If you assign BV if 2, market cap will grow to > 30K CR. Current business doesn’t justify that valuations atleast for 2 years. We need to wait for atleast one year to see how IDFCfirst is transforming.

True, assigning a multiple of 2 is not the right thing for IDFC First Bank right now, and at current market price of 50, it might be rightly valued temporarily… assignment of 2 PBV is difficult to forecast currently.. but assigning a multiple of 0.7 is also not the right thing… specially to good management, their vision and proven record…

It should trade in the range of 1 to 1.5 curently untill we see some certainty in earnings which will be clear in next few quarters. I assign a very less probability to scenario where market will rate it to 0.7…

1 Like

50 page report with elaborate comparison with peer group by Morgan Stanley. But it is amusing to see there is no comparison of NPAs ?! Is it because they couldn’t get the data on NPA?

Let me highlight their some favorite stocks, Axis bank has 5.5%, ICICI Bank has 7.5%, SBI Bank has 8.5% Gross NPAs!!

While the stocks they hate, RBL Bank has 1.5% and IDFC First has 2% Gross NPAs. So comparison will not look good on a chart that’s why better to skip this data.

Also, they were overweight on Yes Bank with a target of 400 till last year, what happened there!

Morgan Stanley revised RBL Bank rating to Sell in Oct 2018, Stock is up 35% since then!

14 Likes

Its too early question Vaidyhanathan. Whats undeniable is his brilliant track record, especially how he built Capital First. At the same time, IDFC bank comes with a huge baggage. A target of 30 is a huge cut indeed and I dont agree with their PBV.

There will be short term pain. I view this entity as a 3+ year story. It may take minimum 10-12 quarters to put this bank on the right path.

Disclaimer: Invested. If this goes to 30, I will happily add more.

2 Likes

Can u pls elaborate on what exactly is the security issue for stocks held in dmat form? I think now statements are given by depositories as well…thanks

I have heard instances of the number of shares changing in the online statements provided by discount brokers. Disputes mostly get resolved, but what if there is a fraud. There have such instances as well, I think in IndiaInfoline.

I think demats with banks are safer for coffee-can kind of investors. Better still, get them rematerialized, if u r gonna coffee-can them anyway.

1 Like

IDFC first bank features in top 10 Forbes Indian banks for 2019.

"The list is largely based on customer satisfaction instead of balance sheets and PnL.

Banks were rated on general satisfaction and key attributes like trust, fees, digital services and financial advice."

