AGM was addressed by Mr. Jai Hiremath, CMDKey Highlights by Capital Mkt

In FY’15, while Pharma segment grew by around 13%, crop protection continued to remain under pressure and de grew by around 5%. Margins were under pressure in both the segments due to sluggish overall demand and uncertain raw material prices.As per the management, while Pharma segment should continue to do well, challenges on inventory and global demand continues to remain on crop protection business.Internationally, due to uncertain climatic conditions and lower food prices, the demand as a whole for the crop protection market is not growing. While every player is busy in gaining what so possible share that it can grab in a falling market, pricing becomes a challenge.

The management was not happy with the performance of Q1 FY’16, which was more or less flat despite the fact that in Q1 FY’15, there was a shutdown of plant and a loss of production of nearly Rs 25 crore. However, management is confident of improving on profitability going forward.The Pharma business definitely is on recovering note after seeing its challenges in terms of margins in FY’14 and in early FY’15. The focus continues to remain on volumes as it’s difficult to raise price due to tough competition that is prevailing in the market.

The Japanese MNC customer, for which the plant has got commissioned and trial production is going on, has commenced its commercial operations and the customer will contribute additional turnover of about Rs 50 crore. As per the management, there is surplus capacity with the company in crop protection business, which they will use it for the Rest of the Market other than US and EU. The Rest of the market slowly is picking up and will start contributing in a meaningful way in 3 to 4 years from now.There are no major capex planned by the company in next couple of years, unless there is some big opportunity from a new client.Thus, as per the management, while challenges continue in Crop protection market, company will be able to grab higher market share in Crop protection business in international market and new businesses will give volumes. For Pharma segment, the pricing is expected to remain stable and the company should be able to do better in terms of volumes.Thus it will be more of a volume led growth going forward in a scenario where pricing is uncertain

HIKAL LTD

Cmp: 156 market cap: 1279.04 cr.

Hikal has a hybrid model which is in pharmaceutical and crop protection business. Both the business equally constitute to the revenue of the business. The company allocates 3/4th of the capital in the pharmaceutical business and 1/4th in the crop protection business (source business segment). Company has growing its revenue at 10.22% since 5 years where as the company profit growth is in negative by 17.34% since 5 years on standalone basis (Mainly due to higher R&D expenses).

Pharma business has been growing at a pace of 21% Q on Q basis while 6% on annual basis. Due to higher R&D expense pharma segment is showing lesser profit compared to the sales. They have been deploying cash in this business.

Crop protection business has been growing at 6% yearly while profit has been growing at 10%. In this business model they provide Crop Synthesis and Contract Manufacturing of Agrochemicals, Intermediates, Biocides and Specialty Chemicals. Preferred Suppliers to Top Crop Protection Companies.

R&D updates

The company has various molecules in the various stages of phase 2 and phase 3. They have been deploying R&D for internal pipelines to Developed processes for several molecules using enzyme technology & validated two green enzymic process technology for major AIP products. 3 patents for novel routes to AIPs filed. Several significant Phase 1 and Phase 2 projects in the development pipelines. First manufacturing potential for a project in the flavor and fragrance sector.

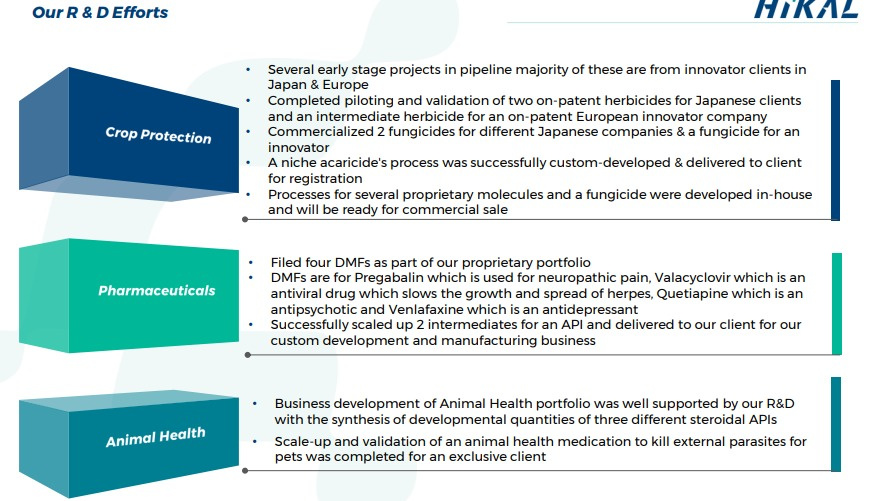

Under crop protection R & D, major project comes from innovator clients in Japan and Europe. They also have commercialized an insecticide for an innovator company and they have completed process development for an on-patent herbicide for another innovator client

