For me dividends are important, this company seems to have not given one for ages

They have paid their loans back which is good but I prefer a bit of gearing specially as interest rates are low

Why should the company only risk equity money and not some debt

I worked as a CFO for a lot of companies and in these times there is nothing like financing growth with debt

An Internet cover above 7-8 times of earnings doesn’t make sense

This company decided to protect their bases instead of returning some dividends and financing growth with loan

Not impressed but the sector is something I like because as more Indians and Chinese get rich the demand for meat will only increase

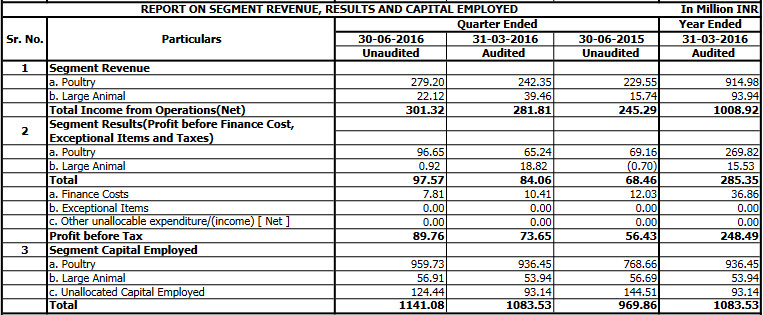

FY16 results announced

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/19EBA839_284F_4543_BFB0_3E552214AF3F_115207.pdf

Points to Note0:

Large Animal segment has posted 100% increase in revenues (9.394 cr v/s 4.355 cr). It also turned profitable with EBIT at 1.553 cr @16.5% margin.

Consolidated EPS at 22.20 v/s 15.98

Other Announcements:

Hester Biosciences Ltd has informed BSE that the Board of Directors of the Company at its meeting held on May 07, 2016, inter alia, have recommended final dividend of 11% that is INR 1.10 per equity share for the financial year 2015-16, subject to approval of members in the ensuing Annual General Meeting.

Further, Ms. Nina Gandhi has been appointed as alternate director of Mr. Ravin Gandhi in place of Ms. Priya Gandhi, who has resigned as alternate director of Mr. Ravin Gandhi with effect from May 07, 2016.

Further, the Board of Directors has decided to appoint Link Intime India Private Limited as its Registrar and Share Transfer Agent in place of Sharepro Services (India) Private Limited.

Disc: Invested.

1 Like

Pretty good set of results. It seems they have got some revenues from the new vaccines they were launching for the large animal segment. It would be interesting to hear the concall scheduled on 9th May at 2 pm (dial in no 02267468363)

Negative - It seems the Nepal plant hasn’t got commissioned yet.

Regards,

Ayush

2 Likes

Hester had launched PPR and Goat Pox vaccine on March 18.

http://www.business-standard.com/article/markets/hester-biosciences-surges-10-on-launching-ppr-and-goat-pox-vaccine-115031900166_1.html

PPR vaccine was in news recently due to an outbreak in Georgia and other east-European countries.

Peste des Petits Ruminants now present in 76 countries, Eradication campaign being formulated

Georgia recently reported its first-ever case of Peste des Petits Ruminants (PPR), a viral disease which is capable of severely impacting goat and sheep populations, while a new outbreak has occurred in the Maldives, showing that even island states are vulnerable to the plague.

The outbreak in Georgia, near the borders with Armenia and Azerbaijan marked new territory for the disease, which is particularly lethal upon contact with unprotected animals.

Experts from the Food and Agriculture Organization (FAO) and the World Organisation for Animal Health (OIE) recommended control measures including vaccination of 800,000 sheep and goats. Quarantine zones have been created and surveillance of animals in adjacent regions intensified.

The outbreaks — coming on the heels of similar episodes in Western Turkey and mainland China — underscore the risks posed by a virus that can kill as many as 90 percent of the animals it infects within days.

