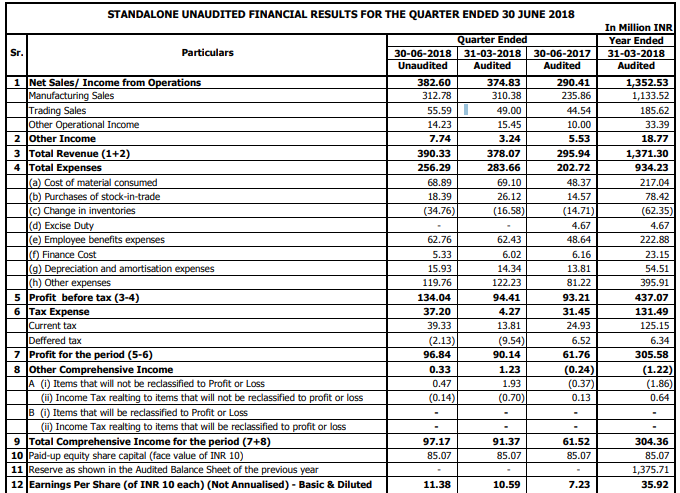

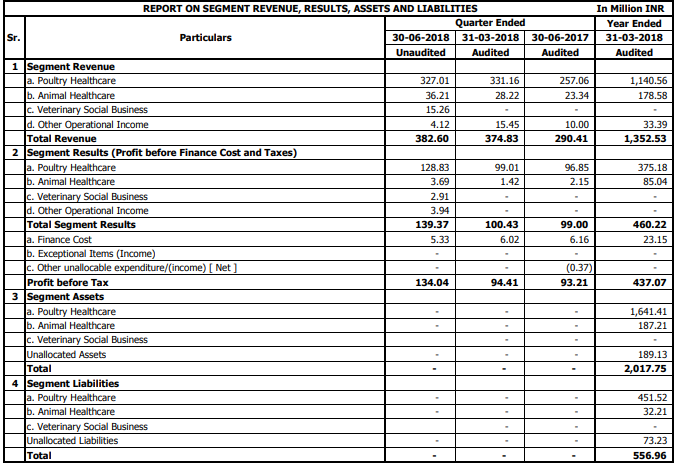

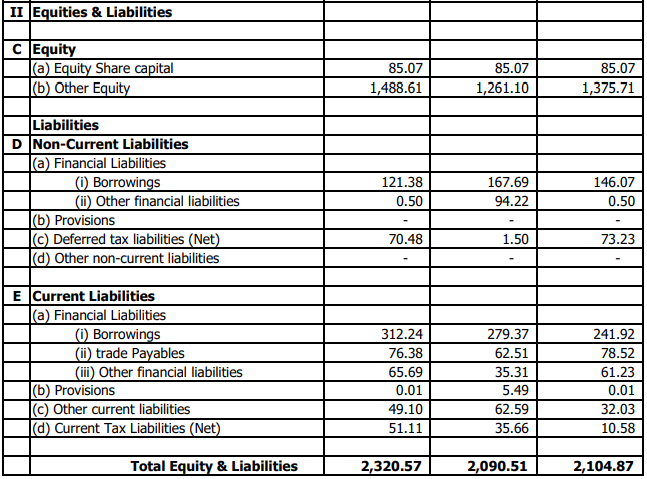

Q1 FY19 results: Strong growth across all segments

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0a640d31-07eb-40e3-b2bf-de8379790229.pdf

Q1 FY19 results: Strong growth across all segments

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0a640d31-07eb-40e3-b2bf-de8379790229.pdf

Revenue up 34 % YoY

OPM revived back at 38% this quarter

PAT increased by 56%

Both Poultry and Animal segments have shown good growth YOY . Animal segment witnessed a growth of more than 50% yoy.