In pharma segment, they have some product coming off-patent shortly and are under various stages of development are Sitagliptin, Dabigatran, lacosamide, olmesartan and Darunavir

In Animal health segments, they have completed the development of a topical parasitic used for dogs and cats & a veterinary medication to kill external parasites for pets for a mid-size company. They have completed process development & first pilot plant campaign for a regulatory starting material used in Oral flea and tick treatment for dogs.

In Contract development, they have completed the first pilot plant campaign for an intermediate of a non- regulatory starting material used for an oncology product under development while second pilot plant trails are under discussion with the same biotech company. The process development and two pilot plant trails for a regulatory starting material used in the treatment of ventricular systolic heart failure has been complete. Process development has been completed for an intermediate in phase 3 trials for a Japanese innovator company used for a treatment of chronic constipation.

Financials

Equity is 8.2 crores with 4.1 crore outstanding shares of 2 RS each

Promoter holding 68.77%

Long term debt of 296.6 crore and short term debt is 171.9 crore as of 31st June 2016. Company has Cash and bank balance of 19.2 crore and short term loans and advances of 44.3 crore.

Year 12 13 14 15 16

Sales 707.81 660.42 829.21 871.85 925.7

Np 46.03 25.25 63.90 40.41 40.5

EPS 28.01 15.36* 7.77 4.92 5.02

Dividend 6 6 4.5 2.5 2

*in 2015 the company has split from Rs10 to Rs2

Investment Thesis:

Company is under two business mainly in Pharma and Crop protection business where they manufacture contracted drugs with in-house R&D.

Mainly they use to have long term supply agreements in 2000s and then they shifted their allocation towards Animal Health care business and crop protection business and have started acquiring R&D companies.

They have been deploying cash into pharma business and they have been steading their crop protection business.

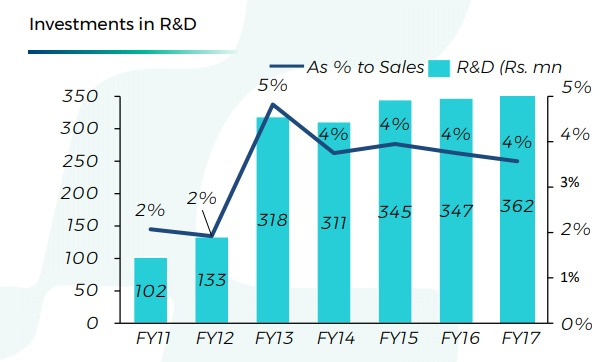

Their R&D expense is 4% of their sales. ROE is between 10-18% for last Five years.

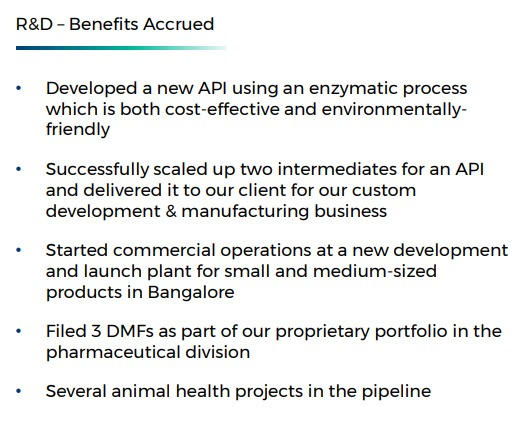

Nearly all projects in R&D has been completed next phase of R&D project is left in pharma business. They would Validated an API product using Enzymatic technology developed and will start manufacturing soon. They would be filing 4 – 5 DMF’s every year and will continue to generate own IP through Process patents

They have an average of 20% payout ratios but their D/E ratios is 1.28

Based on valuation the company is trading on 30.61 PE based on FY 16 EPS of 5.02.

