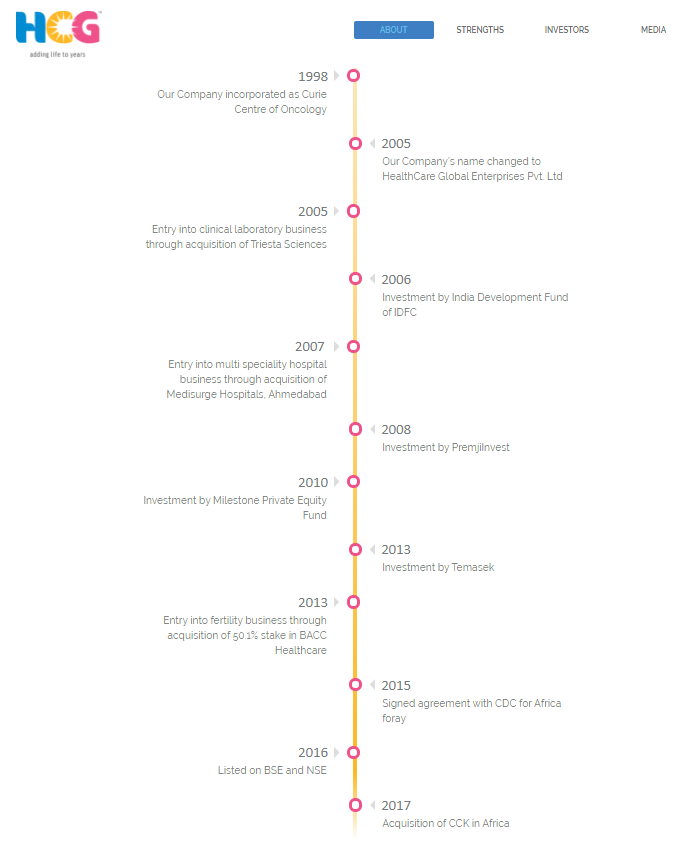

Healthcare Global Enterprises (HCG), a leading cancer care hospital chain was started by Dr BS Ajaikumar in 2005. The company initially established 10 cancer centres with private funding. Currently, it operates 24 HCG facilities (18 cancer centres, two multi-speciality hospitals, three diagnostics and one-day care chemotherapy centre). HCG owns 1364 beds and a team of 200+ oncologists (FY17). Currently, Karnataka, Gujarat regions comprise ~75% of overall revenues. In 2013, the company entered the fertility segment by acquiring a 50.1% stake in BACC Healthcare, founded by Dr Kamini Rao, which operates seven fertility centres under the Milann brand in Bangalore. Cancer care, fertility segment accounted for 92%, 8% of FY17 revenues, respectively.

Unique Business Model :- What I mostly like about this story is their unique scalable business model.

Hub & Spoke Model :- wherein it leverage the Bengaluru COE [Centre Of Excellence] hub for providing seamless cancer care across the comprehensive cancer care centre spoke.

Local tie up to set up new centre :- Focus on a single speciality and opening of newer centres on a partnership model with reputed doctors, typically leads to a breakeven of ~12-18 months for each HCG centre.

Asset Light Model :- Cancer treatment requires multiple patient visits to centres. Its treatment tenure is generally longer than other major therapies. Over the years, the company has followed a strategy of tapping local oncologists to set up a cancer centre. Each cancer centre offers comprehensive cancer diagnosis and treatment services including radiation, medical oncology & surgical treatment. It follows a partnership model (with HCG holding majority stake). This also helps it achieve faster ramp up in newer centres. As per management, a new HCG centre requires | 45-60 crore of capex of which 45-60% account for equipment costs, which is leased by the vendor and is paid by the centre after three years of equipment purchase. Hence, upfront outgo is only | 15-20 crore to put up a HCG centre. Each centre typically has eight to nine doctors and two to three physicians. HCG plans to increase its cancer centres to 25 (from 18 in FY17).

