There r two things that I am waiting for to re-enter:

- A bit time correction as earnings catching up

- Management to be more aggressive and dynamic to market situation.

There r two things that I am waiting for to re-enter:

Finally a good set of numbers. both top line and profit.

topline: 140 vs 110 yoy

eps : 12.81 vs 5.81 yoy

i am not sure if the base itself was low.

discl: no holding.

If you remove the impact of VAT settlement EPS would have been close to 18 so almost 200% rise on small base. Looks like they would end the year at 70+ nothing transformational as such. DPS might rise to 60 again and it will settle at 3k+ for the year. The only issue is that have they left sluggishness behind or just another false start?!

Disc: Sold last year after substantial opportunity cost and lessons learnt

Karvy comes out with a well researched report on Hawkins (is this the first ever analyst report on Hawkins ? ) download report from below link

good numbers , is it finally turnaround?

Unless they start growing sales, this will remain a flash in the pan. The profit surge has come from raw material side which can reverse easily with rising metal prices.

Chairman’s speech http://www.hawkinscookers.com/download/AGM-Speech-2016.pdf

Interestingly he compares the numbers with HUL. A comparison with ttk would have been more appropriate. ( its better than ttk also)

They have good quality products.

But Too slow, too cautious for today’s dynamic world. Just to come up with colored cookers, they took years.

There is a strong demand for quality kitchenware beyond cookware which Hawkins has not been able to exploit.

They want to imply that cookware market is as saturated as FMCG? The question is which is the equivalent of Patanjali in cookware segment? I remember till sometime ago they were implying that they don’t suffer from demand challenges. However, one thing is clear that the return ratios are similar with little growth prospects like HUL.

I had a shocking experience with their online sales channel recently. I ordered quite a few stuff from their website and one glass lid was a cracked one. Repeated mails and calls, sending pics of the same did not help. I gave up chasing them for replacement. Perhaps they had not designed reverse/return logistics.

Hawkins, in my opinion, has always suffered from lack of ambition and drive. The space they operate in and the brand recall was never capitalized on fully. To me it is a story of many missed opportunities for the company. They could have dominated this space completely, instead of making excuses for poor growth and comparing themselves to HUL

I agree with you guys. But a 47 PE TTK with a very wide range of product portfolio hasn’t done anything great in the recent past.