Based on the company’s projects they can be a growth story of 20 – 25% on Revenue and profitability of 25%

Risk

The patent approval gets delayed

Higher debt to equity ratio is a concern which is eating profits so their interest coverage ratios is low.

Any cancellation of contracts will hurt their future growth

Technical reasons:

A cup and handle is formed where handle is 15 and cup is 40 points

Disc- not invested

Revenue:

221.23 Crores June 16 quarter vs 191.48 Crores June 15

Profit:

10.96 crore June 16 quarter VS 1.83 Crore June 15

Cash EPS

3.50 June 16 VS 2.21 June15

Eps:

1.33 June 16 VS 0.22 June15

Key points:

- During the June 2016 quarter, exchange loss of Rs 1.36 Lakhs (june15=6.12 Loss) on foreign currency working capital loans includes, unrealized exchange loss for June Q 16 is of 77 lakhs VS 5.37 Crores

DISC- invested

Hikal sells property at raise funds for business operations

Hikal Ltd has informed BSE that the Company’s API and Intermediates manufacturing facility located at Jigani, Bangalore was recently inspected by the US FDA in compliance with their requirements. At the end of the successful inspection, the Company have been informed by the Investigator that “zero” 483 observations were issued. This was a routine inspection by the US FDA.

FY17 Audited Financial Results

Net Sales crosses Rs. 1,000 Crore

EBITDA of Rs. 197 Crore; Margin of 20%

FY17 Audited Financial Results

PAT of Rs. 67 Crore; Growth of 62%

Total Dividend of Rs. 1.2/‐ per share (60% of FV); including 30% interim dividend

FY18 Q1 Results: http://www.bseindia.com/xml-data/corpfiling/AttachLive/cd2f147f-f5e3-4266-ad75-6d5f53cb8fdf.pdf

Hikal – Annual Report Key takeaways

One of very few global and only Indian Company to provide APIs for both Pharmaceuticals and Agrochemicals – Hybrid Model.

Total revenue has grown by 9.5%. Its segments include:

Agrochemicals - Out of which crop division segment grew by 15% (aided by increase in volumes of existing chemicals – a good sign for robust demand of company products and launch of new chemicals)

A large contract manufacturing project for a leading innovator client was completed and successfully commercialized.

Diversification into biocides and speciality chemicals will also help in future growth .

Sales of Thiabendazole –one of the biggest crop protection products – showed marginal growth this year.

A new state-of –the –art plant at Mahad has been commissioned for one of the leading global innovator customers. Given the successful commercialization of this complex project, their client is considering them with the additional production of an intermediate for this product.

They also commercialized two on – patent herbicides for a Japanese innovator company. Commercial production was successful for both these products and volumes are expected to increase significantly from the next year.

Product Pipeline - Two new insecticides and two fungicides that are expected to commercialize soon.

Pharmaceuticals – There has been an erosion in prices of major products but volumes will increase from hereon and also cost improvements strategies are taken. Also there will be developing new products, expand capacity and debottleneck existing one. (so may be this division will not enjoy historical margins very soon but may see some growth)

Hikal plans to invest further in the intermediate facility (Panoli) and convert this facility into an API plant that will cater to both the generic API and CDMO business.

This year, filed 4 DMFs and 2 CEPs. No observations in recent US FDA inspection at Bengaluru which is a big thing seeing lot of large firms getting observations.

Innovation required to win in long term, such as biopharmaceuticals growth aided by antibody derived drugs.

The biggest drug in 2016 was Humira (AbbVie) with ex-factory sales of US$16.1 billion (+14%). The top 10 drugs in the world represented 25% of the entire market. On a cumulative basis, the best selling drug ever remains Lipitor (US$ 152 billion).

As per management, earlier outsourcing activities were largely driven by the desire to reduce cost. It has changed significantly. Improving quality and efficiency, gaining competitive advantage and operational or technical expertise, and reducing the risk of supply shortages are the main business reason for outsourcing. In 2017, outsourcing should focus on specialized technologies.