HCG also owns and operates two cyclotrons, which are used to produce nuclear medicine to cater to its own 13+ CT-PET scanners (FY17) as well as supplying the same to third party scanners. Going ahead, the management is keen on setting up new HCG and Milann centres in high growth markets and also, expand into Africa through its existing collaboration with CDC, UK. The management has guided for a capex of| 200 crore in FY18. Gross debt was at | 442 crore in FY17 of which vendor debt is | 196 crore.

With it’s focused single facility operation in high potential niche area than go for multi-speciality has caught my eye. HCG expect to post 23% revenue CAGR over FY17-20. Owing to strong therapy tailwind and EBITDA margin levers HCG is positioned for robust growth over next 3-4 year.

Strong EBITDA growth over 25% is CAGR is very achievable aided by steady growth in Centre Of Excellence (Bengaluru), scale up in existing centres which got operational till FY16, and reducing loses from new centres which got operation in last two year.

Key Risk :-

Success of Business hinges on network expansion :- HCG’s business growth has been primarily driven by new centres and hospital setup through various partnership arrangements and acquisitions. It is expected that this will continue to be key driver for future growth.

Subsidiaries financial performance :- Sum subsidiaries reported net loss this year. Going forward they may continue to drag and may not sustain profitability , which could materially and adversely impact business prospect.

Specialist physician could disassociate :- Success of this business will depend on HCG’s ability to attract and retain the leading specialist doctors.

Expansion Plan :-

HCG is following a cluster based growth model.

Karnataka Cluster :- This is the most important cluster which account for 47% of revenue is having the COE and 55% of total capital has been employed here. Expansion plan will be muted here rather HCG will focus on operating leverage from this Cluster.

Western Cluster :- The next leg of expansion will be in this zone. 51% incremental capital will be employed between FY17-21. This cluster as of now accounts for 33% of total revenue. New CCC will come up in Borivali , South Mumbai, Nagpur and Baroda.

Expand wings in Under Served area of Africa :- HCG believes it’s speciality healthcare model can be replicated in other under-served healthcare markets as well. It intends to establish a network of speciality cancer care in East Africa. It has enter into a definitive agreement with CDC and it will invest in the former subsidiary HCG Africa to setup a network of CCCs.

Growth Prospect :-

Fertility and emerging high growth area :- Fertility treatment is yet another emerging segment in India’s Healthcare Industry. The number of couples going for infertility treatment and evolution is likely to increase from 270K in 2015 to 650-700K annually in 2020. The number of IVF cycles performed in India is likely to increase from 100K in 2015 to 250K in 2020.

Domestic Oncology Outlook :- The prevalence cancer in India is expected to increase from 3.9 mn in 2015 to an estimated 7.1mn people in 2020. Reported cancer incidents in India is expected to jump from 1.1mn in 2015 to 2.1mn in 2020.

Underserved Under consumed healthcare in India :- Total Healthcare expenditure in India was at $85bn in 2015 and registered a 13% CAGR from 2000-15, out of which 70-75% is in Hospital segment. While private expenditure jumped 12% the expense from Govt/Insurance jumped 14%. Going forward , assuming GDP growth rate of 8% over FY17-22, it is expected that growth momentum in healthcare expenditure to clock 13-15% cagr over same period and would reach $180bn.

[Disclosure :- Invested 30% of my portfolio . Hence views might be biased ]

Yes it does but it has always been the story from IPO moreover in the recent downturn the valuation remain stretched . Considering the value unlocking from their existing setup I think the valuation is quite justified.

Point I like is opportunity size - which is huge.I read the Annual Report and as per the data shared there there is no doubt of opportunity size especially with the -

Rise in oncology cases

Healthcare insurance playing out

Lack of special cancer care chains

Aging population coming up in India.

Awareness towards cancer

There are many detailed point shared in AR and one must see.

It looks like a long term story if executed well as you added in your notes.

