DCF analysis should be done using Cash Flows and not EPS. Also ensure you account for variables like maintenance capex, incremental working capital and cash taxes correctly.

1 Like

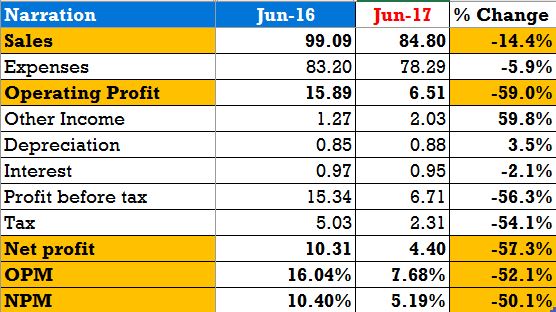

Latest results for Q1-FY17.

1 Like

Poor set of results.

One of the reasons could be inventory destocking due to GST which is the explanation given by a lot of FMCG cos for poor results.

6 Likes

Is any one on the forum attended the AGM?

I attended Hawkins AGM & reason for such steep fall was attributed to GST indeed…

Every other quater they face one issue or another, Chairman is too old to understand the business dynamics of present day business. NO hope left for making any decent money in Hawkins…Maybe Div yield can hold price to certain level, but post BM Episode not much price action seen in Hawkins…

Disclosure: Not holding Hawkins, but tracking since many years now.

3 Likes

Thanks Ashish…What about the young Turks from promoter family…son and son in law? Did they show any signs of taking the business to next orbit? Mored details, if you could share, on AGM would be a really great help…Thanks to Hitesh Bhai who put across the insight i.e GST angle while everyone else had the same data…Regards.

His Son Neil Vasudev (Aged in mid 40s) is not even part of Hawkins board and son-in-law is CFO of the company (came to board few year ago).

Chairman is talking launching news products since many year’s now and what they launch is new variant of pressure Cooker or cookware (Like induction compatible Cooker etc) which not seen to take their growth to even double digit consistently… I feel Div of yield ( Rs 70 0 Div this year) will hold the price above 2500, but consistent double digit growth seems to be distant dream for Hawkins…

In Cooker itself they are not able to capture market with monopoly & new cooker companies like Vinod, Bufferfly along with TTK able to sell because of supply side issues with Hawkins… Most of time in the year if I go to market to check the Hawkins cooker, dealers says thay they dont have supply from Hawkins, but you can see others likes Prestige, Vinod & others brand stocked sufficiently.

7 Likes

Destocking is usually followed by restocking. So maybe some part of pent up demand will spill over to the next quarter.

Thats atleast the way some brokerages have upgraded Emami.

In terms of stock market reaction, usually a couple of days is the time it takes to manifest itself in range bound markets and after that the stock price tends to establish a range till the next bit of newsflow occurs.

6 Likes

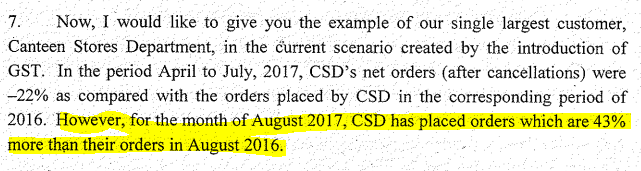

Q1 was impacted by GST-However heartening to note that sales have picked up in August 2017.For eg business from their biggest customer CSD fell 22% in Q1 but has gone up 43% in Aug on yoy basis.Long term GST will help organised players like hawkins.Since market prices in the future my submission is that Q2 is going to be better than Q1 (and Q2 of LY).Other than the chairperson the key person to watch is his son in law ex citi banker and current cfo

As on date they have 1097 active dealers.Once they capture dealer mind and shelf space the dice will roll.Till then the anxious will exit.

Dividend yield is zero protection .Growth or the first whiff of it is the only protection.We must watch the sales numbers for Q2.

3 Likes

Nope. August is correct. Advance orders mentioned in Brahm’s speech.

http://www.hawkinscookers.com/download/AGM-Speech-2017.pdf

1 Like

All,

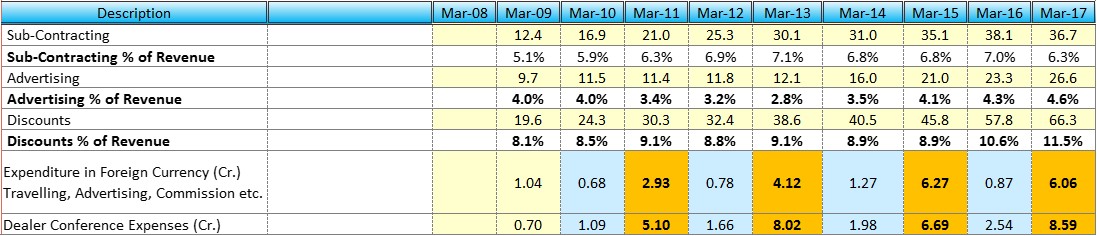

Any idea why the expenses-Expenditure in Foreign Currency and Dealer Conference Expenses- jump drastically on every alternate year (jumped in FY11, 13, 15, 17)?