The contract & Development business was down in terms of value grown as some of the contracted projects volume went down and some of the expected projects were pushed to the next financial year. A long-term contract manufacturing agreement with a European innovator client to exclusively manufacture molecules commercially gained momentum last year.

In the case of Pregabalin for which a DMF was filed in 2014, although the global product launch is expected in December 2018, revenues are gaining momentum with an early launch in the European Union and other semi-regulated markets where the products is off- patent.

Hikal will file DMFs with novel processes having identified six to eight new products for generic development. Company will file five or six DMFs to develop a health of commercial APIs every year.

Animal Healthcare – Company invested further to increase the capacity for one of our products that goes to an animal health company. It will accrue significant revenues in 2017-18 as the capacity goes up by over 50%.

The evolution of new diseases offer untapped opportunities for the animal healthcare market.

Scale-up and validation of an animal health medication to kill external parasites for pets was completed for an exclusive client. They started the financial year with only four clients in this segment and have been able to increase the client base to 10. With more expected in the coming years.

Financials

Company has taken steps for management of working capital, instituted strict norms over the last year which have shown result in the form of lower net operating working capital days as compared to the previous year.

Exports for the year are RS 6612 million (65% of total sales) as compared to RS 7317 million (79% of total sales) in the previous year. There have been diversification of customer base which includes more local customers who in turn re-export our manufactured products.

The median remuneration of employees of the company during FY2016-17 was RS 429750. In the financial year, there was an increase of 8% in the median remuneration of employees;

