@Ankur_Lakhia , For a head and shoulders pattern to play out, its not necessary for the two shoulders to be of same magnitude. The right shoulder or even the left one may be smaller than its counterpart.

Attached chart shows the pattern. If and when the pattern plays out it points out to targets in range of 8500-8600 where the retracement of entire rise is placed.

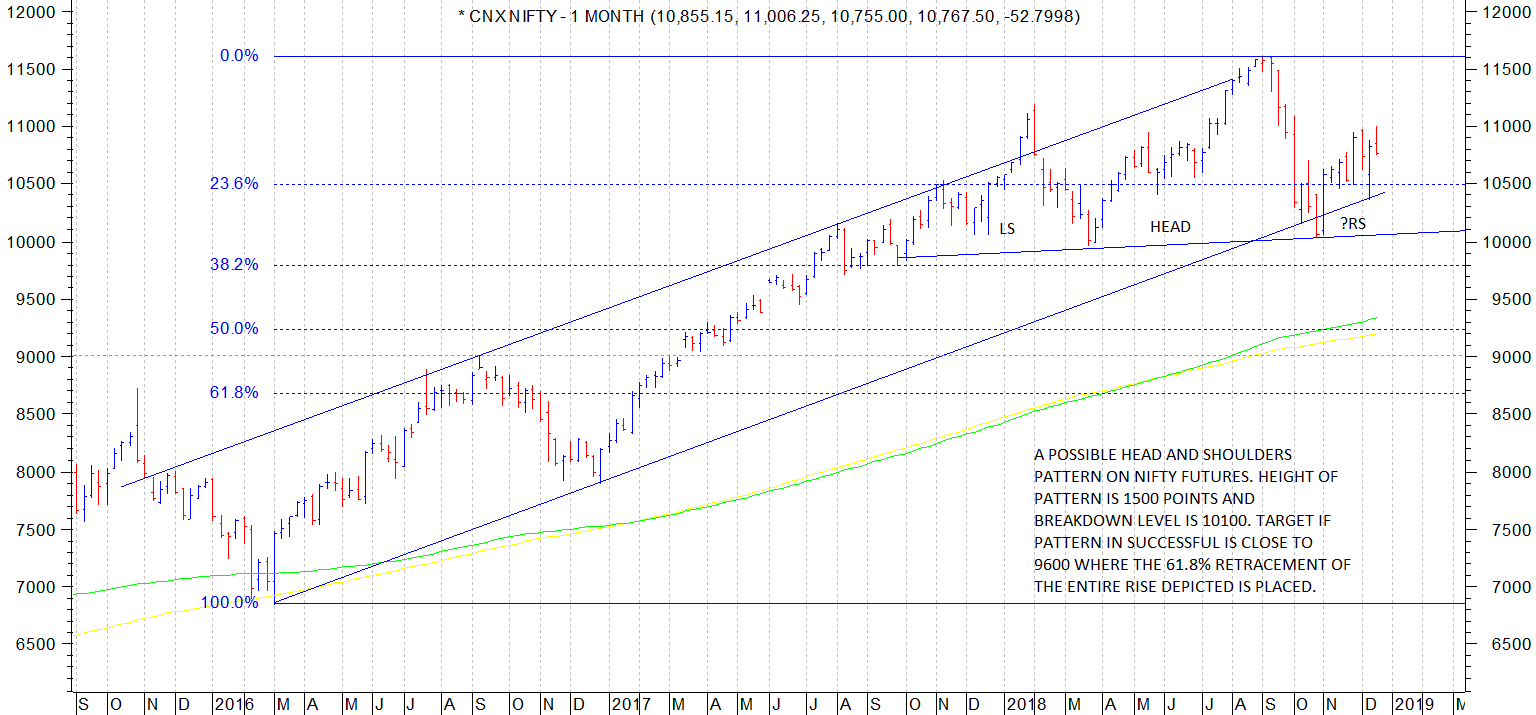

The current rally has taken a lot of people and even technical analysts by surprise. People have changed their views from a possible meltdown to a possible new high. Even the small and midcaps have started showing some resilience of late. How this whole structure unfolds needs to be seen.

Personally I remain cautious considering the political scenario. The silver lining has been the drastic fall in crude prices which has brought cheer to a lot of sectors of the markets.

This sounds quite ominous and fearful. It’s a flat 20 to 25% drawdown from current level. If this H&S pattern plays out, it would result in average portfolios drop in excess of 30-50%.

My view if Monday will be extremely critical. Any significant drop will result in acceleration of fall. Caution is better than bravery, is what I can understand.

Disc. I have negligible skills in technicals. Just sharing my thoughts.

Thank you for your response. I have one follow-up query. In your reply, you mentioned Nifty retracing of 61.8% of rise in line with Fibonacci sequence. My question is whether it is possible to retrace 100% of rise? Past two bear markets in 2000 & 2008 ended with Nifty P/B around 2.0 - 2.1 range. If we apply same criteria today then target comes around 6700-7000 on Nifty which represents 100% of retracement. That is the reason for asking this question. Is 100% retracement possible from technical point of view? This is not to predict any market level but for the purpose of better understanding of technicals with real time picture of what is happening in market.

IMO, ROCE is more important. it will tell you how good business is.

for example, ROCE is 8% for fixed deposit. I think, for ROE we also need to think of dept on balance sheet.

The levers to boost up ROE are net margin, asset turnover and leverage. So sometimes companies with very high leverage can show high ROE which might induce false conclusions. ROCE on the other hand removes the distortions caused by high debt.