Overall very robust results

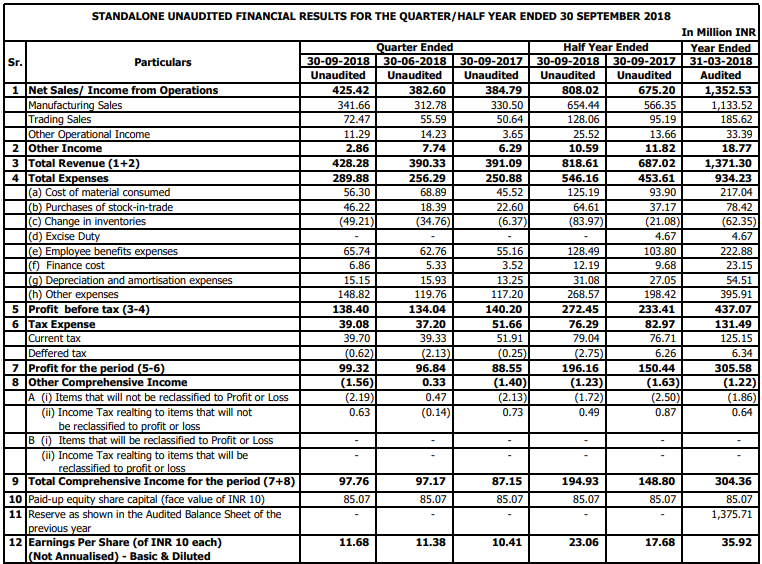

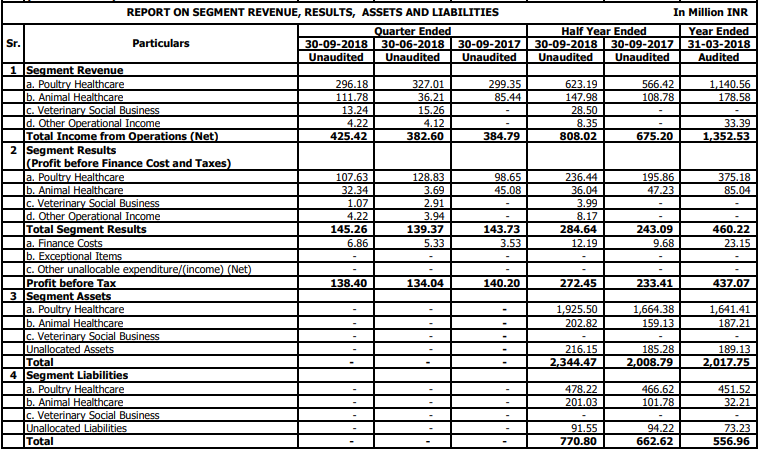

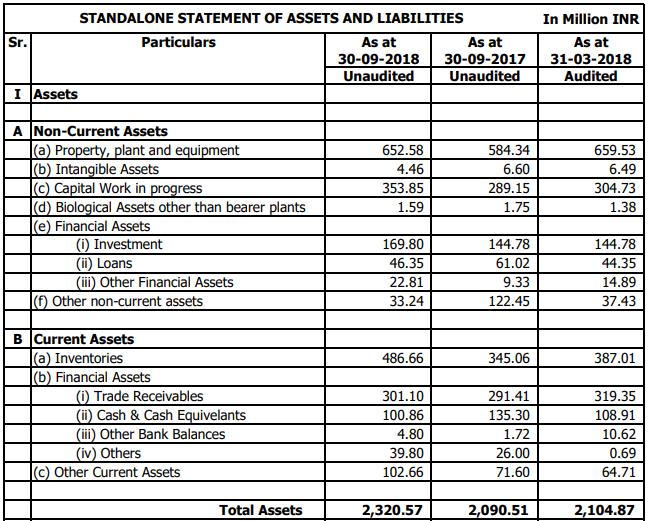

Q2 results:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0e90e45b-856e-4b94-9d40-1c3a16fdf2a6.pdf

What do you make of the results? Result analysis please?

Hester Bio Earning Call transcript Q2/H1 FY19

This piece about declining meat-eating habits among millennials maybe relevant to the long term demand of vaccines:

