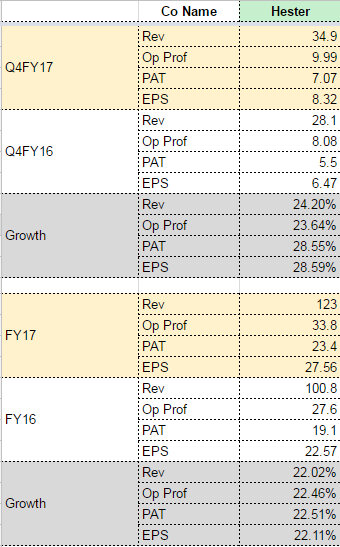

I was expecting better numbers from Hester. The tax outgo is lower and hence PAT and EPS look high.

Large animal business showing a small operating profit. Nepal hasnt commenced operations yet. Export numbers were a disappointment.

I was expecting better numbers from Hester. The tax outgo is lower and hence PAT and EPS look high.

Large animal business showing a small operating profit. Nepal hasnt commenced operations yet. Export numbers were a disappointment.

Summary of my notes from the Annual Report - 2016

• Cumulative production capacity of 6 bn doses once the Nepal capacity goes online

• 2015-16 performance was achieved despite a 6-month trough in India’s poultry sector that affected the sector for 3 quarters. The trough was the result of high feed cost and low realization of poultry output of meat and eggs. This resulted in a lower replacement of chicks.

• Started trial production of two batches in its Nepal plant and submitted these to regulatory authorities in 2 African countries

• HBS has decided to make a strategic shift to health products over dependence on poultry products

• Focus on exports to de-risk company from exclusively depending on domestic market

• Poultry Vaccines Segment: Introduced two Poultry Vaccines namely the Salmonella Live Vaccine and the Inclusion Body Hepatitis Vaccine

• Large Animal Vaccines: started manufacturing and marketing of large animal vaccines. Currently, manufactures PPR and goat pox vaccine. The Indian plant at Mehsana produces the PPR Live vaccine strain meant for India (sungri strain); the Nigerian strain will be made in the Nepal plant for export markets

• Brucella abortus S19 vaccine will be commercialized this year

• Large Animal health Products Segment: Comprises of medicinal products, feed additives & disinfectants. HBS does not manufacture products themselves. The outlook for growth is robust and can outperform the other divisions in the near future.

@basumallick What’s your view on valuation at current market price? As I had bought it at 389 and then sold it @586 since then very much skeptical about valuation.

The Nepal plant will be operational from Nov 15, 2016. The volumes may pick up from Q4. Valuations are on the higher side (as of now & in my opinion). It can remain at these valuation levels if the earnings come through.

Disclosure: I am invested and not selling at this price.

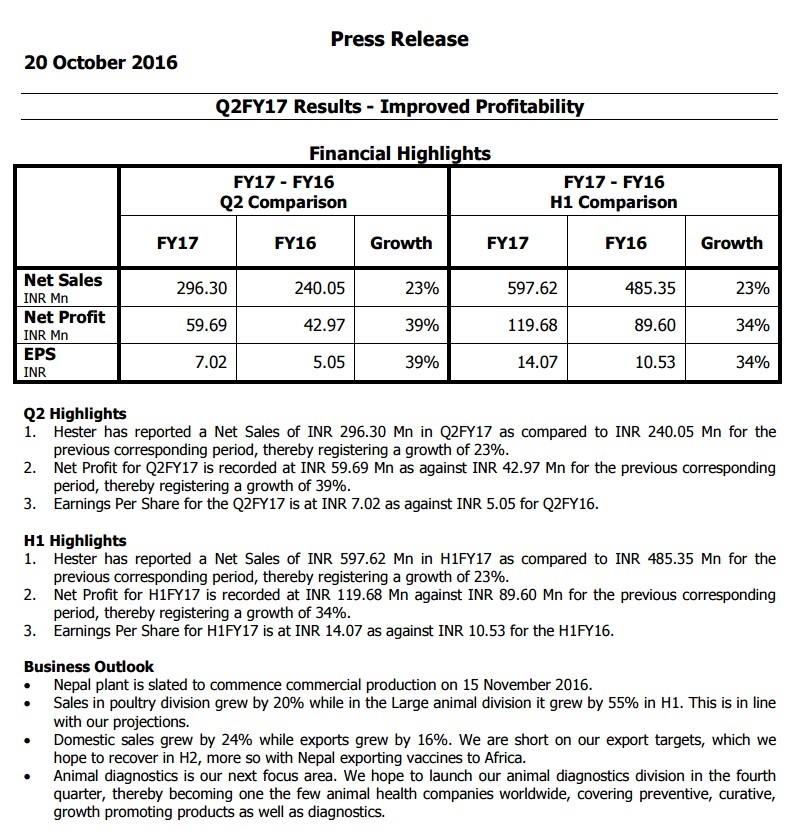

Oct 20, 2016: Q2/H1 FY17 Conf Call Highlights

• The exports have been a bit slow in the first half, but we have reasons to believe that we should pick up in these exports in the third and the fourth quarter.

