Actually, I don’t think building the software to evaluate credit risk is not the moat but using it to actually assess and stick strictly to the parameters is the moat - execution is the moat. No matter how strong a system/process is if the branch managers, credit risk officers are slack and don’t implement it while sanctioning loans, it will backfire. Since Gruh had already had a bad experience in 2000s, once bitten twice shy.

The other companies, not sure if can execute as well as Gruh and here lies the moat, in my opinion!

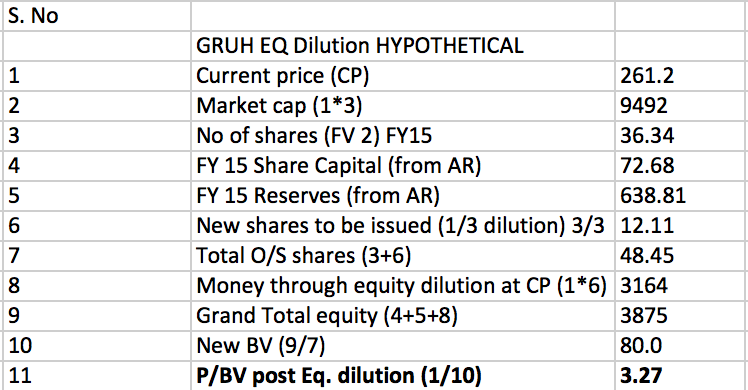

For all those worried about gruh price to book just consider a hypothetical situation where gruh dilutes equity at current rates to the tune of 30% and then calculate the book value then arrived at. It will in all probability look extremely cheap. But since it has very high ROE, it doesnt need to dilute equity.

Plus it pays out 30% of profits as dividends which restricts book value growth.

As mentioned before in the post, gruh has to be evaluated on a PE basis, rather than getting stuck with price to book.

with Hitesh’s nudge, I wanted to do this exercise and below are the results. I will leave it to the forum members on further conclusions. I kept it fairly simple.

the RoE will come down only in the short term as the funds lie un-utilised and as the business can generate high RoE, Gruh will lend more money with the increased equity base (remember, for finance companies leverage is allowed so GRUH can probably lend 10 times, not sure what’s the current leverage of Gruh) and over 3 years or so RoE will go back to previous levels and market knows this so the PE will NOT drop to proportionate levels.

the co is staring at a ticking time bomb - which is a high impact highly likely mudra bank type initiative by Modi to provide affordable low ticket housing finance to the self employed (big vote bank of BJP ) - How can profiteering from the helplessness of a segment like the non documented self employed be a sustainable moat if they are privy to more information as to who is charging how much + if they are a big vote bank + in age of aadhar+Mobile+low cost bank a/c ?

If the RoE drops once for all permanently, it probably means business fundamentals have deteriorated and then as you said, PE will drop (not disproportionate, even worse, exponential) , in fact, that stock will be butchered. Not so in this case of Gruh as RoE will move back to originals levels. Anyway, let’s move on!

can you calculate how capital employed (denominator) will look like on the second year from the time gruh (hypothetically ) issues a qip at cmp . I say hypothetical since if the co has not diluted equity in last 10 years i do not assume it happening now they do not need it too .

Even assuming same efficiency levels ROE can not come back to original levels in 3 years since it has to fight a higher denominator .will be happy to be proved wrong with data .

reacher, let’s move on friendly as this particular discussion is not very important in the broader sense My calculation is only hypothetical as indicated. Also, I said “3 years or so” and did not say “exactly 3 years” - I did not want to do number crunching, make assumptions and find out how many years it will take to reach original RoE etc as this will not lead anywhere nor this is something very important as dilution is NOT happening.

I’m happy to bow my head and move on dear friend. But if it were a significant business changing thing, we would have been happy to discuss this thread bare left and right as per usual VP norms

Income group Monthly expenditure on housing Est. no. of household Housing shortage Share of shortage

( Rs ) ( million ) ( million ) ( % )

Economically weak 0 - 3300 17.5 17.20 98.2

Lower income group 3301 -7300 27.5 1.50 5.4

Middle income group 7301 - 14500 9.9 0.04 0.2

Higher income group 14500 7 - - Source : Report of technical group ( 12th 5 year plan ) on housing shortage

Above table shows the shortage of affortable housing and represents the enormous opportunity present and everybody has space to grow.