FAO and OIE map campaign to stamp out a virus that kills millions of sheep and goats each year.

Concall would indeed be an interesting one.

1 Like

The other side to look at this Nepal plant not commonsing is that it is giving us another opportunity to enter in this stock because otherwise with such good number and also Nepal plant commonsing, the stock might trade much higher.

Any news from conference call?

Bloomberg Interview on Q4 results

Conference Call - Self captured notes:

- Healthy growth was seen in all the four business segments of the company. The poultry segment went through a tough time in Q2 and Q3 of the year in reference. The management did not deviate from their focus on the bottom line. This was achieved by improved product mix and product range.

- Disease eradication program by GOI will be a big boost to the sales of PPR vaccines going forward.

- Poultry vaccine has been the revenue earner for the company. Along with the large animal vaccine a combined growth of 6% was seen.

- During the last year, the company introduced 2 poultry vaccines which was projected to have a sales of Rs20mn , however the company could only do a sales of 7mn. There are four large animal vaccines in the pipeline for this year.

- The sales in the poultry divisions grew at 6.4%.

- Division for Large Animal has shown a growth of nearly 73.2%.

- Domestic sales grew by 6% while exports grew by 73.6%.

- The company has been progressing well with their R&D. R&D expenditure for the year was around Rs51mn and is expected to be around Rs90mn in FY17. The company intends to spend on the recombinant vaccines. Going forward, the focus would be on animal diagnostic. Hester has already manufactured 5 types of diagnostic kits and looking into 3-4 more of such diagnostic kits. These kits are for detection of poultry or cattle diseases. Currently trials are going on and will commercialize these in this financial year.

- As a result of this, the company will be able to match international standards and at par of having three segments of vaccines, healthcare products and diagnostics.

- Trial production has commenced at the Nepal Plant. The commercial production would commence from August 2016.

- Capex was around Rs64mn, which was planned to be around Rs150-Rs170mn, however not materialized due to market condition and smart management decision to improve the bottomline, so the capex was postponed. This year, Rs190-Rs250mn will be spent as Capex to increase the capacity of some vaccines which are already produced by them. Apart from this, the management also intends to add a small facility for manufacture of health products- medicines, disinfectants etc. This will also be to match upto the international standards for facilities as required by international norms.

- Exports grew at 73.6%, which had an increase in sales to Rs100mn from Rs57mn in the previous year. Management intends to grow the exports to 100% on y-o-y basis for the next 3-4 years and exploit the opportunities on the domestic as well as international front.

- During the year, company has made investments by way of equity in associate company namely Leruarua Vetcare (Proprietory) Limited to the extent of Rs0.68mn.

- The company hopes to grow the large animals business at 50%, poultry business at approximately 15% and exports at nearly 100%. Overall the management expects to growth at 20% in this financial year.

- Overall a healthy growth was seen in the company’s ratios. ROCE was at a healthy 20.4% as compared to 17.02% last year. ROE grew at 19.6% as compared to 16.6% last year. ROI was 12.1% as compared to 9.3% last year.

Other Highlights

-

In Poultry alone, there are around 44 different vaccines and 126 SKU’s. Some of these SKU’s had small batch orders which caused inefficiencies. Working capital improvements were made by trying to rationalize the varied product range. Used the recession as an opportunity for focusing on bottom-line improvements. Also there was a change in product mix.

-

Brucella vaccine: Potential Indian market size is Rs700 mn. In great demand. Planned to be introduced between Sep-Dec along with 3 other large animal vaccines.

-

Salmonella + IBH: Potential indian market size is Rs40 mn and company is confident of garnering 40% market share. Introduced in July.

-

On Tendering business: Only vaccines have a tendering mix, while Health Products are commercially traded. 1cr out of 85cr in Poultry vaccines were tender. 1.7 out of 2.3 cr were tender in Large Animal vaccines. Government-related debtor days varies from 5 days to 90 days. But it is 100% secured.