• The Nepal plant which is now slated for firm final commercial production on 15th November 2016.

• Already got an order through FAO for supplies in Africa which would commence the sales for the Nepal plant

• Launch the Brucella vaccine in the next 45 days

• Already got batches tested at the Central Testing Laboratory in Africa which is a common testing laboratory for the whole of African continent for PPR vaccine

• Started our own diagnostics division wherein we will manufacture diagnostic kits at our plant in Ahmedabad and we will do our own marketing and distribution in India besides looking at toll manufacturing opportunities with international companies

• Orders of 3.5cr in hand for Nepal plant. Margin profile to remain similar to get slightly better for international orders.

• Working capital days has drastically reduced to 64 days

• Tax rate to be at similar levels as the co falls under MAT and is getting incentives for R&D capex

• R&D spend till now of 4 cr. Part of this is capitalized and does not go through P&L.

• Total consolidated debt is 56 cr

Hester Bioscience’s long/ short term credit ratings by CARE were upgraded from “BBB+” to “A-:Stable”

http://www.bseindia.com/stock-share-price/hester-biosciences-ltd/hesterbio/524669/

Management Discussion & Analysis (MDA) Snippets - Hester Biosciences Limited

About Hester Bio

Hester Biosciences Limited is an India-based company engaged in manufacturing of poultry vaccines and large animal vaccines, and trading of poultry health products and large animal health products. Its segments include Poultry Division and Large Animal Division. It provides over 40 products across poultry vaccines (live and inactivated), large animal vaccines (live and inactivated), health products and diagnostics. Its product range includes vaccines, drugs, feed supplements and disinfectants.

Key Products and Segments

-Poultry Vaccines (87%)

-Large Animal Health Products (7.40%)

-Poultry Animal Health Products (3.43%)

-Large Animal Vaccines ( 2.17%)

MDA Main Triggers

Industry Overview - Global Veterinary Market

Industry Overview - Indian Veterinary Market

Sectoral Optimism

Corporate Optimism

Current Financials (FY 15 - 16)

Sales stood at 100.8 Crs

EBIDTA stood at 33.07 Crs

PAT stood at 19.23 Crs

EPS at 22.60

Current Financials (H1 FY16-17))

Sales stood at 58.38 Crs

EBIDTA stood at 20.36 Crs

PAT stood at 11.97 Crs

EPS at 14.07

Valuation

At cmp 730, the stock trades at 24x expected FY17e EPS of 29.64. We suggest that buy around 650 with the PE around 22x Fy17e.

Management Guidance

What to Watch out for in Earnings

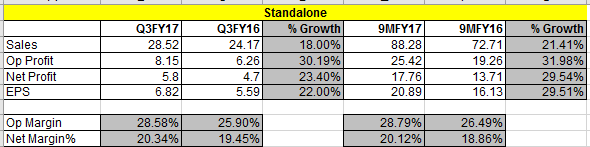

Q3 2017 Results:

Business Overview

Short Summary of Q3 conference call:

we have also prepared few other summaries. Sharing here: https://goo.gl/5RTk0o

Great job Saket. We need such novel initiatives particularly for small and mid cap which are not as frequently or widely covered.

Saket,

It really is commendable in preparing summaries of conference calls. It gives information to all investors that missed such management interactions. But just wanted to share with you Hester uploads its transcripts of calls on their website. I have copied the link to their website. Hope this is helpful.

This is absolutely brilliant! really appreciate your hard work. Thanks a lot for this.

There is a recent interview of the promoter where he mentions the company does not have plans to raise capital in near term. He will be financing his expansion through debt.

Q4 FY17 Results

Dividend of Rs 2.30 / share declared.

Business Overview

Nepal plant

Transcript of conference call is out

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/328ba87d-d30b-406b-9af3-046c96b064cb.pdf

Q4FY17 concall summary:

Poultry vaccines which grew at 19%, the large animal division grew at 61% against our earlier forecasted of 50%. On the export side, we grew at 44% though we had estimated a growth of 100% and on the domestic sales side, we grew around 21% better than our planned or budgeted growth.