But instead of growth by new companies what would be important that which HFC’s is able to maintain its asset quality.

Obtaining market share at the cost of assest quality is not advisable.

As well said by warren Buffet ’ When the tide turn off then you come to know who is sailing naked ’

For Gruh finance the LTV ( loan to value ) is 65% - 75% max. which shows the conservative mindset of the management and margin of safety in case of default, while incase of the HFC LTV is generally 85%.

For last 5 years for Gruh FY10-FY14 gross NPA’s has come down from 1.11% to 0.27%.

While for Repco for June FY14 the gross NPA was 2.5%.

It seems that the market is valuing Gruh more like A FMCG than a HFC because of its high ROE and div. Payout ratio. But htere are 2 points to be noted here 1. In past Gruh has grown faster than FMCG cos.

in future also it is likely to grow faster than them despite all the concerns in view of the huge potential.

2. FMCG cos. don’t have to deal with NPA problem but GRUH has to. But here also the past record

comes into the picture and in future also the position is unlikely to change given the quality of Management

and its parent HDFC. No doubt, market is giving GRUH high P/E and P/BV.

Here you will have to consider the flagpole from 183 to the top made above 300 levels. And then if u see the retracement by the stock was much more than 61.8%.

Flag pattern is defined as a temporary halt in side a fast upmove. Flag usually occurs midway in a stock’s upmove. Retracement of the upmove in a flag ideally should be 50% or less and preferably around 38.2%. Here it is not so.

But overall the structure that is being witnessed is quite good bcos it has made a strong base around 220 odd levels and then gradually moved up after digesting negative views.

Technical view on GRUH FINANCE LTD.The stock has tested a high of 317.70 in January 2015 and corrected to the levels of 189.50 in May 2015. Since May 2015 to till date the stock has formed a good base between the price range of 220 and 260. The recent up move in the stock indicates that the stock is coming out of the consolidation phase and is likely to move on the higher side. From last few trading sessions the stock has crossed and sustained above its 200 DMA which is currently placed around the levels of 253.Recently the stock has attempted to cross its previous 6 months high price with strong volume participation, which indicates that the stock price is attempting to shift in the higher range.Increasing volume in the stock in last few weeks coupled with consistent week on week price gains from last three weeks, suggests strength in the stock. The stock has formed a double bottom pattern around levels of 222 on daily and weekly chart and it is attempting give breakout of the same pattern.All of the above mentioned technical specifications indicate that the stock has the potential to test the levels of 315 in the medium term.

Buy GRUH FINANCE LTD. at Rs.260.65 and on dips up to Rs.250 with stop loss placed at Rs.240 (closing basis) for the medium term price target of Rs.315.

The irony is now between Fundamentalists vs. Technicals. Fundamentals says it’s a bit expensive while technicals says it is looking for a higher range break out towards 320. If technicals play out as predicted the stock will be even more expensive!

Does gut feeling has a place here? If yes, Gruh is headed higher.

Suppose they reduce dividend payout. What will happen? The growth rate won’t increase because they are not restricting growth for capital wants. What will really happen is leverage will come down. We need to remember Gruh is the most leveraged NBFC in India. RoA will increase a bit with reduced interest outgo. But with leverage down, their RoE will come down a lot. Their RoA is quite similar to many NBFCs, so will be RoE after reduced leverage. So valuation premium would contract.

My calculation is only hypothetical as indicated. Also, I said “3 years or so” and did not say “exactly 3 years” - I did not want to do number crunching, make assumptions and find out how many years it will take to reach original RoE etc as this will not lead anywhere nor this is something very important as dilution is NOT happening.

My calculation is only hypothetical as indicated. Also, I said “3 years or so” and did not say “exactly 3 years” - I did not want to do number crunching, make assumptions and find out how many years it will take to reach original RoE etc as this will not lead anywhere nor this is something very important as dilution is NOT happening.