Booming Metals Rally Signals Optimism on Global Growth

COMMODITIES

Investors pile into industrial metals, pushing prices of copper, aluminum and zinc to multiyear highs

Prices for copper hit their highest level in nearly three years last week.

Prices for copper hit their highest level in nearly three years last week.PHOTO: KHAM/REUTERS

SHARE

By Ira Iosebashvili and Amrith Ramkumar

Aug. 21, 2017 5:30 a.m. ET

Bullish investors are pushing the prices of copper, aluminum and other industrial metals to multiyear highs, betting that recent signs of resurgent global growth and falling supplies will stoke demand for raw materials.

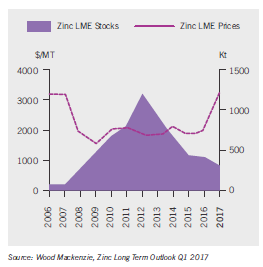

Prices for copper hit their highest level in nearly three years last week, and zinc reached its highest price in a decade. Aluminum has climbed to three-year peaks and iron ore has rallied nearly 35% since the end of May. Shares of miners have also soared, with the MSCI World Metals & Mining Index up roughly 13% during that span.

Driving the gains are expectations that this year’s nascent rebound in global growth will continue, with major economies around the world shifting into higher gear after a long period of lackluster performance. Many investors are also betting that reduced supplies and a selloff in the dollar will continue boosting prices, which had fallen in recent years alongside other commodities as new producers saturated markets.

The recovery in copper and some other base metals “has really only just begun,” said Christopher LaFemina, an analyst at Jefferies. “There’s much more to go.”

Global investors view demand for base metals as an important gauge of economic health, as they are the building blocks of construction and used to make everything from airplanes to smartphones. A continued rise in metals prices could help push up inflation in the U.S. and abroad, giving central banks a freer hand to raise rates or taper the massive monetary policy programs they have employed to kick-start growth in the aftermath of the financial crisis.

The rally in the metals sector affects everything from currencies in developing markets to debt from commodity-producing countries, some analysts said. Rising metals prices are a boon to countries like Australia, a major iron ore exporter, as well as Indonesia and Chile, which produce nickel and copper, respectively. The Australian dollar has risen almost 7% against the U.S. dollar since the end of May, while the Chilean peso is up roughly 4%. The iShares J.P. Morgan USD Emerging Markets Bond ETF has risen in five of the past six sessions through Friday and posted an 11-session winning streak in mid-July, its longest in more than five years.

With the backdrop for metals looking more supportive than it has in years, investors have piled in. Net bets by hedge funds and other speculative investors on a higher copper price stood at 120,175 contracts for the week ended Aug. 15, the highest level since the Commodity Futures Trading Commission began recording the data in 2006.

ADVERTISEMENT

The one-sided positioning and pace of the rally has concerned some investors, who worry that prices have gotten ahead of fundamentals and disappointing news could spark a rush for the exits.

“When the whole world gets crowded into one trade, it typically ends in tears,” said Christopher Stanton, portfolio manager at Sunrise Capital LLC. Mr. Stanton took profits on most of his copper and nickel positions last week. “If anything, this is a market begging to be shorted.”

Although analysts have cautioned that some investors have gotten ahead of fundamentals, recent supply disruptions and a strengthening global economy have continued to fuel the rally. The International Monetary Fund most recently projected global gross domestic product growth at 3.5% for 2017, up from 3.4% last July. The IMF raised 2017 and 2018 growth estimates for China, the world’s top metals consumer, citing strong credit growth and fiscal support. It also increased euro area growth projections, highlighting diminished political risks.

UBS Wealth Management advised clients to take a position in aluminum earlier this month, saying the metal will benefit from tighter supplies and stronger global growth.

That backdrop has buoyed metals prices, which have in turn supported stocks of miners such as Freeport-McMoRan Inc. and Glencore PLC. Shares of Glencore, one of the world’s largest coal, copper and zinc producers, have surged more than 20% since the start of June, though still well below a high reached in 2011. Freeport’s shares have climbed roughly 23%.

Lucas White, a member of global investment management firm GMO’s focused equity team, last year urged investors to buy shares in natural-resource producers as a way to take advantage of beaten-down commodity prices. A year later, Mr. White still believes “there’s good value in the mining companies,” and is “overweight” the sector.

“We believe these companies can generate earnings and cash flow,” he said.

Expectations for future supply shortfalls are fueling gains as well, some analysts said. Aluminum prices rallied recently after China cut its refining capacity and cracked down on illegal producers of the metal as part of an effort to fight pollution. Falling global stockpiles and production cuts have helped boost zinc prices by more than 20% this year. Although the International Copper Study Group, an organization of copper-producing and -consuming countries, currently sees refined copper usage and production almost equal, some analysts including Mr. LaFemina expect supply to taper off while demand growth stays steady.

A weaker dollar is also buoying prices, as metals are denominated in the U.S. currency and have become more affordable to foreign investors. The WSJ Dollar Index, which tracks the currency against 16 others, has declined roughly 7% this year.

A potential source of trouble could come from China. Economists have previously anticipated a broad slowdown in the second half of the year, as China’s leaders signaled they would continue efforts to tackle rising debt levels and curb home speculation. Evidence that growth may be cooling came last Monday, when data showed that the pace of Chinese industrial output, retail and housing sales and fixed-asset investment decelerated in July from the previous month and came in below economists’ expectations.

For now, however, investors are confident that China will prevent growth from slowing too much ahead of a key Communist Party leadership shuffle this year. And while some data wobbled in July, key metrics like total social finance—a broad measure of credit that includes bank loans and nonbank lending—remain robust compared with prior years, said Jerry Lucas, a senior strategist at UBS Wealth Management.

“China is trying to do a fine balancing act going into Party congress this fall,“ Mr. Lucas said. “No one’s interested in rocking the boat.”

Write to Ira Iosebashvili at ira.iosebashvili@wsj.com