-

Exports revenue mix: Out of 10 cr sales, Poultry contributed 8.5 cr of which 75-90% were vaccines. Remaining 1.5 cr was Large Animal (health products)

-

Dosage capacity of Nepal plant is 1.2 billion doses, Not sure if it is total capacity or only for PPR (which i had asked for). I think it is overall capacity.

-

Mgmt said Q4 margins can be considered as steady-state margins going forward with respect to Large Animal segment.

-

Exports did not contain any Large Animal vaccines orders.

-

Only a small order of PPR Vaccine was done in Mar 16. It was the Indian strain.

-

Company had ongoing inspections as part of the license registration in the African countries. Proceeding as per schedule.

-

Cold-chain Distribution network in Africa: Continuing to put things in place. Currently working with a few partners, But long term plan is to have own distribution network.

-

No opportunity loss in Global FAO Tender for PPR vaccination program due to delay in start of Nepal plant, as it has not yet started. Mgmt believes there is an increased impetus within FAO to start the program in mid-CY17. In fact, management stated that it has received a small order which will be executed as soon as Nepal plant is operational.

Nepal Plant:

- Capacity utilization will be approx. 20% in FY17.

- Full capacity utilization will contribute Rs500 mn.

Diagnostic Kits Division:

-

Main Target customer is for Small Farmers (especially wrt Cattle and Sheep) - Field Diagnosis and end-to-end services such as sample testing, etc.

-

Also work with Big Integrators/Cattle farms - Disease diagnosis programs which involve Zero Monitoring, Testing and Evaluation. While some of these clients have their own labs and hence Hester will sell only diagnostic kits.

-

Two modes of revenue

1 Direct Sales of diagnostic kits

2 Testing of samples in company’s independent lab located at Anand, 70km from Ahmedabad for a fee. Samples are tested, analysed and reports are sent to farmers. Currently the service is only for Poultry. Will be extended to Large Animals in future as well.

Update: Company uploaded official transcript to exchanges

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/11F3D22E_007F_4714_9331_215291F7F5CA_152113.pdf

11 Likes

Thanks for sharing your notes. It was good to see you on the concall.

Thanks Ayush.

It was my first one.

Was a bit nervous and also apprehensive since my voice is not clear.

Listening to it again on researchbytes, i felt my voice was fine.

Anyways, it was a test run as i have lot of questions for Take solutions concall on 12th.

2 Likes

Thanks @crazymama it was good listening on conference call. You have asked your first but I was little reluctant to ask . Anyways will ask in future. And BTW going by mgt commentary Hester bio is looking good for next three to four years.

hi,

Do you think the scale of opportunity is very large for this co and current market cap is too low agst the opportuniy size…?

Reema: Your domestic sales have grown faster than exports. So, domestic sales are up 21 percent, exports at 14 percent. Can we expect a further pickup in exports?

A: Yes, for exports we have projected to grow at approximately 100 percent on a year-on-year (Y-o-Y) basis for the next two to three years. However, for this quarter it has been 14 percent but we would pick it up in the second or the third quarter and we are very confident to grow our exports at 100 percent with Africa as our focus area.

Please use Mr Gandhi’s projections with a pinch of salt. He has a history of over promising and under-delivering.

Disclosure-- Invested in the stock

5 Likes

Hester Concall – 1 Aug 2016 – Q1FY17

My quick notes from the call yesterday.

Summary:

• Business growing in line with expectations

• 4 divisions – Main focus on growing 4 divisions to create equitable distribution of revenue

• Q1 FY17 – growth drivers are:

o Inventory management / credit control / product mix – improving profitability

o Introduced 3 poultry vaccines – total now at 49 vaccines

o Reduced costs through solar power installation of 100KW – will be increasing it to 750KW in 12 months based on efficiency tracked over the next Quarter

o Domestic grew 21% / Exports by 14%

Want to achieve 100% growth in exports

Expansion plans – started work in vet diagnostic division.