Rs in million Rs in million

Expenditure on R&D 2016-17 2015-16

Total R&D expenditure as a percentage of total turnover 3.57% 3.75%

(In Crores) Mar-15 Mar-16 Mar-17

P&L statement

Sales 871.85 925.65 1013.94

Sales % Growth 4.89 5.81 8.71

Net profit 40.51 41.32 66.79

Net Profit % Growth -58.1832 1.96031 38.13445

Balance Sheet

Borrowings 547.14 504.95 506.19

Other Liabilities 327.24 320.24 300.94

Cash & Bank 13.69 19.16 16.47

Net Block 639.35 623.18 668.33

Capital Work in Progress 61.66 66.13 62.76

Cash Flow Statement

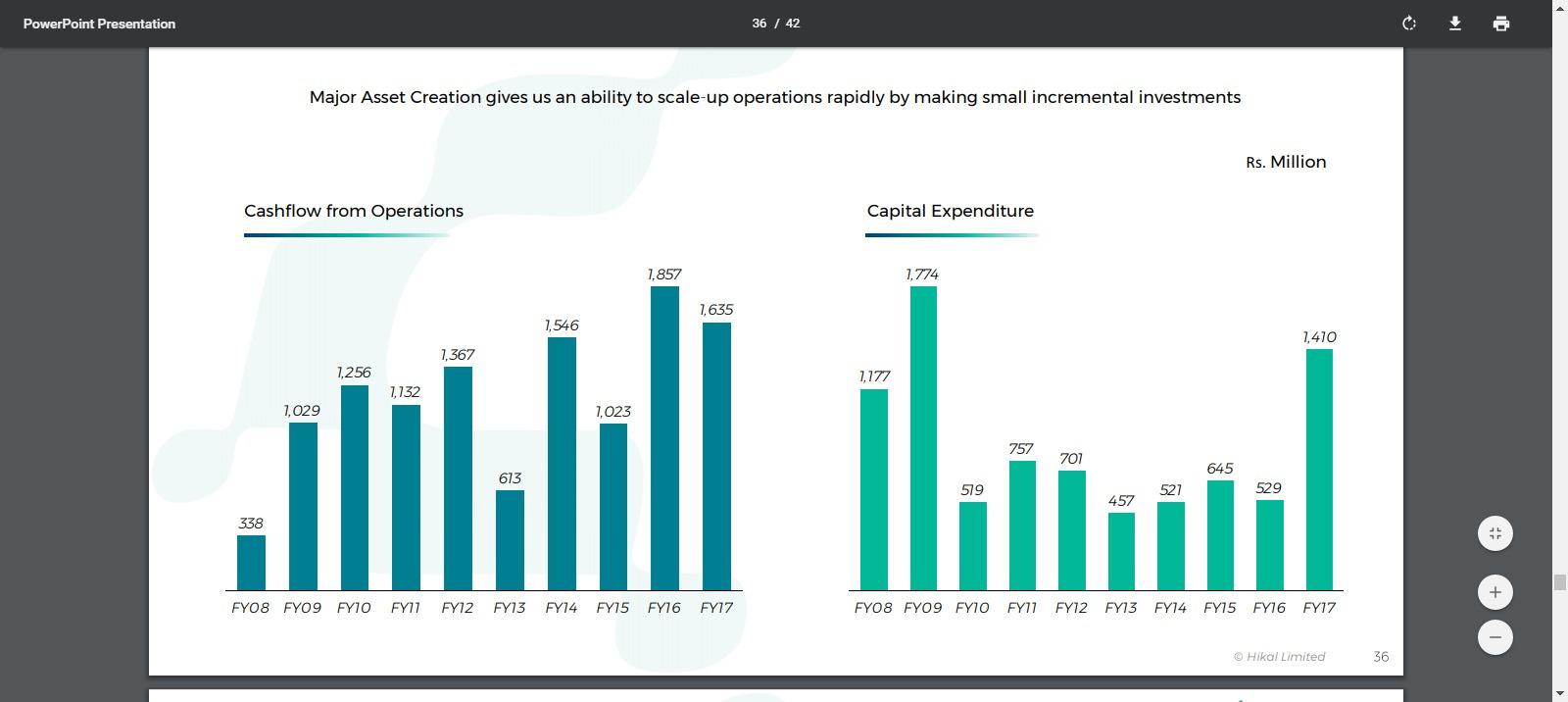

Cash from Operating Activity 102.27 185.7 163.49

Cash from Investing Activity -43 -64.07 -102.59

Cash from Financing Activity -68.82 -123.56 -63.27

Net Cash Flow -9.54 -1.92 -2.37

Quarterly Number (in Crores) Jun-16 Sep-16 Dec-16 Mar-17 Jun-17

Sales 221.23 232.31 250.84 309.56 262.71

Sales % YOY 13.45 12.19 4.16 6.39 15.79

Net profit 11.54 15.24 13.2 27.43 13.32

Net profit % YOY Growth 84.14 68.37 5.98 18.88 13.36

Operating Profit 43.59 47.07 48.89 57 49.67

Operating profit % YOY Growth 16.66 16.93 6.05 -4.53 12.24

Total foreign exchange used and earned:

Used : Rs 3304 million (Previous year Rs 2734 million)

Earned : Rs 6612 million (Previous year Rs 7317 million)

The holding company has the following subsidiaries:

a) Acoris Research Limited (India): A 100% subsidiary of the Holding Comoany.

b) Hikal International BV (Netherlands)

Divested property in Bengaluru which was lying vacant , and cash transferred to reserves which made balance sheet strong .

Maintained EBITDA at 20%. Reduced overall cost of borrowings through upgrade in credit rating and also there is further scope for it.

Technical

How much money they got from the Vacant Bengaluru R&D Land

Oct 17 : Investor presentation:

Q2 FY18 Results: http://www.bseindia.com/xml-data/corpfiling/AttachLive/90492b40-069d-447e-9d9a-ed1e965bda01.pdf

Flat bottom line

With highest sales in last 5 qtrs, 56.5% rise in PBT from last 4 qtrs average & highest operational profit in last 5 qtrs company has delivered seemingly good result. Would request experts to provide their comments/feedback on the recent result

Brief history of Hikal -

Years 2008-13 were marked by high operational income and good EBITDA margins; but this good performance at operational level didn’t reflect in bottomline. Couple of reasons i can think of -

- Debt fueled expansion resulting in high interest costs (rising from 16 cr to 66 cr in 5 years),

- Losses from derivative contracts (combined losses for 5 years ~89 cr),

- Acquired EU subsidiary write-off (60 cr) due to 2008 meltdown,

- Higher depreciation (non cash item, though).

