V Vadiyanathan explaining everything in a simple language and quite interesting to see he talking about retail booking growing to 1lac crore from current 35k

3 Likes

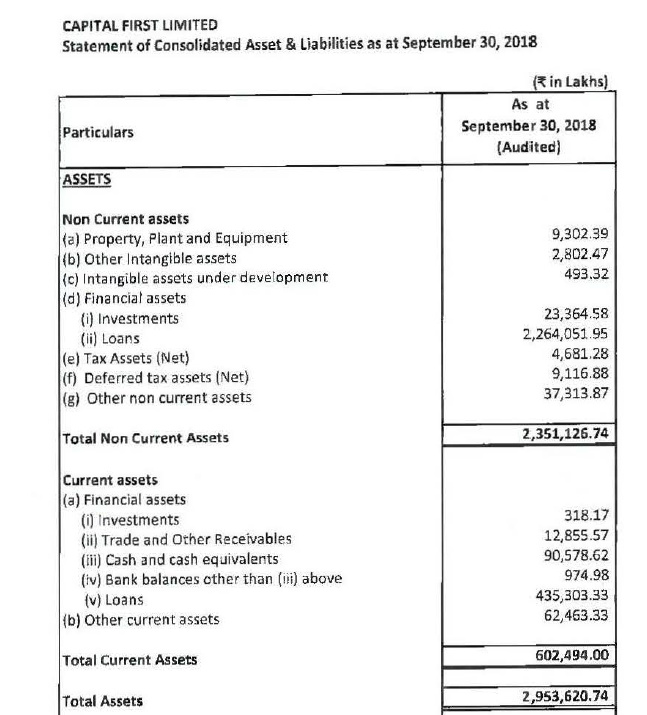

All is fine however what is the reason behind increase in Gross NPAs. One time loss on account of merger in P&L is fine but increase in Gross NPA (from 895 crores to 1671 crores this quarter) has nothing to do with merger accounting. Is that because of Capital First NPAs now been booked in consolidated accounts?

If capf has avg. Gnpa of 2% , then add ~650 cr. Gnpa for capf loan book.

In last quarter concall, mr. lall had mentioned npas would further come down without further provisioning. So I was slightly disappointed as I thought combined nnpa would be in 0.7-0.8% range.

Now opex has to be watched I guess as that’s on the higher side. Hope thats spent as productive expenditure rather thanas non productive expenditure.