Exports were lower than expectations as registrations are not in our hands and took longer than expected. We hope to grow at 100% next year. Second issue on export is our PPR business - which has been slow to pick up. Somewhere middle of this year it may pick up.

We expect large animal business to grow 50% next year.

We had committed and planned to launch the diagnostics division in the fourth quarter of the last financial year. There has been a little delay in that and the diagnostics division would be launched within a month’s time that is in Q1 of this financial year. We hope that this division settles by Q2-Q3 from where we would start generating sales. profitability in this division should be reasonably better than the average profitability of the other divisions. By Q3 we should have a trend ready based on which forecasting can be done.

We have been more focused on profitability and keep strict check on working capital and better production planning.

On the Nepal front as you are aware, end of last calendar year we started our commercial production, we had by that time also won a tender which order also we have executed. We are now focusing on additional tender business as well as the domestic sales from the produced at the Nepal plant. This also would stabilize shortly in this first or the second quarter and we should comfortably be able to take the sales and distribution activities further.

On international front, our focus remains to be in for Africa in this financial year and in this year we should have developed a strong distribution network mainly in Eastern Africa and then going further to Southern part of Africa and then to Western Africa. The whole distribution network, etc. would be in place in the next 3 to 4 months which is actually it is already functioning but when I say in place, I mean additional resources to be pooled in towards making it more robust than what it is, not that it is less, anything of it less at this point of time, it is just that we want to make deeper penetrations into the African market because the registrations which we are getting are coming on quite reasonably fast at this point of time. We have also got our other vaccines tested in the African Union Laboratory for supplying in the African continent. So these activities are well in place.

R&D spend is about 6% of turnover. We would continue spending 6-8%. We aim to roll out thermostable PPR Vaccine this year. In Africa there is good opportunity for this.

Internal target is for 30% growth for FY18.

Asset turn improved to 1.5 times vs 1.4. Inventory days down to 97 vs 120. Receivable days down to 78 vs 94. Overall working capital days down to 66 from 107.

Dividend of 5.3 resulting in payout of 18.15% as per policy.

We have invested about 15 Cr towards creating an additional capacity for inactivated vaccines, which should go on stream in September or October in this year in 2017.

We have registrations for most of the countries in Africa however we need more product registrations to push sales.

We are looking to churn more out of the capacities already created before doing next major capex.

The big ticket items PPR, Brucella which are now very strong for us. They definitely would be the growth drivers as far as the large animal division is concerned and besides that on the large animal health products side, we have planned to launch around 30 products in this financial year. These products could include it could be medicines, it could be feed supplements, it could be disinfectants. So, this is the range that we are really trying to launch within this financial year.

We may do 10 Cr from Nepal.

PPR tender size are from as low as 20 lac to as high as 7,8,10 or 12 Cr. Depends on Country.

Top Vaccines - In terms of value in poultry, live vaccine Gumboro would be number one. In terms of doses, Newcastle disease would be number one. IB Vaccine would be equal to Gumboro in no of doses but value is less.

Besides tender business, we have made immense big inroads in LA Vaccines throughout the country. For international tendering, we are the only co with Indian and Nigerian strain.

We as a company want to use Africa as the base for our growth. So, we are putting, we are creating our own infrastructure, our own distribution, we would definitely be probably the only company or may be one of the only companies, I would say the only company being a manufacturer having its own distribution network. Other cos have distributor in SA. Now how does this translate into business is something that we have to work ourselves.

Given the opportunity we should at least have, we could very easily have one of the vaccines or between Brucella and PPR we could cross more than 150 crores very easily. These are conservative nos, anyone can read the documents that the opportunity is of $15 Bln for next 15 years. In India Govt has 2 disease eradication programs Brucella & PPR. Put together we could do 100 Cr.

We are not looking to do QIP. May need only if we have some opportunity of very fast growth in business.

2020 Vision - We want to be 8-10 times bigger but it will be bottom line focused.

Vaccine is something it is a preventive medication which has to be given irrespective whether there is an outbreak or not an outbreak.

How do we get the strain - Getting the seed virus is not the issue, the issue is producing the vaccine.

I thought Rajiv Gandhi was trying to tamp down expectations now that the company is more than 30 times P/E even he estimated future growth at around 23-25 CAGR.

Happy with the progress of the company