anyone who hadn’t considered SEBI lowering the TER already does not understand the nature of the business. Only unknown was the timing. However, timing of lower TER adjustment should not impact fair value in a huge way. I was surprised to see many analysts reduce their price targets after SEBI announcements. I guess they have to go with the flow rather than stick their neck out.

My fair value calculation is based on a low discount rate of 11% which the market will assign to a strong business like HDFC AMC. When a business is trading at fair value, expected return is equal to discount rate used in valuation. If you are willing to invest with an expected return of 11% (and many people will be more than happy given the alternative), this is a fairly valued investment and a good balance between (low) risk and (low) return.

But when a business is trading at fair value, there is no margin of safety also, isn’t it?

P. S: It’s only an academic question. I don’t track this company or hold any stake

Hello Yogesh, only for the sake of argument - is 11% an adequate discount rate to make up for the risk that comes with a cyclical business (even as good as HDFC) like AMC’s? Can we confidently say that the HDFC’s future purely rests in their hands and that no external events are likely to shake up the profitability of the company? I wouldnt mind assigning a discount rate of 11% to HDFC bank or Procter and Gamble Hygiene and Health, or Castrol.

Worth watching…

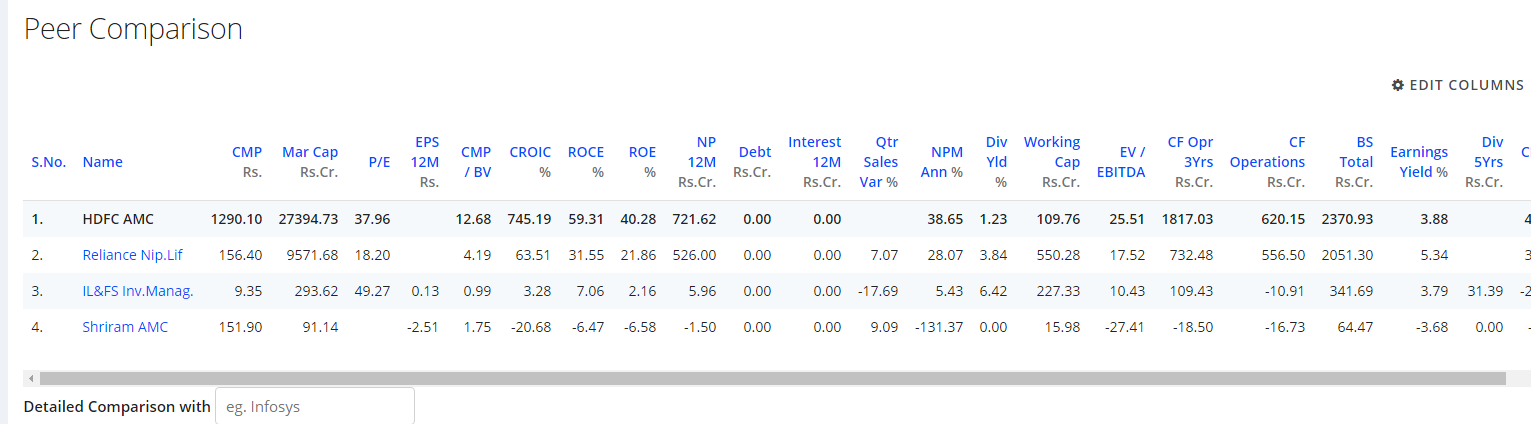

Guys, can you name more listed players in this space like MOSL, edelweiss, HDFC AMC

Looks like the quarterly AUM numbers for HDFC & ICICI MFs have reduced marginally in Q2 as compared to Q1, where as SBI & Kotak and couple more have shown QoQ growth in AUM. Any views?

https://www.amfiindia.com/research-information/aum-data/average-aum

I think it is very difficult to assume unless one gets out the data for category wise growth, which I believe is now published on AMFI website.

For e.g: If bulk of the flows into SBI and Kotak is into low yielding ETFs and Debt Funds, it doesn’t mean much.

Also, since market has fallen, one has to segregate flows from performance while comparing AUM. That also shouldn’t be difficult as point to point performance of all schemes is available on websites like value research

@Yogesh_s @dineshssairam @drgrudge @zygo23554 @prashantrane2000 @hitesh2710 @deevee

Has anybody looked at how the Fund Manager/CXO’s compensation structure is designed? Is it aligned with interests of equity shareholders?

Fund managers can eat away substantial portion of the profits by way of performance based incentives/Bonuses impacting return to equity shareholders.

Ideal to have a low fixed salary + performance based compensation linked to share price.

Hi

HDFC AMC posted its results.for Q2FY19

- 13% growth in revenue from Q2FY18 to Q2FY19

- 9% growth in AUM YoY. AUM dropped from June 18 to Sept 18 (2.8%)

- SIP flows have remained more or less constant since June

- Individual accounts continue to grow +24% YoY and also an increase from Q1FY19

- 64.2% of txns happening digitally vs 48.4% in Q2FY18

Rgds

Hope this well rest the euphoria this thread has generated. Overvaluation will get correct for sure

Is the result / Numbers after SEBI profit margin reduction? or the impact will be in next quarter ?

Given the reduction in AUM QoQ (which is primarily due to stock market correction I guess), do you think they have managed well enough to maintain profits at levels same as Q1?

From there presentation

"1. Reduction of 15bps in TER (effective May 30, 2018) -entirely passed on to distributors

2 SEBI circular dated October 22, 2018 –Key points

• No upfront commissions to be paid except on SIPs

• All schemes related expenses should be debited to the schemes’ account and not the AMC account

. B-30 expenses and commissions restricted to assets raised from individual customers only

3 SEBI yet to notify on the reduction of TER • Weighted average impact on HDFC MF equity-oriented AUM at c. 24bps (our endeavour would be to pass this on by reduction of distribution commission)

No major impact on profit of next quarter also as it will be cut from distributor share

Thanks

Ashit

Pretty impressive Q2 presentation in terms of the way they have addressed most questions proactively rather than just put out data and gyan without deeper analysis.

Interesting to see them state outright that TER impact will be passed on to the distributor and the company will not be absorbing this, as clear an indication of where the power balance lies. I will try to get a sense of how the distributor community is reacting to this and how they plan to tweak their product mix - from what I can tell based on personal experience, the stoppage of upfront commission coupled with AMC’s passing on TER cut can be pretty huge in the short run. Effectively one is asking the distributor to work hard this year to increase his revenue for the next year, large banks and distributors will surely try to push bulk of the incremental equity AUM towards PMS and AIF since they can make 4% upfront fee there.

One Q that I need to get answers to is in the classification of their AUM by channel - Equity AUM it says Direct share is 17.4% but does this include the money that comes in through the RIA code? Will talk to some people over the next month or so and finally get down to doing some work on this story.

Does anybody have the q2 cincall transcript or notes. Please share. Not on website. Thanks

Chart shown in article says about trust and brand power

Thanks

Ashit