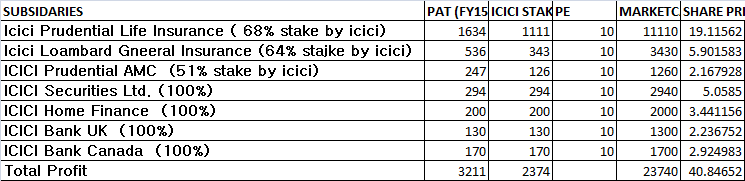

ICICI bank needs no introduction- being the largest private sector lender.

Almost everybody knows what this bank is up to and the negative news surrounding its stock.

Without beating around the bush, let me come straight away to the point as to why this thread.

Let me quote some figures straight from its q3 results-

-

Q3 NP( Standalone)- Rs 3018cr vs provisioning of Rs 2844cr

-

TTM NP ( Standalone )- Rs 11980 cr vs provisioning of Rs 6100cr (aprox)

-

Present value of net NPAs ( as on 31 Dec 15 ) - Rs 10,014 cr

-

Present value of Restructured loans - Rs 11,294 cr with no major restructuring pipeline.

Some conservative assumptions-

-

All Net NPAs are written off.

-

30% of restructured loans ( experts say 20-25 % ) become Net NPAs.

In such a situation the bank will have to take a hit of - Rs 13000 cr (Aprox)

Compare this to the TTM profit of ICICI bank ie Rs 12000 cr ( Aprox )

That means, if ICICI bank were to part with its one year profits, it would become clean all over again.

Thats about the the over hyped asset quality concerns vis a vis the bank’s cheap valuations.

Post this cleaning ( suppose it were to happen ), the bank has 2-3 options-

Option 1. Start behaving like HDFC or INDUSIND bank. ( unlikely, but possible )

Option 2. Start behaving like Axis Bank atleast. ( Likely )

Option 3. Keep behaving like ICICI bank ( Remember 2008 !!! )

In case of option 1, it will become a super multibagger largecap. ( otherwise a rarity)

In case of option 2, it will still become a multibagger.

In case of option 3, It will still go up 2-3 times from here on when the market cycle turns and some time passes ( 2-3 yrs that is )

Disc: Not invested. Planing to invest.

Objective of the post:

- To validate my theory. ( Is it as simple as I am thinking it to be??? )

- To stimulate a healthy and informative discussion.

Eagerly waiting for the better informed to throw some light,

Ranvir Dehal

)

)