less at 75% at origination and drop from there. In most cases borrowers default on their loan when they lose their job or business income and not because their property lost value. Even developer loans will be performing if demand for housing go up.

Disc: Invested in Indiabulls Housing, PNB Housing

3 Likes

There are definitely negative impact on real estate and jewellery stocks in short term.

But long term effects seems to be good.

Further reduction in interest rates , lower prices in real estate , will spur demand and

If the developer will reduce the efforts of making black money as now. Then all the profit will be reflected in balance sheet , more money for share holders.

Gold and jewellery businessman have earned a lot in this two days and same should get reflected in the dec’16 quarter.

1 Like

On Demand Side:

Most of the customers for housing finance companies like HDFC and Can Fin are salaried. So there is no issue of Black Money there.

For Gruh and Repco, the customers are in the low income category. So there is no issue of black money there as well.

On Supply Side:

We think that most small builders thrive on black money from few customers and that’s how supply is created. But if there is strong demand from people who buy property with white then supply will come in automatically.

After all, we learn from the developed markets. The housing sector in USA is still thriving even after so many years of growth and there is no black money involved.

This step of demonetization will provide great opportunity to buy some great companies.

3 Likes

If we talk about liquidity for banks, since its going to take a while for the new notes to be in full circulation and not everyone is going to perform electronic transactions, banks are going to be flush with liquidity for some time.

News reports have stated that till Saturday banks have received worth $30 billion in deposits!! Here is one such report. http://www.bloomberg.com/news/articles/2016-11-12/india-s-largest-bank-gets-7-billion-in-deposits-as-atms-run-dry

I think as a result we are going to see a drop in interest rates across asset classes. This should be a good news for NBFCs which borrow from banks.

Critical comments on this are welcome.

2 Likes

Any listed companies which will benefit due t o increase in cashless transactions.

The key question is if this currency move is a demonetization or just a currency replacement? Prima-facie it appears to be a currency replacement as old notes are replaced with newer and high value notes.

86% of money is gone. If all of this is replaced then it will be a pure swap and nothing else… if a substantial amount is not replaced then we will move towards a less- cash if not a cashless economy. To me that is unlikely as there is no word of moving to a cashless economy. Only when RBI releases its next annual report we will know how much of the old currency is replaced with new one.

In case of a currency replacement there is no long term structural impact. In fact cash economy will grow after a hiccup.

If this a true demonetization then people will switch to cheques cards etc and transactions will be recorded. govt will get more taxes and this will be effectively a tax increase. Normally a tax increase causes slowdown but given high deficits it may not be so bad.

As of now banks have seen a surge in deposits as people are rushing to deposit junk notes and there is limit on atm withdrawals. So it’s no surprise that banks are flush with liquidity and they are lowering rates. Once ( or rather if) withdrawal limits are relaxed people will drain the banks of all this excess liquidity . Since banks are cutting rates they are expecting this liquidity to be long term of if not permanent.

1 Like

Right now it seems that the poor have been the hardest hit by the demonetisation (or currency replacement if you will). The road side vendors, daily wage labourers, micro entrepreneurs etc. It seems that right now there is more less-cash than cash-less. However, when it comes to money, we underestimate the ability of human beings to evolve and adapt. What do you think people will adopt more easily to - less cash or cash less? No matter how tech-handicapped, people will find a way to adjust and cope. More so now because we have online payment wallets, UPI, NEFT, RTGS etc. I never had to teach my mother and grand mother to use Whatsapp, but they do use it. More often than myself. You know why? Because the impression of it being free (as far as SMS/STD calls are concerned).

- Word on the street says that retailers and small shops are queuing up to get POS machines installed at their shops.

- People are getting more comfortable paying via PayTM.

There no doubt is greater uncertainty as to how this will pan out in the short term. If I were in a position where I handle other people’s money (i.e. a fund manager), I would play it safe. Thats what has happened. Wish I had the cash to buy in this correction.

FYI - Some stats:

- About 5.5 lakh crore worth of deposits in the demonetised 500/1000 rupee notes have been received so far, across all banks.

- About 1.1 lakh crore has been withdrawn by people via ATMs banks

- With more ATMs being recalibrated and the supply of 500 & 2000 rupee notes set to increase, this cash crunch will end soon. Probably by 1st week of December.

And as predicted earlier - interest rates set to fall. All interest rates will fall very soon: Arundhati Bhattacharya, SBI

1 Like

Indians have a high tolerance for pain and low tolerance for change. That’s how we missed industrialization in 18th and 19th century and that’s why we turn away large industrialization proposals due to resistance from locals. I know this is a generic statement but I think it will apply in this case also.

People I have interacted with are taking a wait and watch approach while enduring the pain. Everyone is hoping that cash will be available soon so they can just go back to their usual way rather than adapt change and switch to checks and cards let alone mobile and other newer payment options.

Even the chaiwala in my office is already planning to turn off his paytm option as he sees people are now having enough cash just a week after he signed up for Paytm. chaiwala is one of those cases where low value transactions have disproportionately high cost of non-cash payments as most payment providers have a fixed cost per transaction. Most of the consumer transactions in India are low value so recipients can’t afford to switch to non-cash options. Only discretionary services (restaurants, entertainment etc) take non-cash payment as they have high margins. So even those who are willing to change aren’t doing so for economic reasons. Govt could have pushed Rupay network to compete with Visa and Mastercard to lower the transaction costs.

Do we really want the cash crunch to end soon? That sounds like a useless question but we have to ask why did we get in this place first? The official word is to address black money,corruption, counterfeits etc. Except for the last objective, the first two will be back with a pause once the cash crunch ends. I think this is a popular misunderstanding in India that black money is in the form of cash. Black money is unaccounted income and income is unaccounted when transactions are settled in cash. That’s the link between black money and cash. If the cash is back how do we solve the black money? I guess the answer is, it depends on how much cash comes back.