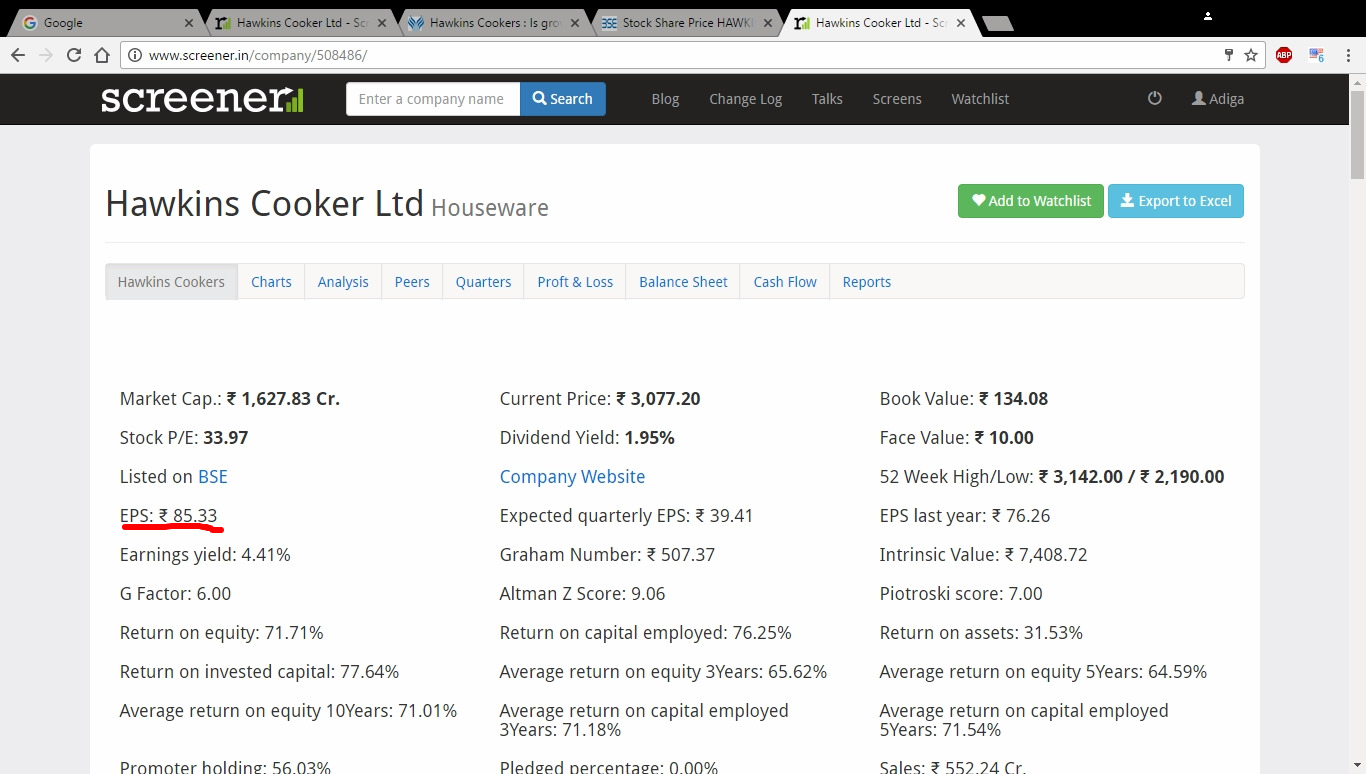

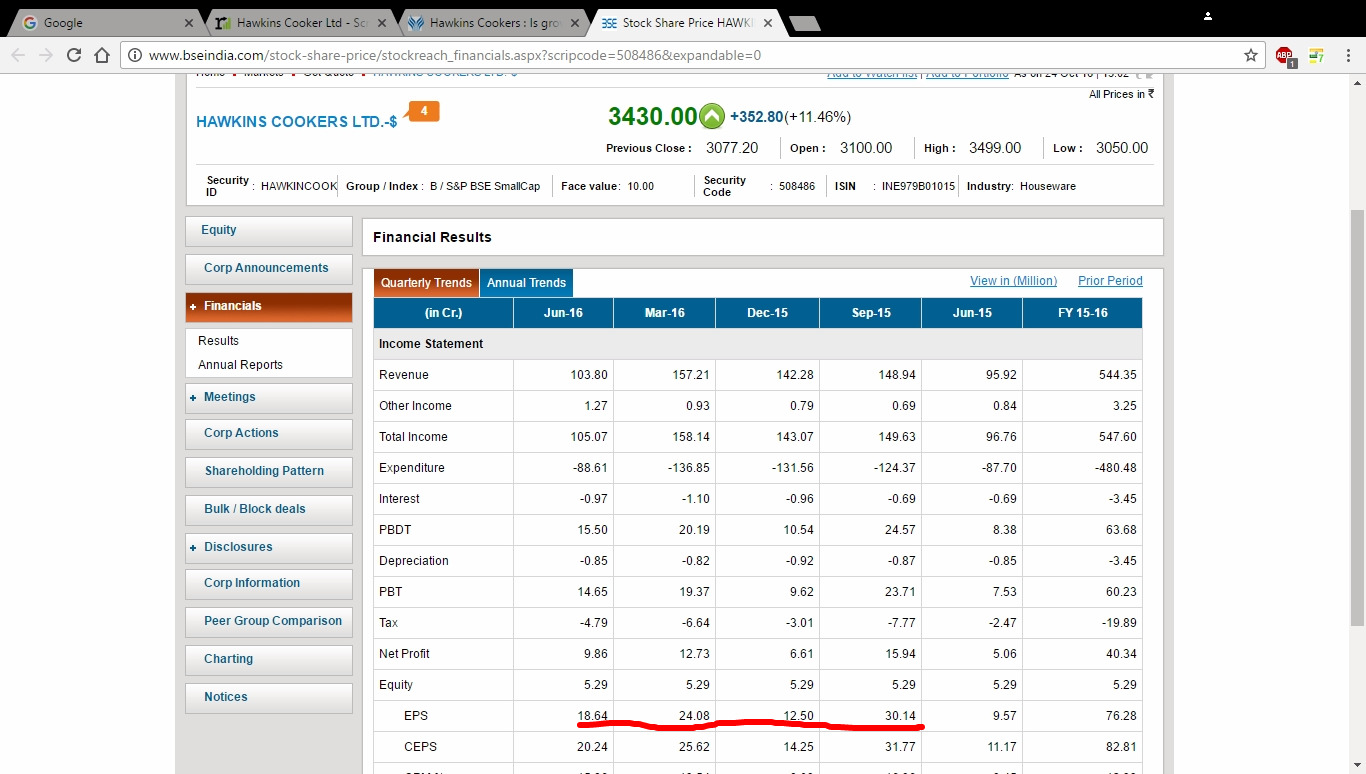

the figures on screener.in are correct

http://www.bseindia.com/stock-share-price/stockreach_financials.aspx?scripcode=508486&expandable=0

Yes you are right. In the annual results the eps figure is different. @pratyushmittal Please look into the matter.

EPS is correct. its the TTM EPS

Thanks All.

Pratyush: Hope you will find a way to correct this anomaly as the 10-yrs EPS figures in the annual results table appear incorrectly on the website but get corrected on downloading the excel

Thx

RR