Therefore, despite topline growing from 480cr to 700cr, PAT was in sorry state - (in crs) 47, 40, 7, 37, 46 from 2008-13 respectively. Meanwhile, gross block almost tripled from 380cr in '08 to 1000 cr in '13 meaning consistently high capex during this period. So, big investments were being made to get the company future ready and to develop a good API pipeline.

Now, here’s a note on R&D expenses over the years -

Hikal has significantly pushed up R&D in last 5 yrs. Almost 35cr/yr! Now, what riches has this increased R&D bought to Hikal? Not much in terms of stock gains or tangibles, obviously. But if we consider intangibles, this has moved the company onto a completely different trajectory, effects of which will be visible in next few years.

From 2015-17, Capex has almost been around the same level as depreciation (except for 2017-18). So, Net Fixed Assets is almost stagnant. Interest costs have come down from 68cr to 45cr though debt has not come down (580cr → 560cr), which means rate of interest has come down considerably during last 4-5 years.

D/E is consistently improving in last 10 years. Similarly, CFO have improved and are much more consistent in last 4-5 years.

Management’s competence is beyond question with the presence of many eminent personalities in top management and Board of Directors (Kalyanis, Hiremaths, Dr. Wolfgang Welter, Dr. Axel Kleemann).

Some huge tailwinds are there in CRAMS/API business at the moment. Here’s a note from Neuland’s annual report.

!Global Animal Healthcare market to grow at a CAGR of 4-5% over next decade to reach USD 55b+

— UnseenValue (@unseenvalue) March 30, 2018

Can #MakeInIndia, the LOWEST-COST destination in #pharma manufacturing be ignored for long? Think!!

Long runway ahead of ethically led, R&D focused, cGMP approved biz #lollapalooza pic.twitter.com/EqxIm6XtFS

Persistent R&D efforts put in over last 5-6 years in developing their own proprietary portfolio, process development/research, scale up from lab->commercial should take care of the margins going fwd. Agro chemicals space is a big opportunity for India in my view. It is at a point where pharma was there few years ago. Here’s what Hikal management had to say on Q3’FY18 result -