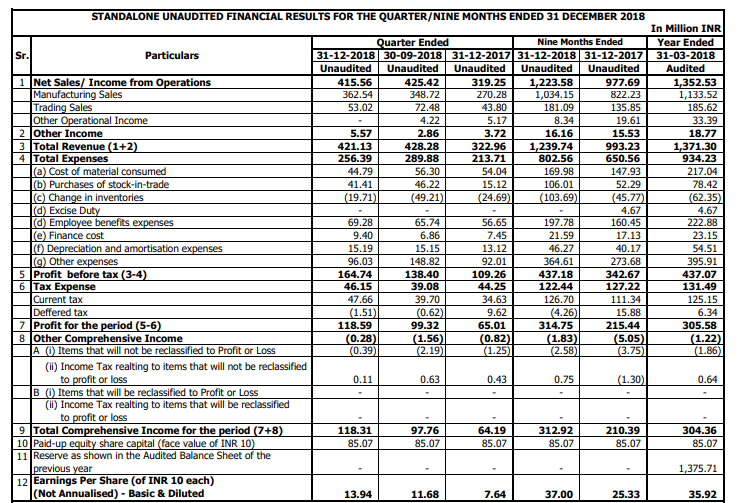

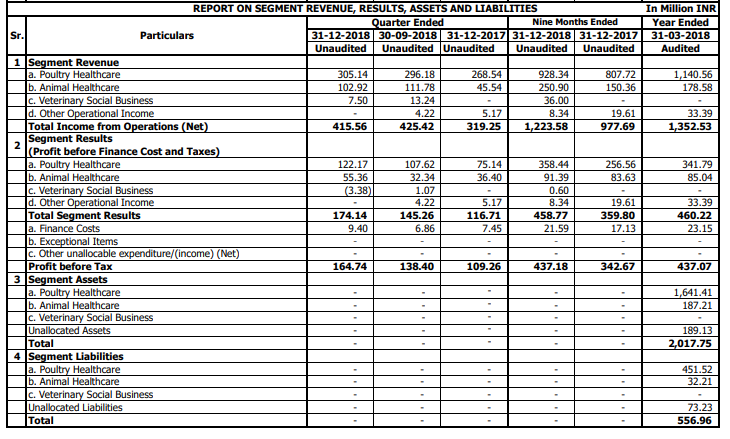

Hester Q3 Results - https://www.bseindia.com/xml-data/corpfiling/AttachLive/0cc903ed-e5d1-411d-8958-965eb6202279.pdf

Transcript of earning Conf call held on 29th Jan 2019.

Press release on Q3FY 19 and 9M FY19 results.

Hester is into poultry vaccine manufacturing (domestic ~35% market share) and in last few years has diversified to animal vaccines, poultry health products and animal health products. Product portfolio comprises of over 50 vaccines and over 35 health products. Exports to 9 countries with registration process on in over 20 countries. Founded in 1987 by a first generation entrepreneur.

Hester has multiple growth drivers ahead (long runway ahead) -

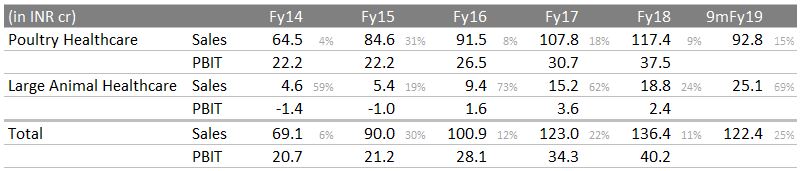

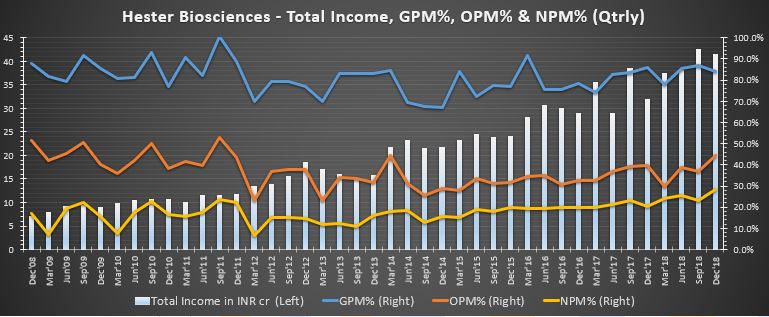

Some data and chart to chew -

Disc: Recently invested; no transaction in last 30 days.

great results by hester as usual.