I am skeptical about the local tie-ups.Generally if we see people around us - people try to go best and specialty hospital specially for oncology.A general healthcare hospital like they have in amdabad might be fine but for oncology local tie-ups might be looked down.I would be keen to watch the performance of other centers going ahead.

Also, valuations in general are stretched but how to value a hospital is different.If someone can shed light on valuing hospital chain then we can further delve down.I read a report somewhere on how to value a hospital chain - like AROPS, number of beds etc.

I invested little amount for tracking and would be interested in more information.

As per the company the local tieup they are only having with most reputed oncologist. So It is understandable that it will be a both way beneficial and this space is now overcrowded with patients so I don’t think there is any risk with local tie up.

About the Ahmadabad mulispecialty hospital they are planning to convert it to a CCC.

Valuation is definitely stretched but one need to understand the niche space this company is operating on and large longterm scope for value unlocking . Hence in my opinion this valuation is quite justified. Though need some opposite views to understand if I am missing out anything in this part.

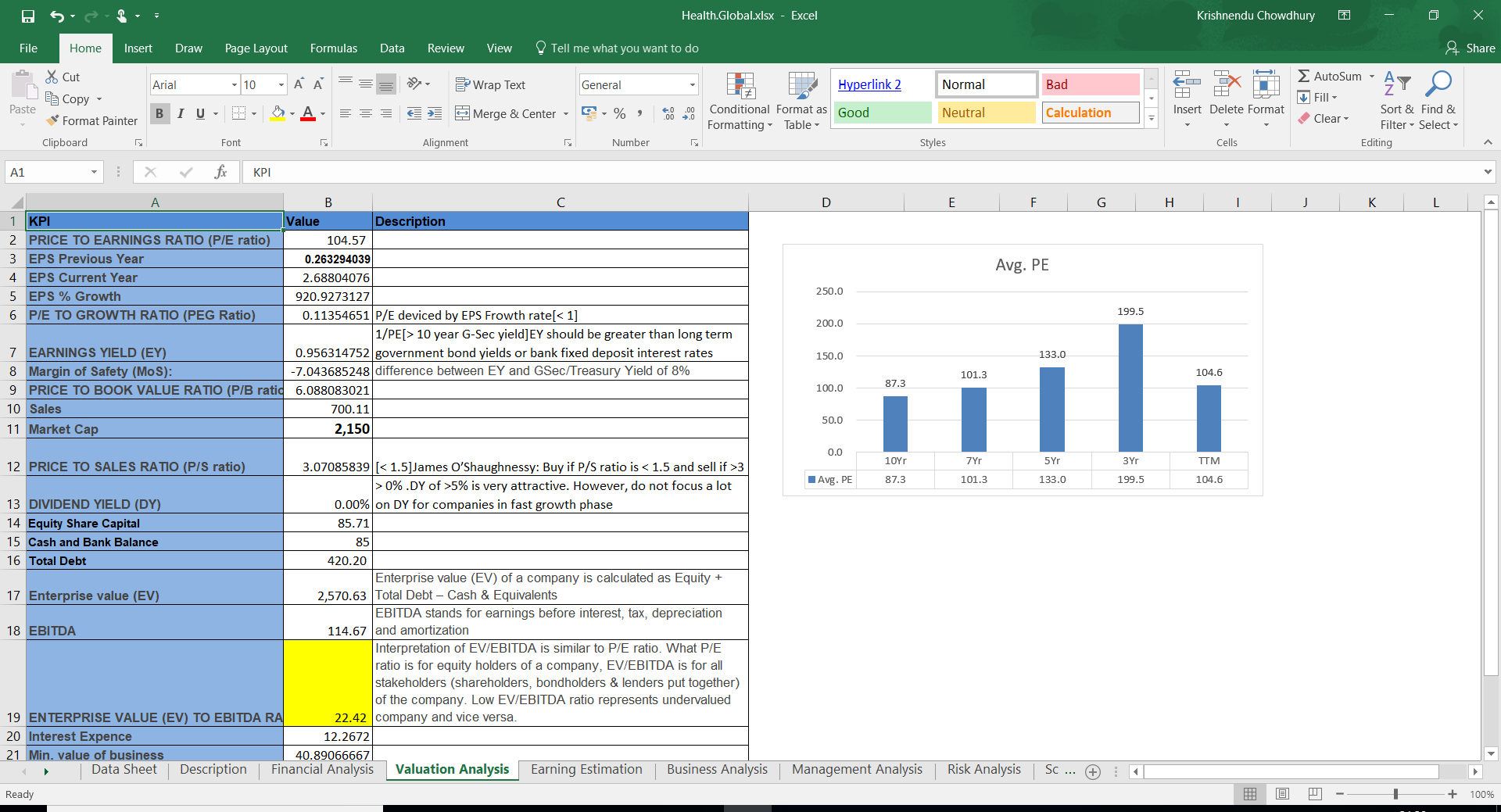

Well I believe everyone is considering the PE here for valuation but in my opinion it should be based on Enterprise Value and what I have got here is 22.4 . So very much reasonable for me. And also you can find a historical PE downtrend with the EBITDA margin improvement and as soon as the CCC become profitable we can see more downturn in PE. Also the Price to sales ratio is at 3 so if I go by most conservative estimate of sales growth of 15% then also this valuation seems very much justified to me.

I think this is a unique business and hard to calculate the valuation

Mohnish Pabrai had placed a significant bet on this . I like his investment thesis . I guess he sees something in this business which is not clearly visible , at least to me .

In my opinion the valuation should be considered on EV TO EBITDA [which is similar to PE ] basis along with Price to Sales ratio. Both of which I have explained earlier.

I think here the story is more on the jockey and high growth - under served Cancer and Fertility treatment businesses, off-course asset light business model, partnership with local doctors.