1 Like

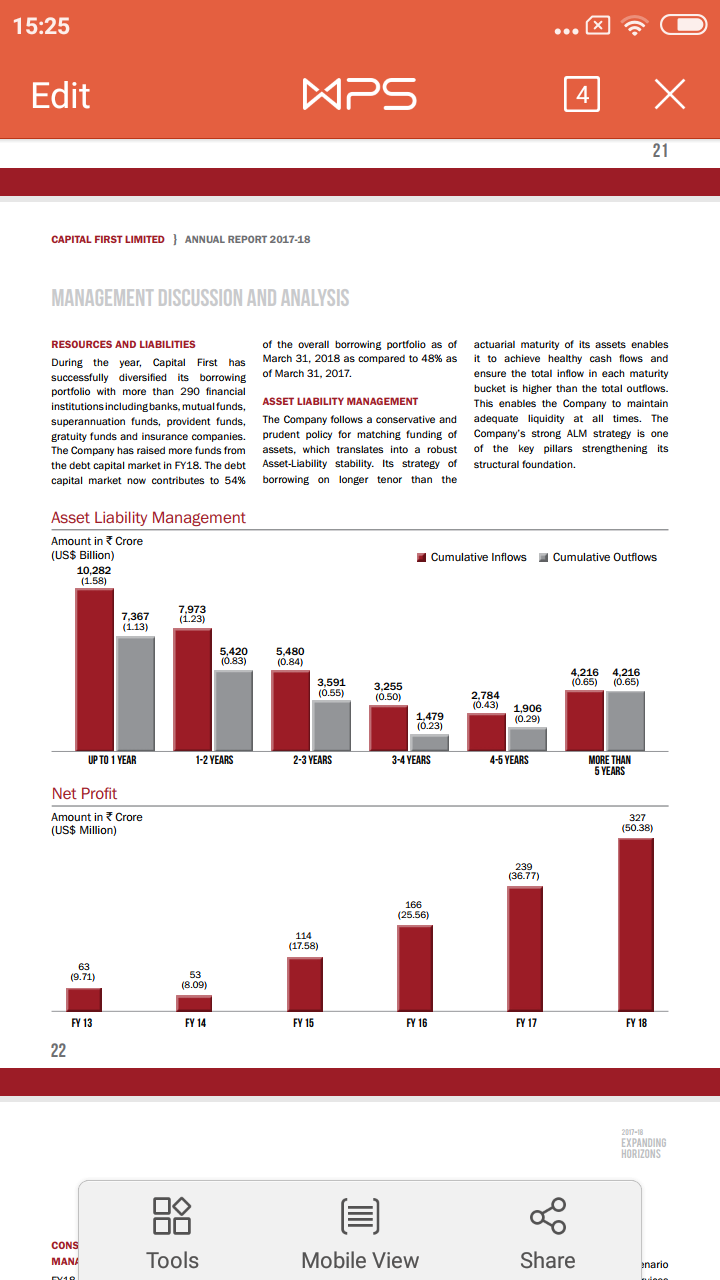

Following is a screenshot from capital first fy18 annual report showing that majority of the assets and liabilities mature in 0-2 yrs. The maturing debt should get replaced by cheaper funds (150-180 bps cheaper as idfc first bank’s cost of funds is cheaper by that much amount).

4 Likes

How much importance should we give to ROE for Banks?

Asking this, because a banks has very high leverage and ROE is a function of leverage. ROE is manipulated easily by changing leverage. So, should we give much importance to ROE given that bank has high leverage?

Look at RoE and RoA both

It’s a very much important metric in evaluating banks, prefers banks with high roe and lowest leverage, high leverage erodes the book value even there are small percentage of NPA

This is where ROA(return on assets) comes into picture, banks with high ROA with low leverage can have same ROE as bank with low ROA and high leverage

So ROA can be considered important metric than ROE, as ROA increases ROE increases

ROE = ROA×(Debt/Equity)