Value Chain-

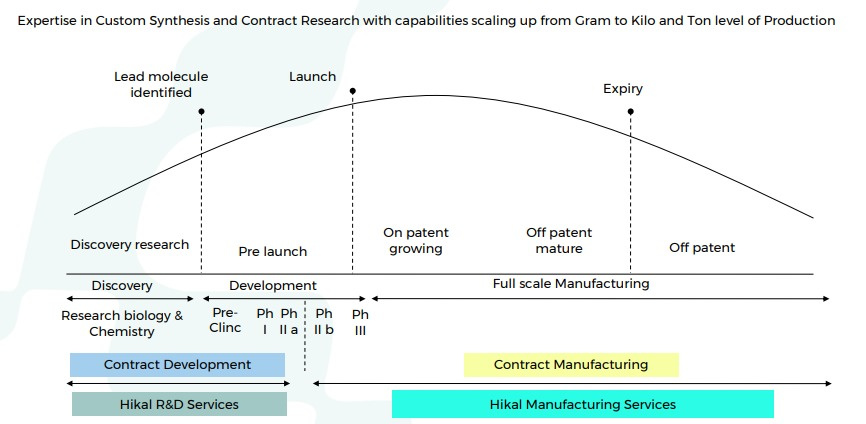

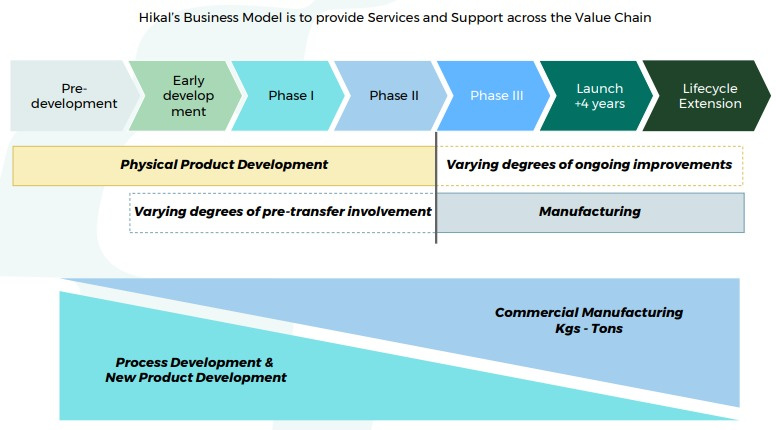

Good part is that Hikal is present across the entire value chain right from discovery, development, to full scale manufacturing. Aconis acquisition has provided them with state of the art R&D wing. Advantage of being present right from discovery (research) and development (clinicals) phase is that you get exclusivity once the molecule is commercialized. Margins are also much higher than usual in such relationships as you become extremely critical to your client.

You get many more chances to milk the drug life cycle (custom synthesis, contract manufacturing, process research, process improvement, patents, life cycle enhancement). Providers then get a better chance to expand with the client horizontally.

Moat -

High margins attract competition. But how difficult it is to acquire the capabilities and resources once someone is able to identify and analyse the sources of rival’s competitive advantage? Tangibles are relatively easy to copy; On the other hand, culture, processes, tacit knowledge and patents are not! In crams, providers become indispensables. CRAMS is an extremely sticky business as innovator / customer can’t so easily switch to another supplier after years of knowledge sharing & joint product development. That’s the moat!

Risks -

In CRAMS sector biggest risks are not regulatory, as weekly audits from MNCs / innovators are common. Real risk is losing your partner’s faith in your systems & procedures.

- IP leak (mindset of imitating your customer’s IP for self gain)

- Data integrity (GVK Bio)

Very nice post @Mridul! I’m also trying to understand this co better. It seems there were lots of expectations in past but the bottomline growth didn’t used to show because of the reasons mentioned by you but finally good performance has started showing up in recent quarters…if this sustains it will be good.

The stock seems to be under pressure in recent days due to selling by mutual funds which have a big stake.

On the risk side - it seems the prices of one of their key api had increased and hence growth looked higher…don’t know how sustainable the same is. Also a newer generation drug is getting better adoption.

Disc: invested

Some data/chart to chew -

Green shoots seen in Pharma segment (in Q3Fy18).

Pharma

Hikal - Anekal/Bangalore/Karanataka

API Pre-Feasibility Report

http://www.environmentclearance.nic.in/writereaddata/Online/TOR/12_Nov_2016_122356800124YQMBWEMPReport.pdf

Expansion: Gabapentine, Bupropion, Cinnarizene, Ondansetron, Acebutalol

New Products: P-Benzyloxy Aniline, Ondencetron API, Oxypentifylline, Triprolidine HCL, Gemfibrozil, Decoquinate, Levetiracetam, Verapamil, Valproic Acid, Sodium Valaproate, Di-Valproex Sodium, Magnesium Valproate, Topiramaten, Tertiary Lucin.

Date of EC Granted : 16 Feb 2018

Source: View Form A Part I

Crop Protection

Hikal - Mahad/Raighad/Maharashtra plant

Modernization project of Manufacturing of Pesticides, Insecticides & Fungicides

http://www.environmentclearance.nic.in/writereaddata/EIA/241020174SIHOF0QCompleteEIAreportHIKAL-.pdf

Expansion: Diuron, Benefuresate, Benzophenaf, 3 5 Dichloroaniline

New Products: Clothianidin, Trifloxystrobin, Azoxystrobin, Thiacloprid, SMPGM, Fludioxanil

Date of EC Granted: 15 Jan 2018

Source: View Form A Part I

Disc: On radar. No investment yet.

Rightly said, bottomline growth never showed up due to various reasons. Have been tracking their quarterly release. Please see the attached file. Believe 2016-17 AR gave lot of indication and numbers are also showing up accordingly but management was positive in the past as well but never delivered numbers. Attached file might help

Hikal-VP.xlsx (13.9 KB)

Discl: Invested

Good job assimilating numbers along with mgmt commentary at one place @kunal_patel. Helps understand ups and downs of the business and how mgmt guided through time.