Just for the record ROE is net income divided by shareholders equity. ROCE is calculated by getting the ratio of EBIT to the capital employed. Capital employed refers to total assets of the company minus all current liabilities.

Essentially speaking if one is looking at a company generating high ROE one has to look at it a bit deeper into the levers boosting ROE and if leverage is the prominent factor one has to be careful.

If I have to prefer only one parameter I would prefer ROCE. And a step higher would be to find out return on incremental invested capital.

Companies with very high ROE/ROCE with little growth usually remain in a range for long period of time. Ideal scenario to find winner is is to look at companies growing with increasing return ratios. (usually due to higher asset turns in companies with low margins (titan is a classic example) or with improving margins. (ajanta pharma is a classic example from 2011 to 2016))

While predicting using technical analysis the tagline to use is nothing is impossible. So 100% retracement is also possible. And usually for severe corrections, 61.8% ratios is the ratio to lookout for, sometimes corrections finish much before these levels often at 50% retracement levels.

What I tried to correlate in the chart I put up was that the potential target provided by a potentially successful head and shoulders pattern would be 8500-8600 which is in close vicinity of the 61.8% ratio of the entire rally.

I have no idea whether the head and shoulders pattern would play out or not. The index may remain rangebound and frustrate everyone or else take a dive and play out the path described by the head and shoulders pattern.

Technical analysis is often the art of connecting the dots using different methods and parameters used in technical analysis. I think the best method is to try to use both technical and fundamental analysis if possible.

Technical analysis is often very helpful in finding out sectoral rallies as most of the companies in sector would have similar structure or atleast similar trend.

Hi @hitesh2710 ,

I have a related question to ROE- the problem that I face. How much discount the PE multiple should have , Or is expected to have for a company that has ROE of 15 vs a company that has ROE of 30?

PE is not arrived at only considering ROE. The P part of PE ratio is determined by markets and hence the ratio will vary from time to time depending upon market moods. There is no one size fits all kind of answer to this question.

Determinants of PE ratio would include growth rates, ROE, balance sheet strength, future prospects, sectoral fancy, sectoral positioning like market leadership etc and so on and so forth. You can go through Basant Maheshwari’s The Thoughtful Investor or Pat Dorsey’s Five rules for successful investing to get a better idea on it.

There is no alternative to reading and digesting basic books on investing if one is serious about investing. In my list that would include Peter Lynch’s One Up on Wall Street and Pat Dorsey’s book mentioned earlier.

@hitesh2710 thanks for the response, I have read one up on Wall Street and the thoughtful investor. Yet I don’t have anything but intuition to guide me. I would like to know your opinion on whether PNB housing is really cheap right now as compared to gruh finance as that is the reason for my question😁

Regarding finding out whether PNB Hf Is cheap wrt gruh, u can do a small exercise.

Put up comparative figures like historical growth rates for say 3-5 years, in terms of revenues, profits, compare ROAs and ROEs of both companies, compare Book values of both cos, dividend payouts, NIMs, earnings and price earnings as of now (and historical if possible) , NPA ratios, provision coverage ratios and then try to figure out the query.

Besides these Gruh will always enjoy higher valuation because of the parentage it has as compared to PNBHF, besides the kind of clients it caters to and the competition which it is likely to face in its subsegment. (like how easy it is to dislodge Gruh vs PNBHF) . A crucial differentiating point would be the avg ticket size of loans of both companies.

According to my view, its difficult to compare gruh vs pnbhf because it is not an apples to apples comparision since the business segments both companies address are different and that leads to difference in competition both companies are likely to face.

I have read the books recommended by VPickers such as One up the wall street, The Intelligent Investor and Pat Dorsey’s Five Rules for successful investing. Along with this I have also read Mark Minervini’s 2 books. I haven’t read any book specific to/targeting indian audiences and markets. Are you also of the view that Indian markets behave differently than what is mentioned in these books.

Markets are not obliged to follow a path outlined in these or any other books. Its practically very difficult to predict the market path atleast for the short to medium term.

What these books would provide is a way to find out good companies and a way to figure out a reasonably good level to buy these companies.

I have always found Peter Lynch’s teachings in his book to be easily applicable to Indian markets.

My views on NBFCs have not changed much. I still think its difficult to imagine most of them giving above average returns. There would be the odd counter trend rally or some of these companies can remain range bound for a long time.

Ideal thing would be to focus on individual names in the NBFC sector and try to figure out how these would gain with a lot of smaller fly by night operators leaving the field. Dominant names in sector niches would make for good investments. Good thing is there would be plenty of time to accumulate these good companies over next few weeks and months.

hello sir,

your view on Shaily Engineering plastics…they are niche plastic moulding company having ambitious target of doubling their revenue in coming 2-3 years. They are entering into carbon steel furniture business and seting up a plant for the same.

As far as i think CS furniture biz is not a niche segment and currently many unorganised players are into it. Shaily which known for their skillset in innovative plastic componentrs biz entering into ordinary CS biz may dent their profit margins.

Hello Sir,

I have some tracking quantity of Coal India and want to know your views on it. I feel coal demand will be there in India for sometime as we dont have any other scalable alternative of power generation. Also it is the only company producing coal. But Coal India being a government company and it is not able to meet demand is a concern. So wanted to know your opinion.

I dont track Shaily very closely currentlly but the overall impression I got when I visited their plant and meeting the management was very favourable.

I guess (its only a guess) if they have invested in CS plant then they wont do so without considering all aspects of the business. They are a B to B player and hence would put up plants only if they see consistent demand coming up. And the products they manufacture are top class and would be much better than peers in terms of finishing, durability and quality. I think they might have had commitment from a big customer for regular offtake of the product before putting up any kind of capex.