Of course it can, but the first is presently happening while the second is a future possibility.

Also, the competition in higher cc segments is not just Bajaj. It includes Honda, Yamaha, Suzuki, TVS and many more

Hi guys

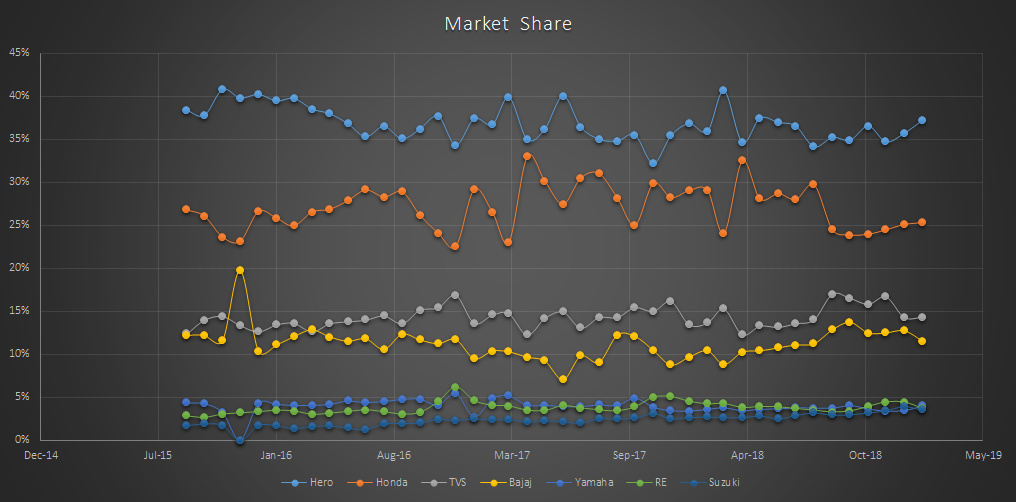

Just wanted to share some facts on sales figures as there seems to be a consensus that Hero is losing market share rapidly

Looking back from Diwali 2015 onwards here is the actual trend. Some pointers below.

- On a TTM basis from Nov 2017 Hero has always had ~36% market share which is its mean market share for over 40 quarters. Whereas both Honda and Bajaj have shaved off a percentage or more of market share in overall 2 wheeler sales in the same period.

- Having said that FY19 will be a comparatively poor year for Hero as it will lose overall share to Bajaj and TVS (the same for Honda, infact Honda will lose even more market share from FY18 to FY19 than Hero)

- Hero had higher share of ~38% in 2015-2016

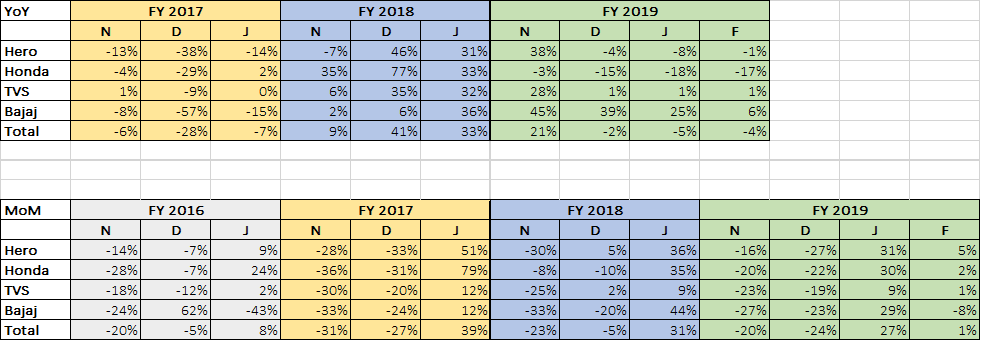

- On a YoY basis in Dec 2018 Hero had a 4% drop in sales compared to 15% drop in Honda’s sales. Similar number for Hero in 2017 and 2016 were 46% increase and a decrease of 38% respectively.

- Similar numbers echo for MoM.

edit: news just came in that Hero posted their March 2019 numbers at an abysmal 581279 units, that is a ~21% drop YoY. For FY19 they have grown a mere 5.6% compared to 11%+ in FY18. I think this is the worst March numbers in 5 years or so.

Rgds

disc: no investment in 2 wheeler segment.

5 Likes

We need to see how Bajaj has done. Will be interesting to see how it shapes up with BS6

Dec QoQ sales were down for HH, Bajaj and TVS. I do not think when sales are going down across the board, any one company is taking another’s share if its sales have reduced lesser. None is succeeding, its a bad year for all.

It is when the market is conducive, and one who clocks more sales counts as market captured.

Agri and textiles, are two sectors which employ the maximum number of people in India, and both sectors are showing depressed numbers due to demonetization and have barely recovered since.

Villages and small towns are biggest markets for 2 wheelers, therefore the sales of our companies are dipping. No surprise there.

I think HH is the better company of the lot, due to its branding and wide spread dealership channels. The current situation will be a great opportunity to snag the stock at a good price for the very long term.