- Diagnostic kit for poultry and large animals

- Will launch by end of Q2 – waiting for a more robust portfolio

- Nepal plant complete – will inaugurate in the next couple of weeks

- More trial batches underway/ recently completed.

- Looking at Africa – setting up plans for our distribution networks. Waiting for activation. These will be Hester owned – focus on East African markets for now.

- Looking to expand into health products – right now dependent on 3rd party manufacturers. Want to bring this in house – will look to create their own manufacturing units for this.

CFO Highlights – Q1 FY17 Vs Q1 FY16:

Divisions performance

- Poultry Vaccine: INR 26.45 Cr vs INR 21.38 Cr

- Poultry Health Products: INR 0.79 Cr Vs INR 0.58 Cr

- Large Animal Vaccine: INR: INR 0.21 Cr Vs INR 0.02

- Large Animal Health Products: INR 2 Cr Vs INR 1.55 Cr

Combined sales

- INR 30.13 Cr Vs 24.62 Cr – Growth of 23%

- Export 2.70 Cr Vs 2.36 Cr

- Domestic 26.75 Cr Vs INR 22.17 Cr

- EBITDA @ 35.56% Vs 33.34%

- NP @ INR 5.99 Vs. INR 4.66

Balance sheet

- Inventory level at 97 days

- Debtors at 2.27 months

- WC Cycle at 70 days Vs 77 days

- FAT – 1.66 times Vs 1.49 times

- Invested 2.33 Cr in capex - Total earmarked in the region of 20 Cr for this year.

- ROCE @ 30.48%

- ROE @ 22.57%

- ROI @ 15.66%

- EPS - INR 7.05 Vs INR 5.48

Key Business Movements/ Highlights in the first Q

- PPR vaccine under registration in all African markets

- Energy costs will be reduced by about 10-15 Lakhs per quarter based on current 100KW solar plant. Plan to grow this 6 times – saving 90 Lakhs when (and IF) solar capacity expanded to 750 KW

- Forecast the business to grow 20% this year – margins sustainable. (This growth discounts Nepal facility according to Mr. Gandhi)

- PPR market size – based on FAO – US$7.5 Billion over 15 years (Globally)

- Size of tenders for PPR are typically small right now – because the process is starting

- Number of players that can bid for PPR – limited to 3 to 4, both in India and Internationally. (Indian manufacturers cannot bid for international tenders)

- Fund raising for 30 Cr Capex – Open to both debt and equity as a source. Currently 25 Cr limit sanctioned by banks. Also have board approval of 75 Cr QIP if the need arises.

- 30 Cr capex = 20 Cr New facility (health products) + 10 Cr to enhance existing production facility

- Capex on diagnostic will be 0 – facilities same as the vaccine business

- Market potential for diagnostic business – small in India / opportunities internationally are more. More than anything its product extension at minimal cost and allows Hester to offer a broader range of products to the same customers.

- For Nepal investment – debt repayment over 4-5 years. Amount of debt to be repaid – 21 Cr

- Large animal health vaccine in India – opportunity size is INR 50-60 Cr

All in all Hester looks to be focused on the right things with a good roadmap laid out. Rajiv Gandhi as always sounds positive and while I don’t doubt his capability I think the story will take slightly longer to pan out than he anticipates.

PPR continues to promise to be a significant upside when tenders begin to fructify.

Akshay

Disc: Invested - No transactions in the last 12 months

6 Likes

I am reading about Hester and following from AR FY15 caught my attention

The Company also received registration approvals

for 14 poultry vaccines in four different countries.

The Company cleared two international contract

manufacturing inspections from private companies and

ensured compliance with European and Japanese drug

regulatory standards.

I didn’t know they were into contract manufacturing. This is an interesting fact over and above their base business.

4 Likes

Below is my summary of reading a bit on Hester. Still work in progress as I have only done desk research. Will try to talk to some industry people to get a better idea. Reports by HDFC and Karvy are pretty good.

