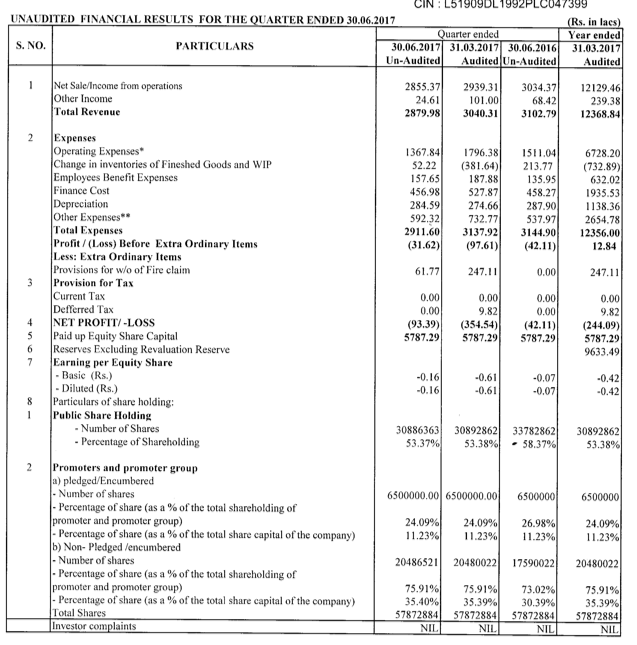

Margins seemed to have been improving throughout FY17 in Q1, Q2 and Q3 with 21%, 24% and 30% roughly but Q4 it has dropped down to 11%. Any idea what has caused this drop? Thanks!

Even though they have mentioned that demonetisation had not made any significant impact. But I believe it could be demonetisation. Need to see how the next quarter turn out to be.

I think it has to do with seasonality. Historically, March has been very weak quarter so it’s not right to compare QOQ. YOY is an apple to apple comparison and on that I think it’s been doing quite well for last at least four quarters. The business slowly and steadily seems to be turning around well but I would like to see more of revenue growth to confirm the same.

Yes thats true, expecting the next quarter should have a positive impact, If they started remaining 50 Cr worth product lines lying idle.

Got it. I just noticed that march OPM has been worse than the other quarters for the last few years as well. Point taken. Tracking this turnaround curiously to see if their sales improves.

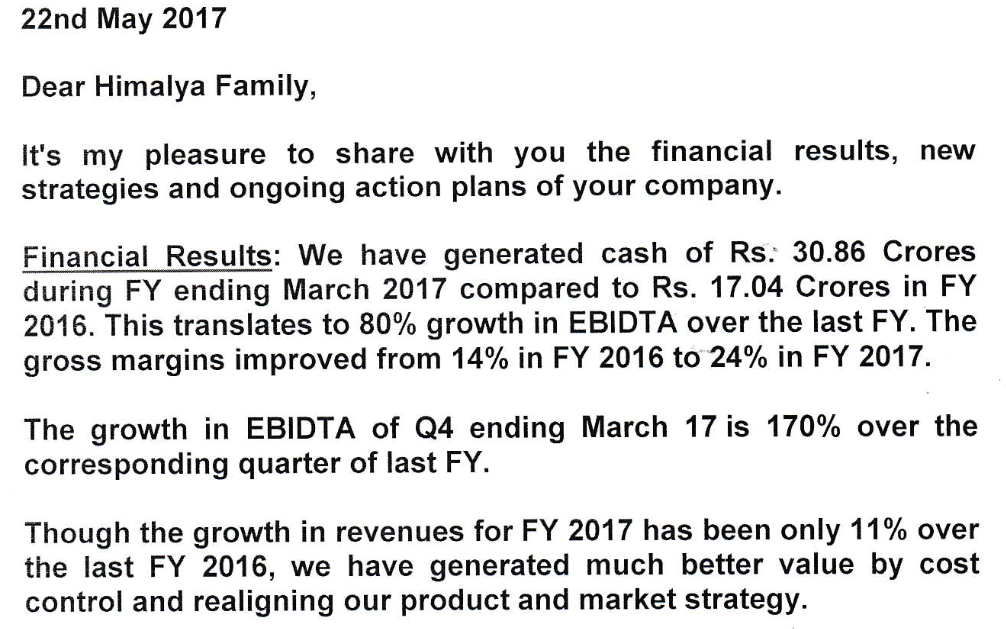

Chairman Letter.

As per Man Mohan Malik, All the processing units were re-opened in Gujarat, alteast we should see positive impact in the coming quarter.

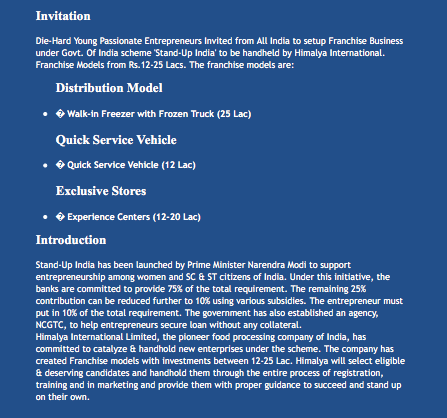

New Franchise Business Model. Need to see how this will evolve.

http://www.himalyainternational.com/FranchiseStandupIndia.html

Their products are listed on amazon.com. There Himalys Fresh has around 81% rating as a vendor, it is only from 112 ratings and in the past 1 year they received 41 ratings and looks like they are on amazon.com from atleast 2014 and dont see much happening there.