2 Likes

As per my limited knowledge, the listed M&M is only automobile/tractors business…pls correct me if wrong

When I last tracked M&M, defence was not part of listed entity. Pls correct me if wrong. Thanks

I was tracking auto shares charts and comparing Bajaj to hero. These are cyclical businesses but charts so far do not truly reflect that. Hero’s chart looks more secular with some hiccups during recession (when all businesses suffered) and more of stagnancy now than a true cyclical dips as seen in cements oils metals etc. So far I would not rate them as true cyclical…although Ford’s of the world would present the risk this business might present at some point of time…not denying it’s not cyclical but it’s variables are little more deep and difficult to understand than pure cyclicals…and probably that’s because of the consumer touch…

Anyways, one thing I do not understand is the huge dip in Bajaj stock in 2008 09 recession as compared to rather stable hero stock…any idea on that?

And if anyone can list down the variables affecting this cyclical business? Interest rates, financing cost, monsoon for rural, cost of steel, crude etc…none of which I feel has a direct Deep impact…exactly why is this slowdown…and if it’s a cyclical downturn then why stock is still reasonably valued…why this is not a consumer durable business, what makes it different from say a Prestige or Whirlpool…is what I am thinking when I have started tracking it sincerely now. Thanks

1 Like

They have subsidiary for all others. Please check annual report/website.

The current issues will only be exaggerated next year. Liquidity crisis at HFC and NBFC due to NPA was the first stage. Even Maruti Suzuki is facing the heat.

Heromotocorp’s positives are it’s market share overall, market share in economy segment, growing share of scooters and it’s dealer network.

It’s negatives are a dated product lineup and lack of exciting products. Those looking at an Enfield, Jawa, Dominar, Apache or KTM will never consider a Hero.

But the question is what %age of people in rural belt of Northern India think about Dominar, KTM etc vs a Passion or a Splendor.

As for the lineup, I think entry into the 125 cc scooter (with Destini, Maestro doing well) and premium motorcycle segment (relaunch of Xtreme, Karizma etc) takes care of that.

As investors we should trust the brand & give some bandwidth to the mgmt to make these new efforts work out. In my opinion, external issues are plagueing the industry as a whole coz of which prices are depressed. Makes for a good time to add more of historically resilient players.

3 Likes

A lot of disruption coming towards the auto industry in few years.

Yes there is alot of disruption. But the technology is not a closely guarded secret.

End of the day the differentiator might very well be the service penetration and distribution of the company.

People might end up paying a premium for bajaj or hero simply because they will want strong post sales support. We cannot simply look at a company based on products, especially products that require high degree of post sales support and service such as automobiles.

It may take years for a new entrant to reach the scale in terms of support and distribution of that of a bajaj/hero in India. I think an electric Splendour or an electric Pulsar or Bullet will have more appeal to the customer when/if it happens in the distant future.

It will be interesting to see how bajaj/hero/eicher handle this imminent change in the industry.

3 Likes

Hero is an investor in Ather Energy: https://www.atherenergy.com

TVS is an investor in Ultraviolette: http://www.ultraviolette.com/product.html

1 Like

Hero Motors like Eicher and Maruti is giving a good chance to buy the stock at the support level. Unless there is more pain in the buying, we should see the support level hold. I am buying in SIP mode.

KKP

2 Likes

For Hero, aligning to the impending disruption is a couple of acquisitions away. In fact, it will be a great opportunity to take lead in capturing market share, of the new market. It is in plenty of cash, and can easily take lead as soon as the management has clarity.

Maruti is not buying the EV argument. They don’t see it as cost effective yet. Same goes for bikes. Why would the mass buy EVs even if they are at the same cost? There are so many unknowns to the buyer… pickup, buying cost, recharging cost, repairing cost, looks etc.

I think, unless the management sees EVs getting a lower cost-per-KM, they wont’ go heavy.

As of now, I will let this EV-disruption and poor sales factor drag the share price down, and buy this long term compounder at corrections.

8 Likes

People underestimate the staying power of a company like Hero. Yes disruption shakes the pecking order but not if the mgmt is PROACTIVE.

Proactiveness shows up in the way Hero mgmt has invested in Ather to get hold of 2W EV technology. The way it has invested in ramping up scooter launches, the way it is launching premium bikes.

If you can’t compete with a competitor, copy it or buy it. That’s the age old rule of business - Facebook has done it successfully, Walmart is trying to do it as well.

Hero is doing both - buy Ather, copy premium bikes from competitors.

At the same time it is spending ₹1500 crore on capacity expansion that’ll further cement it’s lead in the mass market bike segment in the south (majority of ramp up in Andhra I read).

Add to all this is the attractive price the company is available at currently & it really is a whole package.

Disclosure: invested & views biased

7 Likes

Anyone has access to Smartkarma? There is a piece on Hero by Nitin Mangal with the following summary:

Expectations of setting gold standards are always from heroes. Hero Motocorp being the largest two-wheeler company of India and part of Nifty-50 is expected to raise the bar, be it disclosures or corporate governance standards. These great expectations are put in check as just a glance of its financial statements revealed that rather than following conservative accounting policy and disclosures, the company has adopted aggressive policies which tend to mask its comparative and real exposure to financial risks.

It will be Interesting to see how the 2 and 3 wheeler market will get disrupted over the next 5 years.

1 Like