Capabilities

The company is into a niche area and doing well. It has demonstrated good execution in its business model. There is competition but not so many players. Eg of Hester’s capabilities and execution

* Good distribution network in India and Africa. This is very important for selling vaccines as they need to be stored at low temperatures

* Technical support to farmers- Leaders in offering such services to the Poultry industry. Avanti-like support.

* Biologics manufacturing technology is complex and very difficult to replicate, which is why there are only a handful of manufactures in India - Venky’s (no 1) , Indovax (no 3)and Indian Immunologicals are the only major manufacturers besides HBL. Today, if you really look at the manufacturers of the Animal Vaccines you would be able to count them on your fingers, probably a few more they would definitely not go beyond 15-companies. Most of them have merged with the big companies and therefore, the technology availability, the ability to get technology is going down day-by-day.

* First in India in Goat pox vaccine

* Clever in setting up PPR vaccine plant in Nepal

* Only 3 companies in India can make PPR vaccine. Other 2 are Indian Immunological (National Dairy development Board) and MSD. They claim that they are the only company in world that can make both traits of PPR. But my take is that maybe Sungri trait is not imp for companies to tap into because of the small size. They maybe focusing only on Nigerian trait by design

* Hester has developed a thermostable vaccine for Newcastle disease. The advantage of thermostable vaccine is that this vaccine can be stored outside for 10-days at temperatures up to 37 to 40 degree Celsius and vaccine would still be potent and effective. This is particularly important in backyard poultry because this poultry is in very remote areas and transportation is often not refrigerated. This vaccine is expected to have a huge demand in Africa.

* Hester has embarked on a project for immunising backyard poultry in India, against Ranikhet (Newcastle) disease, in collaboration with GALVmed, a Scottish NGO, which in turn is funded by the Bill Gates Foundation. From GALVmed flier "In India, GALVmed has teamed up with Hester to vaccinate up to 100 million chickens using the thermostable LaSota Newcastle disease vaccine. The vaccination will cover three states of Chhattisgarh, Jharkhand and Odisha"

* Industry asset turns are 1.2x (Source:Concall, but need to check) and Hester working for 1.5-1.6x

Positives

-

Expanding portfolio of products- Health products and diagnostics kits. Large animal health products is a big opportunity. All large global MNCs get majority of revenue from this segment, whereas Hester has just started here.

-

PPR exports from Nepal is a big opportunity of USD7.5bn. In 20 player market, assuming a 5% market share translates to 2400 cr. New players will come in but Hester can have a price advantage. Current capacity can do 50cr per year but management has said that this can be expanded 3x at the same site. Will also look at acquisitions in Africa to aid in marketing and distribution of PPR vaccine. The plant will have 10 year tax holiday.

-

International players have priced PPR vaccine at upto 10 cents per dose, as also mentioned in FAO/OEI document. Hester is selling in India for 2.5-3.5 cents.

-

Capacity utilization operating leverage from Nepal plant, which will produce Nigerian trait of PPR vaccine.

-

Doubled domestic inactivated vaccine capacity for international opportunities. Spent 17cr. Currently full utilization.

-

Current geographical reach is low. Export to overtake domestic business by 2020. Focus on Africa, west asia, southeast asia.

-

Future of vaccines- Hester is pursuing R&D to manufacture recombinant poultry vaccines, which HBL expects to patent in about 2 years. HBL believes that is the only Indian company right now working on a Recombinant Poultry Vaccines

Negatives

-

Management gives very aggressive guidance and has a track record of not meeting it. eg…1000cr turnover in few years. 200cr turnover by FY17 which was later changed to 120cr. Multiple promises of launches and certain revenues from vaccines which didnt materialize

-

I DONT treat delay in Nepal plant commercialization as a big negative…They faced problems of earthquake and then border problems. Plant is operational now.