They have posted a customer service number on amazon.com website and I have called them around 5:45 PM Eastern Time and looks like they are closed by that time. Its too early to close though.

Their product basket seems to be good but it all depends on how much they can penetrate into domestic as well as US market.

Sebi penalises 6 entities for disclosures lapses

A probe conducted by Sebi found that these entities had failed to make the relevant disclosures in respect of the encumbrance of 65 lakh shares, amounting to 11.96 per cent stake, of Himalya International Ltd (HIL) during October 2014.

Sebi penalises 6 entities for disclosures lapses

Markets regulator Sebi today imposed a penalty of Rs 4 lakh on Himalya International’s six promoter entities for their failure to make timely disclosures pertaining to their encumbrance of shares of the company.

The fine has been levied on Doon Valley Foods, MM Malik HUF, Man Mohan Malik, Sangita Malik, Sanjiv Kakkar and Anita Kakkar for not complying with provisions of SAST (Substantial Acquisition of Shares and Takeovers) regulations, Sebi said in an order.

A probe conducted by Sebi found that these entities had failed to make the relevant disclosures in respect of the encumbrance of 65 lakh shares, amounting to 11.96 per cent stake, of Himalya International Ltd (HIL) during October 2014.

1 Like

Share holding pattern for June 2017.

16 Lakh shares released.

http://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=526899&qtrid=94.00&Flag=New

Very Good Analysis sir …

ALL THE BEST SIR

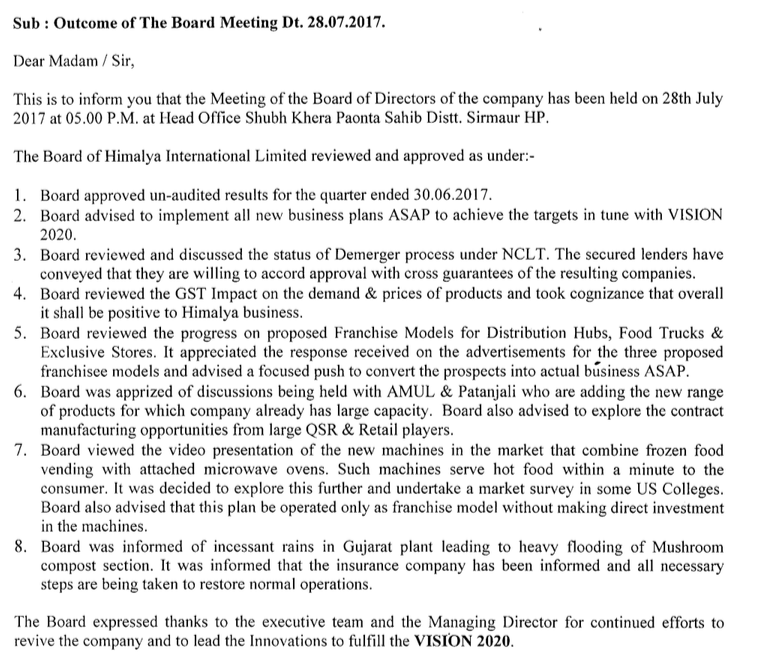

Chairman`s Letter 29Th July 2017

Dear Himalya Members,

Please allow me this opportunity to share the ‘State of affairs’ of your company.

Financials: The Q1 financials have been posted at BSE & our corporate website www.HimalyaInternational.com. We have generated cash of Rs 710 lacs during the quarter ending June 2017. **The capacity utilization during the period has remained low with most of the revenue coming from Mushrooms.**We have been consistently cutting down the cost of operations leading to better margins. The EBIDTA margin is 24.86% during the quarter ending 30th June 2017. The major boost in performance shall come only by putting the dormant production lines in operation.