Disclosure: invested

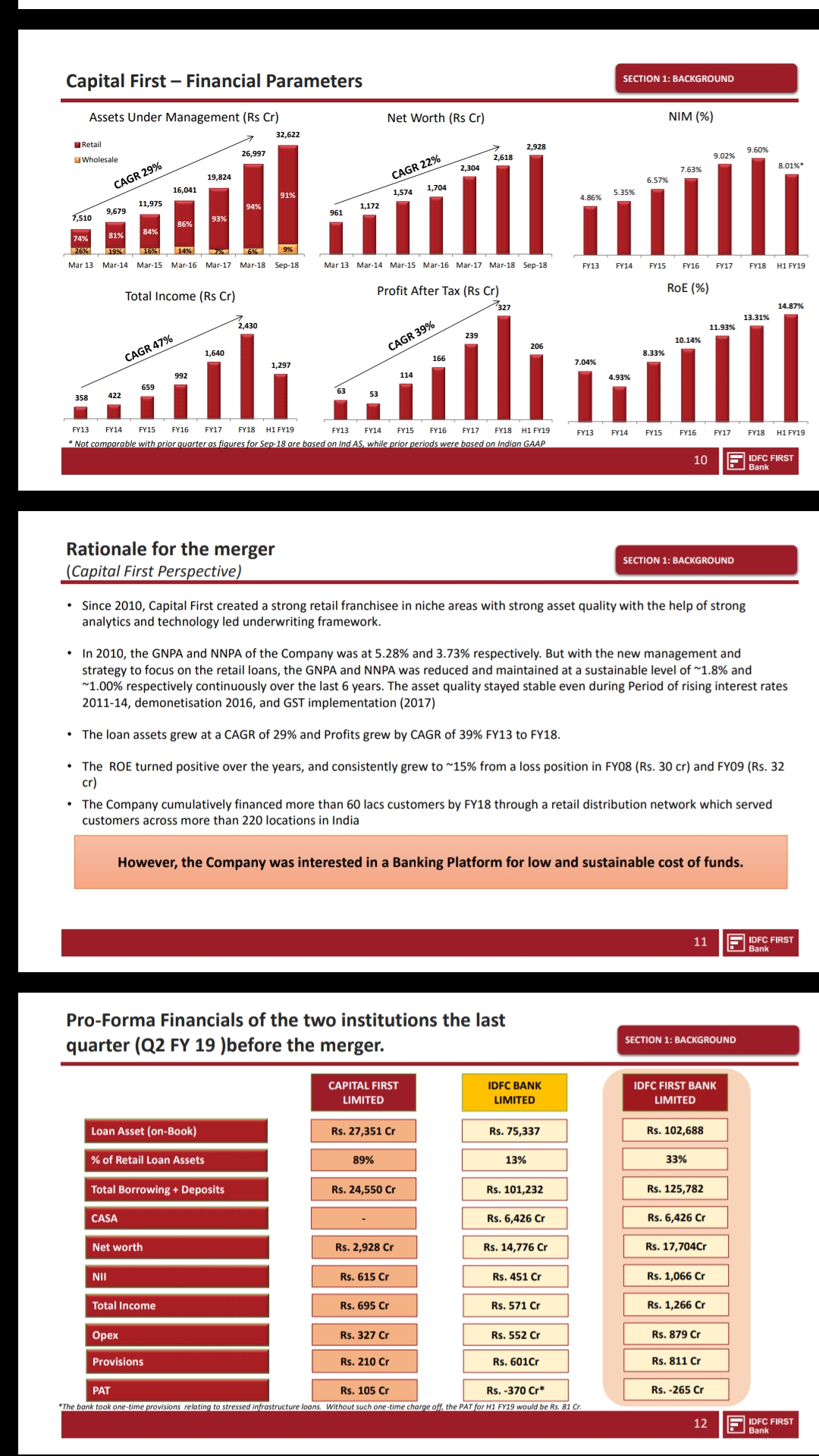

Thanks Vicky. I just checked Sep 2018 financials of CAPF. It had loan book of around 22.6K crores. if we assume GNPA for IDFC bank remained same qoq, there was increase of 776 crores on account of merger which is ~3.4% of CAPF loan book. I consider this value to be quite high for a retail NBFC and wonder why these NPAs were not cleaned before merger like IDFC Bank tried to clean up its books before merger.

sorry. it was 27K (22640+4353)= 27K. Even at 27K, 776Cr works out at 2.9% which is marginally on higher side. For a good retail NBFC with strong underwriting standards, it should be max 1.5-2%

1 Like

32.6 k cr. is the AUM, 27.x cr. is the loan assets. Both q2 fy19 figures. Refer to the attached page from IDFC first bank presentation.

1 Like

You are right however asset under management includes cash holdings, investments in government bonds and other assets as well. NPAs are generally calculated as % of loan book

Right. IDFC bank and/or capf have contributed to npas in Q3. Btw As per the page quoted above, capf had gnpa of 1.8% (it says maintained continuously, so q2 figures I guess)…

lets hope NPAs reduce going forward and all the legacy issues are taken care of.

1 Like

So what is the conclusion @dgoel25, is the increase in GNPA due to CAPF loan book or IDFC is still misfiring its legacy infra assets!

Do we any idea about the remaining loan book of IDFC bank in the merged identity?

From Ujjivan experience, branch expansion is pretty costly affair. Ujjivan Cost to income ratio is close to 70%!!

Interesting read.

8 Likes

Very aggressive targets for CASA growth. Each bank desires CASA but few succeed. Need to watch closely.

~600 cr was capf gnpa which got added into the bank as per Mr. Vaidyanathan.