I went through the whole excel. I feel management has been pretty much accurate in bringing forward what’s aiding and what’s haunting them qtr by qtr. For instance, their crop protection business was hit by destocking and industry downturn in 2015/16. Pretty much every company in this sector was hit at that time for the same reason.

They have been pretty accurate in projecting offtake (sales) (as i said in my earlier post, sales has not been an issue for this company, margins are!) with the introduction of new products. Margins most of the time were hit due to higher RM costs, plant shutdowns, destocking, pricing pressures.

Management commentary started turning very positive starting Jan 2016 (Q4 FY16) as capex was to come online in 12-18 months, R&D spending was starting to pay-off, introduction of new products, expanded teams, improved client base.

Overall, i feel they have been doing a decent job. There are things like RM cost pressures or cyclical downturns which are not in their hands. Though, with the introduction of newer products, increased geographical presence, emphasis on R&D, development of own product portfolio, timely expansion of facilities, great regulatory track record, they have now built a very good pipeline. R&D efforts are starting to pay-off in both pharma and crop protection segments.

I believe knowledge based business trajectory is like that of Hikal. Takes time to take-off, but once it does take-off, things can skyrocket.

Hikal Banglore expansion - (Project cost ~80 Cr)

- These API’s & Intermediates are used in the manufacture of medicines, most of which are life saving Drugs. The demand of such products is tremendous in India and abroad and there is a huge gap in the demand and supply chain. The market of these products has a fast progressing growth and there is ample opportunity in indigenous as well as export market. The project is envisaged to meet the demand supply gap in both domestic market and export market, as API demand is increasing day by day.

- Hikal’s Banglore plant was initially set up a API manufacturing unit with a capacity of 1388 MT/pa along with by-products. Hikal has added new API (Bulk drug and intermediate) at this existing plant. Additional production will be 3439.3 MT/pa (total volume of 4827.3 MT/A) along with by-products of capacity 6622.4 MT/A + 68406 MTPA Solvents by products.

Hikal - Mahad/Raighad plant modification (Project cost ~107.92 Cr)

- Modernization project to manufacture Pesticides, insecticides & fungicides

- Present production capacity is 993 MT/month.

- Modernization involves change in product mix. Considering prevailing market condition company proposes to reduce some of the existing products by 506.33 MT/M while some of the existing products will be increased by 265 MT/M. At the same time new products will be introduced by 130 MT/M. Hence, modernization project will have total manufacturing capacity of 881.67 MT/M. In addition Hikal proposes to introduce 84 MT/month pesticides formulations at same location. Total byproducts are expected to be increased from 828.78 MT/M to 1350.78 MT/Month

Noteworthy - Fifty percent of Hikal’s business has evolved from custom synthesis projects, which start from gram level and rise to multi ton supplies.

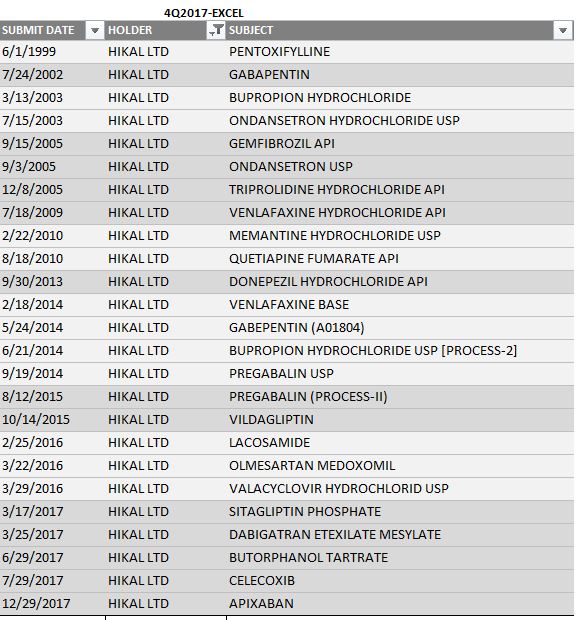

In CY16 and CY17, Hikal filed 8 out of 25 total active DMFs currently.

Enjoys dominant position in Gabapentin API business. Around 30-35% market share. This API has been a significant contributor of Hikal’s pharma revenues as of FY17.