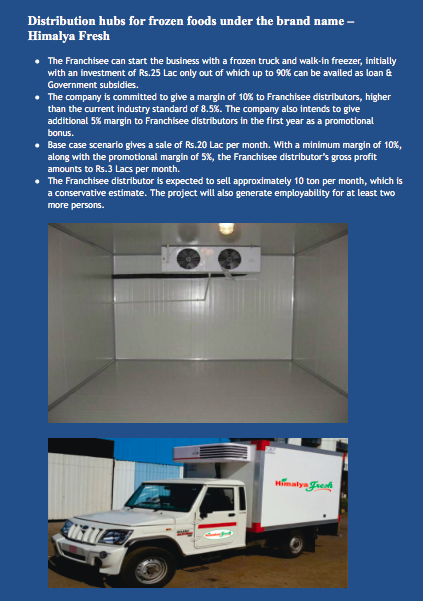

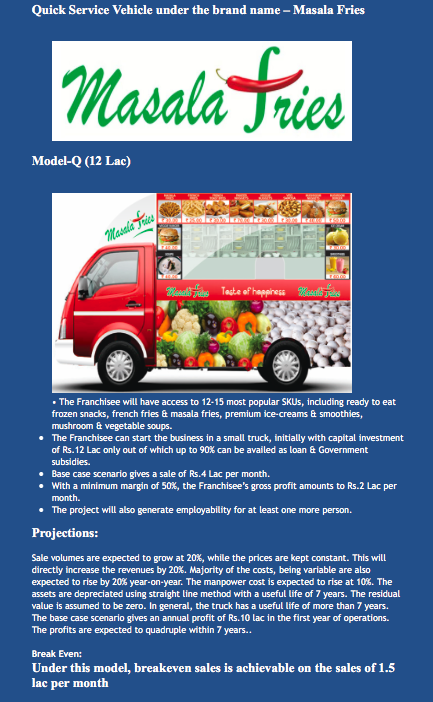

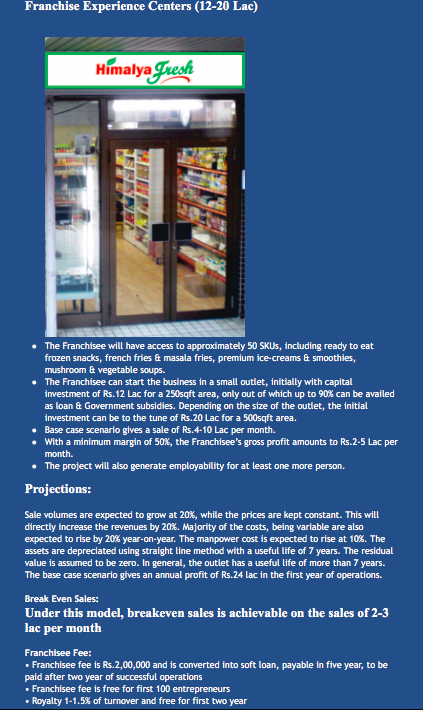

**Franchise Models:**We have great expectations from our new strategy to enter domestic Indian market by way of three Franchise models; Distribution Hubs, Quick Serve Vans (QSV) and Exclusive stores. Implementation of these models pan India will fill all the production lines that are

lying idle.

Mobile Food Truck business is the fastest growing segment in food service industry. This segment has grown by 400% from USD 650 million in 2012 to USD 2.7 billion in 2017 in USA. We are receiving very good response for all three models and especially the QSV model. The QSV model with small investment has stirred great excitement with youngsters aspiring to start the Mobile Food Trucks to serve fast foods to ever increasing mobile population in towns & cities Pan India. Our QSV will be a new avatar with look, feel and efficiency of the Quick service Restaurant chains but serving better & healthier food at substantially lower prices than the multinational QSR chains. We have already concluded all aspects of this model & created SOP’s and training modules to handhold the young entrepreneurs. The details can be viewed at our new website www.HimalyaFranchise.com. We hope to start the first lot of QSV’s by October 2017.

New Export Markets: We have entered in contract for sale of our products in Brazil market and shipments have started this month.

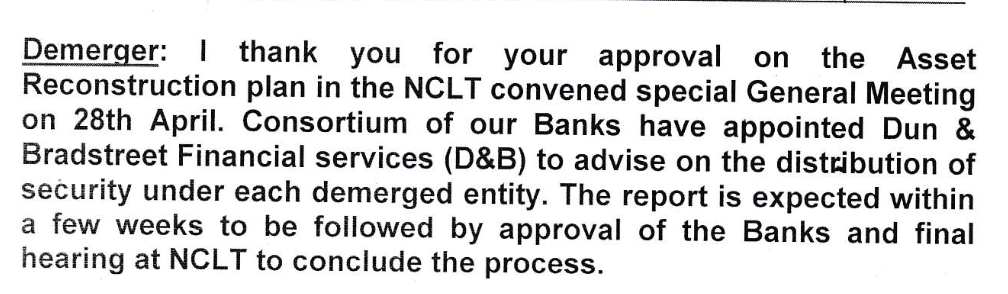

Demerger: The secured lenders have conveyed that they are willing to accord approval for Asset

Reconstruction with cross guarantees of the resulting companies. The Steps are being taken to complete all modalities as per lenders requirement.

GST: The effect of GST on the demand & prices of our products seems to be Nett positive for our business.

Gujarat Floods: There have been torrential rains in Gujarat leading to flooding in Mushroom section since 23rd July. We are taking all the measures to restore the operations and also assess the damages for filing the insurance claim.

I am grateful for all the support and blessings and request you to keep your trust in our capabilities to turn around and make Himalya a great food company of India.

1 Like

Most of revenue comes only from Mushroom operations, no visibility in improving the utilisation of existing production lines. Another solace is in entering in to Brazil markets for contract supply.