Key Risk: They have grown mostly by InOrganic way of Acquisition mode, any one wrong step in future will spoil the story.

I haven’t given much information about them because they are very renounced personality also many information is available in public domain . The only concern is about the valuation I guess here regarding the 130 P.E. But as I have mentioned it is trading at 22 EV/EBITDA and 3 times of it’s Sales and with continuous decreasing P.E. as the CCCs gradually becoming profitable. And once all the CCC will become profitable it will be a Cash Cow. considering this facts I have invested 30% of my Portfolio hence view might be biased.

See I always have mentioned that valuation is a concern but different investment philosophy is having different way to assert into it. I have been tracking this company since their IPO and all the time it’s valuation kept myself away from this stock . But when the Indexes were corrected a lot in recent times but Market is willing to give it a high PE. This boost my confidence and I only have invested recently. Also the Company board has approved almost 9.34 lac share to the Promoter at a price of 321.

I just tried to a comparison between Fortis and HCG. I understand both are into different specialties.But i just wanted to compare it a very high level basis.

HCG - BED- 1659

FORTIS BED- 10000

So Fortis has 6 times more bed capacity than HCG if we ignore all other factors market cap of Fortis should be 2700 crore (HCG MCap) * 6 which is close to 16000 crores.

Now let us look at other factors - Average revenue per bed (ARBOP) of HCG is rs 30598 and that of Fortis is 36000. The occupancy rate percentage of HCG is 50% and that of Fortis is 72. So even if you consider HCG is into very specialized offering it might take a year to catch up with Fortis metrics. So Fortis fares better on these metrics.

Now lets come to debt HCG has debt and other liability of 800 crores. Fortis has about 4800. So fortis has excess debt of 4000 crores. If i remove the debt from 16000 crore market cap the value of fortis it 12000 crores.

The bids for Fortis has come around 160 rupees which gives it a market cap of 8200.

So either Fortis is highly undervalued or HCG is overvalued. Let me know if i am missing anything.

Hi

Here, I feel we have to give weightage to perceptions on management also which is a huge factor on future performance and valuation.

Kind Regards

Jose