-

As per concall “Availability of the strain in order to make these Vaccines, the companies are becoming fewer and fewer worldwide, there have been mergers and acquisitions in the last 15-years, and the big players have become very big. So the access and the availability even for the seed viruses have gone down tremendously. So this is also a very big barrier to get into this business.” Can this make it difficult to develop new vaccines?

Competition-

Europe accounts for the largest share of the animal vaccines market followed by North America. The market is dominated by multinational players with the top 5 players contributing close to 70% of the global market. The top 5 players by worldwide sales in 2014 are:

- All large MNCs biggest revenue comes from Large animal health while Hester case is opposite so it can grow alot.

- Indian poultry vaccine market- Top 3 ( Venky, Hester, Indovax) have 80% share, rest MNCs. Gap between Hester and num 3 is huge.

- In Large animal vaccines- Indian immunologicals is (only?) competitor in India

- Large animal health companies in India- Zoetis, Virbac, MSD. Zoetis prices its vaccines at same level as others in India

21 Likes

Nice Detailed Post Rohit. How Will Diseases like Bird Flu & any other similar diseases in future will effect Hester ! Is it an opportunity or loss ? Considering that many poultry farms could not be in a position to afford the vaccines when these diseases spread and will resort to culling !! Poultry rates fell down to INR 90 / Kg few years back with bird flu.

Why Nepal was considered for new plant ? Landlocked ? And this is export oriented product unit. Any African Country could be a better bet.

India rejected Nigerian Strain PPR production due to fear of its spread and doesn’t it hold good for Nepal, if not now in future ? Any one incidence of its spread in sub-continent might effect Hester ?

The new plant is built for mainly for PPR tender business in Africa, What is the fall back incase the tenders outcome is not positive for Hester ? Is there retail market for Nigerian PPR in Africa ?

These are my priliminary apprehensions.

2 Likes

Fantastic post and summary, @pikrohit! Having been following and invested in this company for sometime now, I have been impressed by the long term journey of the company - they started as traders for big MNCs in mid 90s and are today one of the largest producers of vaccines in India. Going forward if one looks at their plans etc, they are making efforts to expand the product range, enter animal health area (which is the bigger segment for all the MNCs) and get more revenues from exports. So the steps are logical and if executed well, they can do pretty well. However, the management has promised a lot in past but delivered lesser or later.

Regards,

Ayush

4 Likes

Here is a text from 2007 AR

The poultry industry has now stabilised, which was earlier under stress due to the Bird Flu outbreak in February 2006. The industry growth rate is back in double digits, this time with a higher focus on hygiene and disease preventive measures. The use of poultry vaccines has gained lot of importance as a tool to prevent diseases.

Even if you look at results in 2007, the revenues were flattish. Eventually these things are a temporary blip and the industry would rebound very fast after the disease is controlled. In fact, Poultries had a tough time in 2016 also. If you read AR and concall transcripts, management said that the year was the toughest in last 10-15 years and costs of operation for poultries were 20% below selling price. But the industry has recovered now.

Nepal was selected because of Nigerian strain cant be manufactured in India. Geographical proximity to India and 10 year tax break may have played a role. Africa could have been an option but it may not be easy to go to a country that you are not so familiar with. That said, Hester is planning a green field plant in Africa, but it will come only they have clear visibility of utilization at Nepal.

Nepal doesnt have a large cattle population. So PPR spreading would not be a big risk. If it spreads, Hester opportunity size will only increase.

PPR vaccines are also needed in countries other than Africa. South east asia, middle east etc. The opportunity of PPR is enormous and Hester with approvals in place shouldnt have problems getting the tenders. They probably have one of the lowest cost structures, and also good distribution network. So I dont see any reasons why they wouldnt grab some portion of the pie.

They are also working with non tender business, although volumes will be small. This has been mentioned in concalls.

@ayushmit absolutely…the company is making the right moves. This is a case where we shouldnt rush as there could be disappointments (compared to commentary) on the way, providing better opportunities to buy.

6 Likes