Need to carefully watch the NPAs as more might tumble out in coming quarters…

Hello members,

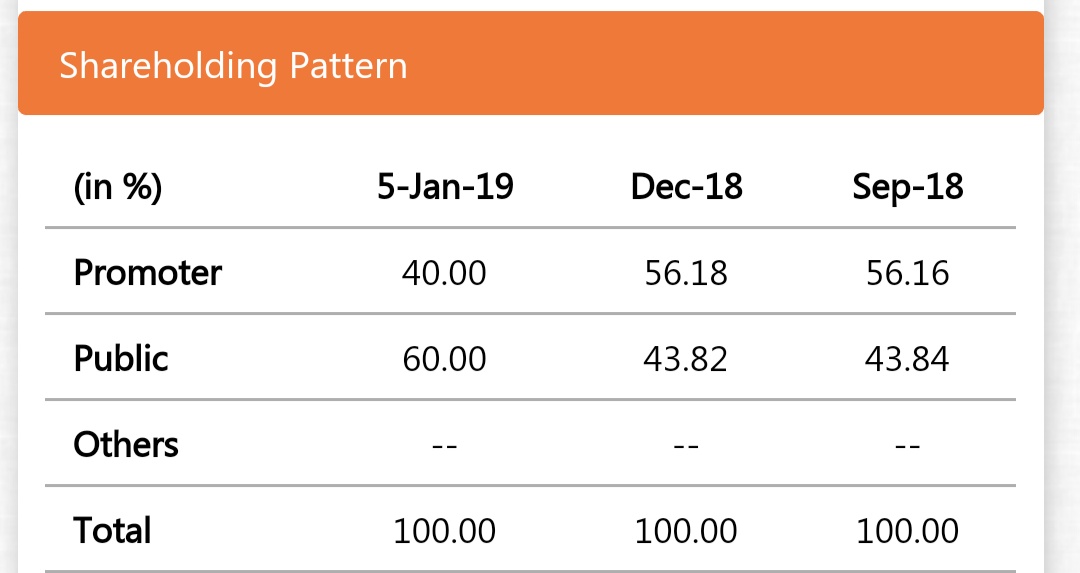

Please find the % holding of IDFC ltd in its subsidiaries below:

My doubt is, should we invest in IDFC First Bank through IDFC Ltd instead of directly investing in IDFC First Bank?

I mean, market cap of IDFC ltd is around Rs.5500 crores and Market cap of IDFC First Bank is approx Rs.21000 crore. IDFC Ltd holds 56.18% stake of IDFC First Bank which is approximately equal to Rs.11797 crore.

This is not all, IDFC Ltd is planning to monetise all the other assets (except Banking and AMC business) by end of the CY19. This is expected to result into net price of Rs.1200 crore which they are planning to transfer to share holder in a tax complient and tax efficient way.

After this, they will be completing 5 years in october 2020 with the banking license which means they can reduce their stake in IDFC First Bank to 40% and they have kept the option open to do so (Q3FY19 concall) which will bring more cash inflow to IDFC Ltd.

On AMC front, they are expecting to increase PAT 3 to 4 times in next 3 to 4 years and expecting to monetise assets from AMC after that.

So, it seems like IDFC Ltd is trading at very high discount than it should be…

Anyone having understanding of this, can you please help the community to decide if they should invest in IDFC First bank through IDFC Ltd or should directly invest in to IDFC Bank Ltd?

Disc:invested in IDFC First Bank Ltd.

1 Like

IDFC ltd has 40% of bank. Every share of IDFC ltd has

- about 1.2 shares of the bank,

2.the AMC biz. (Probably worth 7.5-10/- a share, as 9 month fy19 PAT is 44 cr., This being a down year for MF industry ) .

- rest of the businesses Which as per the management are worth 7.5/- per share post taxes paid, which they will distribute likely via buyback this year…

One may look at the bank or the hold co. Depending on the discount he’s attaching to bank holding in the hold co… the hold co. discount ranges anywhere from 30 to 70%.

Disc: Invested in both, disappointed by decision to not reverse merge with bank post Oct 2020.

1 Like

IDFC holds only 40% in IDFC first bank post the merger with Capital First with effective date of 5th Jan.

1 Like

Thank you for the clarification vicky…

1 Like

5 Likes

Hey all, I like IDFC First bank. Here is my thesis. 05022019 IDFC First Deck.pdf (2.6 MB)

Let me know if you wanna discuss anything…would love to collaborate…

9 Likes