4 Likes

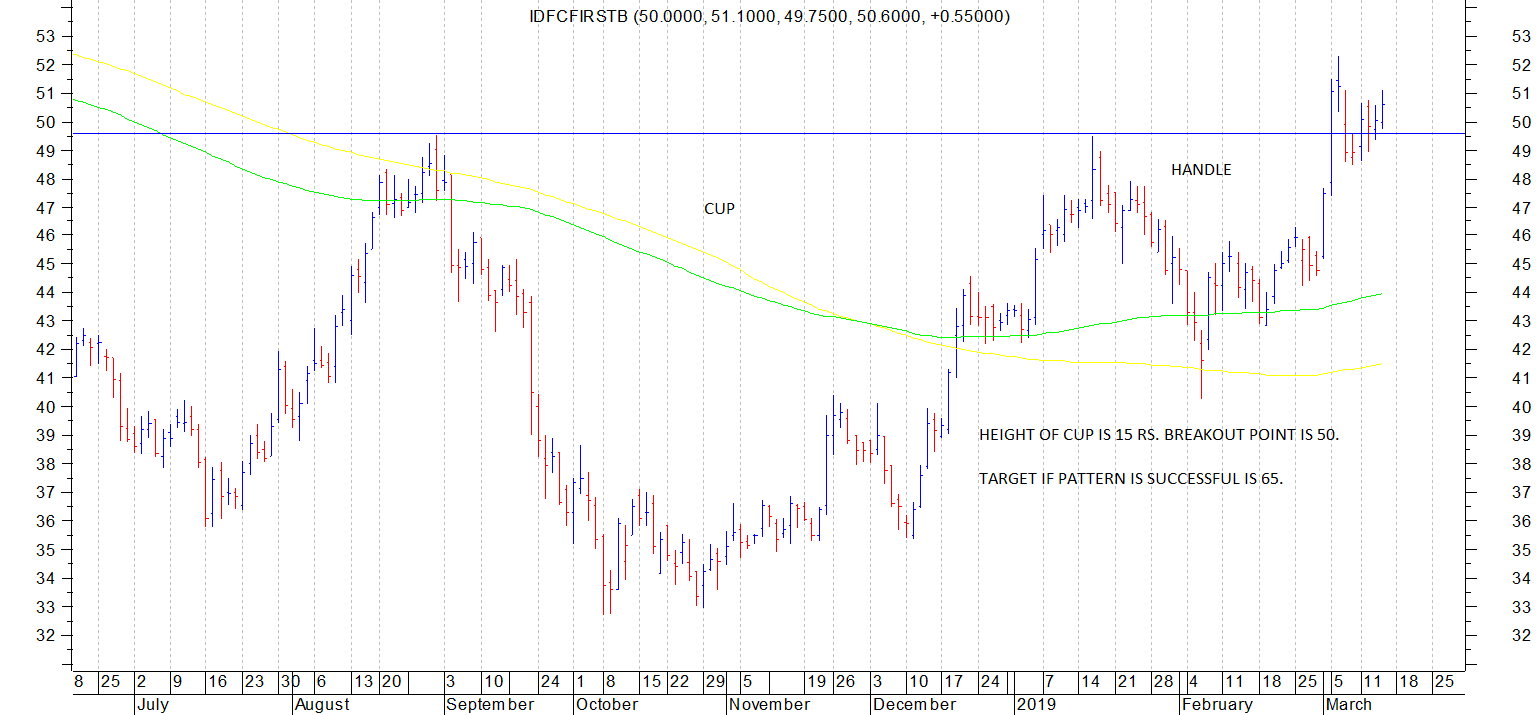

IDFC First Bank has broken out of a cup and handle pattern on daily/weekly charts. Potential target could be 65.

disc; invested based on technical pattern with a strict appropriate stop loss.

7 Likes

What’s the stop loss? Since you are already discussing your trade and possible price target, I hope disclosing stop loss isn’t an issue either.

First of all this is not a recommendation. On valuepickr we dont recommend stocks. All these posts are aimed at enhancing knowledge through sharing. Disclosure is made only as a standard procedure.

For my own trade i usually use the recent swing low as a stop loss which i consider appropriate. For anyone contèmplating investment in the company he/she should do their own due diligence and take appropriate decision.

9 Likes

So, instead of looking at ROE one should look at ROA and the leverage seperately… It is fine if ROE is slightly lower due to lower leverage…

Instead of comparing ROE, one should compare the ROA and leverage…

But in Morgan stanley report where they have given the target of Rs.30, they have given a very high weightage to ROE…

1 Like

Hitesh ji can’t IDFC Ltd is better bet than IDFC Bank >it has better book and also have stack in the IDFC Bank.

When the chart pattern is as clear and classical as it is shown above for me it becomes a strong buy based on technicals.

I think fundamentally the picture will emerge clearer after 4-6 quarters of Vaidyanathan being in charge and we see how things are moving forward. Till that time all the number crunching we do is all guesswork and prone to errors.

Regardging IDFC Ltd the valuations may very well be attractive as you mention (I havent checked it to either confirm or reject it) but as long as the ticker doesnt show some strength as shown by IDFC Bank I dont want to consider it. In both IDFC and IDFC Bank it is very difficult to project any numbers confidently and hence I am not even trying.

For me a technical pick should have a clear cut pattern, visible stop loss and targets and sufficient volumes to take a position and exit in profit/loss if needed. There are huge volumes traded on IDFC Bank and so volumes atleast is not a concern for me.

7 Likes

I wanted to open an account with IDFC First bank… so registered for the call back from them on monday… but didn’t received any call from them… So… registered again for the call back on Wednesday… again no responce from them… they just gave me reference id and did nothing…

So… tracked my reference id from their helpline number… then finally they arranged an executive who visited my home to open my account with them…

It took 1 week for them to arrange an executive… Frankly speaking… i expected better service…

Fine… it was acceptable till this… bt… what I found a real problem is… they have only a 1 product to sell to me… a saving account and that too… one varient where I was required to maintain Rs.25000/- average daily balance… that was on the higher side compare to their competitor… They didn’t have even credit card for their customers…

I enquired to their executive about the changes after merger… he said few things changed… but his main point was… earlier… it was easy for them to convert a walk-in guy into a customer… bt now people just inquire abt the account after looking at advertisement of 7% but it is difficult to convert them as 25k is too high balance to keep into savings account… and you knw… the FD rate below 1 year is also 7%… don’t know why…

Having only one saving account with min balance of 25k and non maintenance charges of up to 400… both are on the higher side compare to competitors…

Only positive is their goodies with this… unlimited atm transactions… cash back on book my show… free lunch at airport… etc…

Bt still… i doubt on their strategy to increase CASA unless… they are planning to develope it…

1 Like

They are introducing 3 different kinds of savings ac from April and we can convert to an account which requires lesser min bal. I think this will start along with their new website which comes soon. Source: idfc executive who opened my sb ac

2 Likes