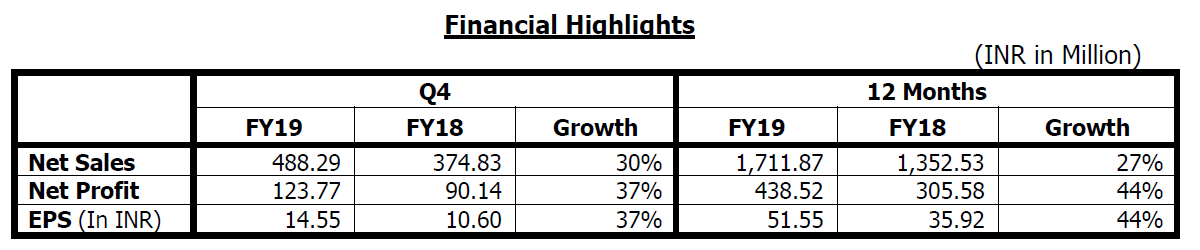

Q4FY19 Results: Sales up by 30%, Profit up by 37%

FY19 Results: Sales up by 27%, Profit up by 44%

India business

Poulty healthcare showing a decent 14.5 % growth in q4 , from 33.1 cr to 37.1 cr

Animal healthcare showing great growth at 268 % on a small base, from 2.8 cr to 10.3 cr.

Q4 FY19 CONCALL NOTES:

Key learnings for the company from past two years has been not to completely depend on govt tenders, single location or product/division.

Implemented those learnings in FY19. Poultry division contribution to revenue is down to 26%(from 91%),animal health division contribution increased to 21%.

Overall all the divisions shown good growth,Hester focussed more on animal health division.

International business did not grow as expected due to external headwinds like registrations of products, distributors…etc

Hester India: Domestic business was good and compensated for low growth in export business. Capacity of Hester India expanded by 50% at existing plants. (Gross Block for standalone India business increased to 100 Cr from 65Cr).

Lot of opportunity in animal and poultry products to utilise this capacity.

Veterinary social business: good progression in Bihar and UP states. Even though we grow rapidly, revenue is less but we get good visibility for Hester products. We will be extending this to other states in India and plan to do same in Nepal and Africa once we are well established.

Animal health division: growing at 50%, for FY20: 50% growth guidance.

Growth is lead by tender business in vaccine and private market in other products. 50% of animal division revenue is tender based, rest 50% is from pvt market.

Our team is educating farmers to use vaccine/other products. Most of the state govts promoting use of PPR and brucella vaccine.

Gaining market share from others as we have less than 10% share and our penetration is not deep in certain states. Lot of opportunity for us to grow further. (Virbac and zydus are two big companies with 400Cr turnover).

Poultry division: 10% growth guidance for FY19.

Poultry division growth in last year mainly by increase in volume.

Texas life sciences(TLS): Revenue of 8 Cr vs 1.4cr…net profit at 50 lac. 86% of revenue is from sale to Hester against 65% in fy18. Hester has 55% stake rest is with existing promoters and they are doing good job. Most of our animal health division products transferred to TLS.

Hester Nepal : Revenue grown to 9Cr from 1.4Cr. EBITDA margins at 49% against loss in FY18. Net loss of 3Cr v/s 7Cr in FY18. Accumulated loss of 12Cr.

Few PPR vaccine tender started coming but not as expected. We have got few tenders which helped to growth nepal business. Most of the revenue is by exports.

Nepal revenue split: Domestic 10%.International business: 70% tender and 30% nontender.

Appointed local distributors/sales network and focussing on domestic sales in Nepal.

Expect PPR vaccine sales to increase. If we get tenders we can do 20-30 cr business.

Nepal business will turnaround for sure.

Hester Africa(Tanzania plant):100% owned by Hester India. Plant construction under progress as planned. Expect commercial production by end of 2020.

Tax exemption for 10 years.

Turnover expected up to 200 Cr at peak utilization.

We are focusing on pvt market of Africa than depending on tenders.

Product availability till last mile was problem in Africa.

Market size is much bigger than Nepal. Tanzania and Ethiopia has large animal population.

Hester Tanzania Pvt ltd creating own distribution network to reach small farmers.

Main reason to set up plant in Africa is to make vaccines which are not allowed to make in India or Nepal plant. Only PPR vaccine is duplicate for both Nepal and Africa. Remaining products are specific vaccines for Africa.

R &D : 3 Cr in FY19 (7Cr fy18) R&d focused on developing new vaccine and improving efficiency of current vaccines to reduce cost. Additional 2-3 product possible in FY20.

Disclosure: not invested.