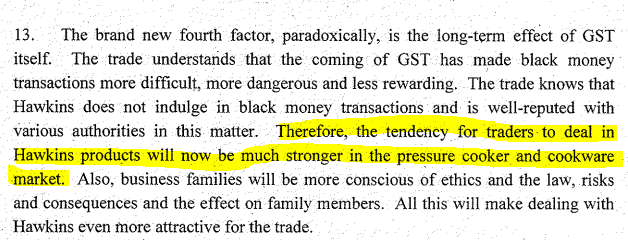

Quite bullish commentory from management in AGM (read in exchange announcement)

http://www.bseindia.com/xml-data/corpfiling/AttachHis/11a02c3c-011e-49e1-b821-9ab0cf81a946.pdf

Let us see how the story pans out, so far it has been a laggard.

Disc: Not invested, tracking the story

5 Likes

Q2 PAT up 55% Sales up 14%

The results are in line with what management mentioned in the AGM as per snapshot shared earlier.

A new product was launched in September.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/9c36cc2c-ee02-4d64-b21a-96208252dbb9.pdf

1 Like

There was a huge inventory build up, broaders could come in

Compared to last year festival season was earlier.

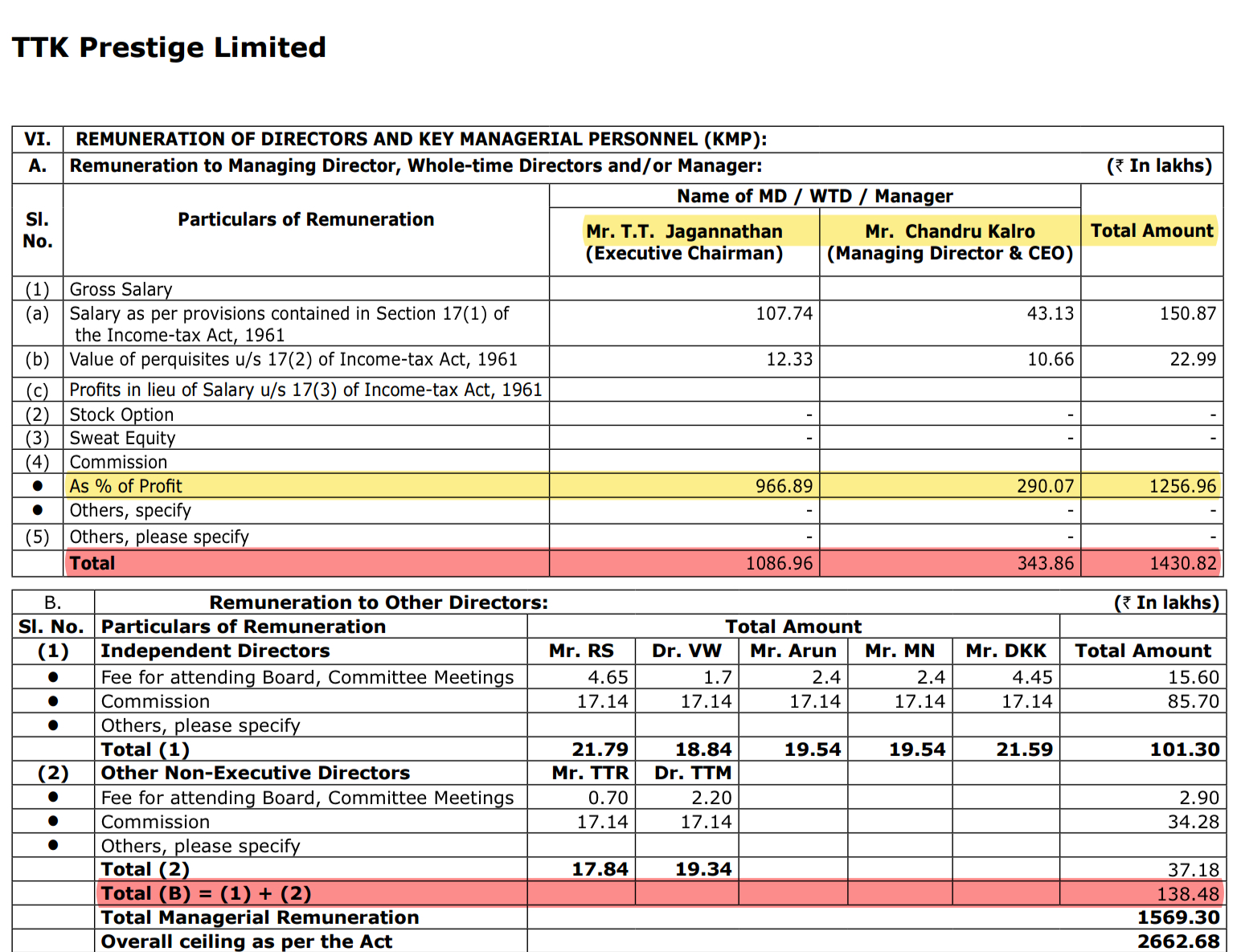

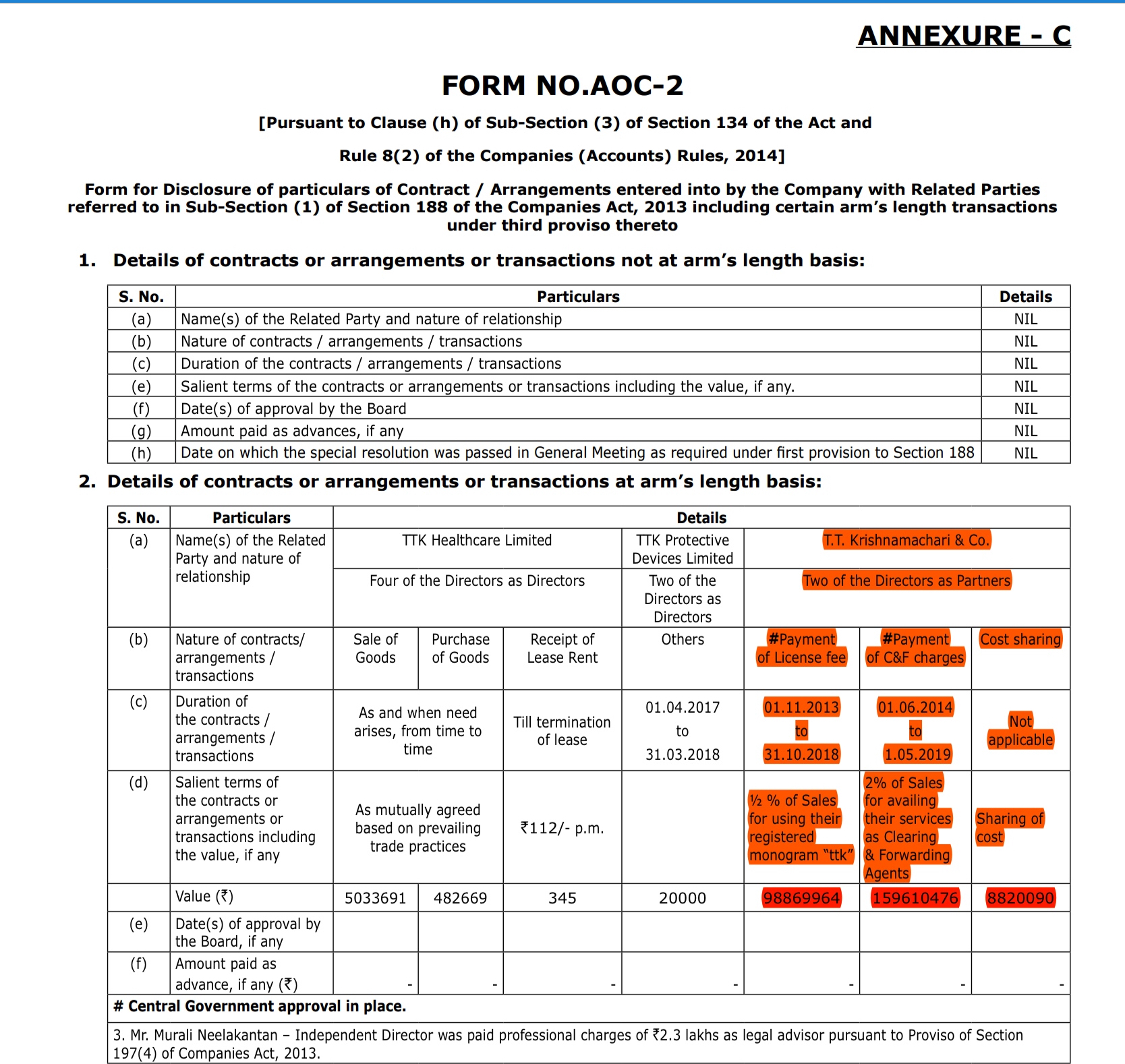

Vivek Sir , according to recent AR of TTK Prestige, 2 directors and one director cum secretory are drawing more than 17 Cr as salary plus commission and on related party transactions, they are drawing more than 26 Cr as trademark royalty and some else thing which I m not understanding. Is it ethical way? Am I missing something? Though I am replying to a very old talk but kindly clear my doubt. Thanks.

3 Likes

Dont track the stock dear

1 Like

Sir, I am just asking in the reference to the quoted post.