Note from the CEO & MD on the Government of India’s initiative to immunize animals against Brucella Disease

About Brucella disease (Brucellosis)

Besides having a positive impact on Hester’s top line, this initiative by the Government of India goes in line with Hester’s objective - Better health for human beings though healthier animals.

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/da427177-7e2e-4352-a440-4cbe323ac37d.pdf

Co presentation (new): https://static1.squarespace.com/static/584173905016e1ca1b9c2115/t/5cf5eff9efc0ff000123a1a5/1559621674757/Hester+Presentation+INR+Mn.pdf

Hester Bio Q1 FY20 Results.

Blogpost on Hester

Investor communication from Hester:

Dear Shareholder, Stakeholder:

Subject: Exports from Hester Nepal; With reference to articles appearing in news on UN’s financial situation

Many of you have forwarded me articles which talk about The United Nations running out of money. Some have expressed a concern.

Your reason to forward the articles or to express this concern is due to the fact that you have a feeling that our Nepal plant is dependent on FAO tenders for PPR vaccine. Such a situation at UN, in your minds, could hamper the business of Hester Nepal.

While surely hoping that FAO starts floating PPR vaccine procurement tenders, please note that we are already working on models wherein we have no dependency on a product or a geography or on any specific tenders. We are working towards ensuring that our business forecasts and objectives, more so at Hester Nepal, are met at the earliest.

We have already started to market the Hester Nepal’s PPR vaccine through our country distributors, through the private market channels.

Besides this, you would be pleased to know that the following channels are additionally being used to derive business from our Nepal plant:

Country tenders: The worldwide PPR disease eradication program is in any case in place. Quite a few countries have started floating tenders for buying the PPR vaccine directly. It will be our attempt to win such tenders.

Manufacturing and marketing of poultry vaccines within Nepal: While having got the manufacturing license, we have recently got market authorisations for quite a few poultry vaccines which are manufactured in Nepal. We are creating a strong marketing and a distribution network within Nepal. Our endeavour is to make Nepal self sufficient in poultry vaccines.

We have received the manufacturing licence for the Classical Swine Fever vaccine, for which registration is on-going in a few South East Asian countries. This vaccine has a good demand in that region.

Situations change, towards which actions have to be taken to ensure that we continue our progress towards our objectives.

Hester Nepal is on the right track, may be temporarily at a slower pace, but we are confident that we shall reach our goal to make Hester Nepal as well as Hester India as sources for animal vaccines, across the globe.

Going further, this endeavour, in any way, does not compromise our objective to maintain our profitability.

Sincerely

Rajiv Gandhi

CEO & Managing Director

Q2FY20 Sales down by 3%, H1FY20 Sales up by 4%

Q2FY20 NP down by 12%, H1FY20 NP down by 6%

Business Overview

Hester India

Q2 and H1 results have been below budget due to the following reasons:

A. Both divisions were impacted. In the Poultry healthcare division, high maize prices continued

to impact the poultry industry. In the Animal healthcare division, while the trade business grew

by 25% in Q2, purchases by various state governments has got delayed. Going further this

year, the poultry industry has already started showing signs of recovery. Government

purchases for animal vaccines should go as per forecasts, to be completed before the end of

the financial year. Current trends of both the divisions make us believe that we shall reach our

Q3 and Q4 targets.

Page 2 of 3

B. Due to increase in working capital cycle, our finance cost increased. Extra credit days have

been given to customers but with great diligence. With the industrial scenario improving and

our sales picking up, we hope to get back to the reduced working capital cycles.

C. In order to go aggressively in the market, recruitments in the marketing division were done,

mainly on the technical sales side. Sales results would be visible in the coming quarters, thereby

reducing the personnel cost-to-sales ratio.

While the top line for the financial year would be impacted due to lower sales in Q1 and Q2, we are

confident of recovering our margins, thereby assuring our profitability ratios.

Hester Nepal

More Details under

Board meeting intimation for fund raising through equity dilution

Not sure of the fund raise objective but appears negative on first glance. Screener shows company hasn’t diluted equity in 10 years.

Thoughts?

Late post as I saw the management interview a month back and sharing the answer here anyway. This is an enabling resolution to raise 150 cr through equity dilution at an opportune time if and when any potential acquisition materializes

The company had done it in the past as well - so not really a negative.

Disc: Invested