I have worked in 2 organizations where there were mergers and they didn’t turn out well. Integration takes a long time and the story doesnt always work out. During all this time of confusion, competitors are working in BAU mode.

I sold off all my holding on this news. Not happy, but this is how life is.

Will consider to buy the merged entity later when the story and reality are clear.

A lot depends upon your horizon. Is your investment horizon the next 6 months/one year or a multiyear hold?

Without doubt, it was fantastic to be holding Gruh as a stand alone company. Very well managed business, top parentage, clear horizon with many-many years of growth ahead, competitor intensity likely to reduce, past track record etc etc. It was difficult to find fault with the business. But since you are in the stock market, you have to be ready for surprises.

I know I may be accused of being fatalistic but being forced to become a shareholder of Bandhan Bank may not be such a bad outcome. Bandhan promoters are also considered clean with good corporate governance (Mr Ghosh is a humble man, is what I have read), amazing casa (41% of deposits), growing faster than Gruh (during the last Q, loans grew 46%, deposits grew 37% while operating profit before provisions grew 56%- ILFS type provisioning of Rs 385 cr will hopefully not be repeated; reasonable net npa at 0.7%). What gives confidence about the quality of promoters & their conservativeness is that they willingly took FULL provisioning of Rs 385 cr in the last quarter.

In my view, it will take a few quarters for things to settle down. The March 2019 quarter should again result in very strong pat growth for Bandhan (ILFS provisioning will be behind and last Q is generally a strong one). A few more quarters of solid growth will make investors forget the shock of the merger. Many disappointed Gruh investors would have sold off and the selling pressure would reduce. Frankly, Gruh should start growing faster under Bandhan will a new geography to do business in and lower cost of funds due to Bandhan’s casa deposits. The combined microfinance business of Bandhan and housing finance business of Gruh should hopefully turn out to be great combination.

Markets hate uncertainty. The way I look at it is that at times like these, one has to do a ‘Rip Van Winkle’, in the story where Rip Van slept off and woke up after many many years.

Furthermore, Bandhan and Gruh is likely to be a good “bandhan” for shareholders. However, investors cannot afford to invest and forget this one till the current situation of reducing liquidity reverses, as growth will be slow in credit related businesses.

Market punishes those stocks the most, who’s PE is being derated and EPS is reducing. Gruh finds itself in that spot. Which brings me back to my question, will Gruh trade near the PE of its rivals: Can Fin homes, PNB HF, LiC HF? Is there is a compelling reason for investors to pay anymore than a nominal premium?

Hi @jamit05 ,

You are pointing a very valid risk, which is a short term risk I feel as well. Gruh valuation multiple may contract, as the HDFC parentage is gone, and that in turn creates an arbitrage opportunity/gap between bandhan and gruh share price - which in turn may lead to correction in Bandhan. I know I am speculating here so I want to declare that its just feeling like a risk factor for the price in the short term.

Not invested in Bandhan / Gruh .

It is important not to lose sight of the fact that 1000 shares of Gruh will give you 568 shares of (Bandhan + Gruh) business. Gruh as a standalone entity will not exist after the next few months so debating whether Gruh will retain its high P/B multiple is irrelevant. You will have to take a view whether you are interested in holding the (Bandhan +Gruh) combined business with its two main verticals of microfinance & housing finance with their financial parameters post-merger (my analysis below).

Interestingly, by buying Gruh at the current price, you will be getting Bandhan shares at a discount of around 8%. This discount is likely to narrow as the merger date approaches.

Attaching the con call where Bandhan has mentioned that they have taken a 100% provision of the ILFS Rs 385 cr loan. If the provision was not taken, net profit would have been up by 93% (Page 3).

My number crunching in the excel attached. PE of 29x as on March 31, 2019 and PE of 24x as on March 31, 2020. P/B of 4.7x as on March 31, 2109 and 3.9x as on March 31, 2020.

I am happy to hold on.

Assumptions:

Bandhan continues to pay Rs 1/share as dividend

Historically, last Q profit for Bandhan contributes 29% of full year PAT. Last Q for Gruh contributes 36% of full year PAT. Have taken more conservative levels for last Q PAT for both companies for calculating FY2019 PAT levels.

FY2020 PAT of combined company grows at 22% (in my view, it should grow faster than this). Gruh’s PAT grew 22% in FY2018. Bandhan’s PAT grew 21% in FY2018 (IPO was in March 2018 and Bandhan has been growing faster after IPO capital raising; 1st 9 mth 2019 PAT growth of 35% despite ILFS provisioning; Gruh’s 1st 9 mth 2019 PAT has grown slower at 16%).

I am also confused on this issue , I bought gruh 3 yrs back , there was a bonus last year and now this bandhan event , if i sell after 2 more years how will the LTCG be calculated on sale of bandhan

if you sell before the merger, you will get the benefit of grandfathering and LTCG will be calculated considering this, however, in case your shares get converted to Bandhan, grandfathering clause will not be available, rest calculation of LTCG will be normal

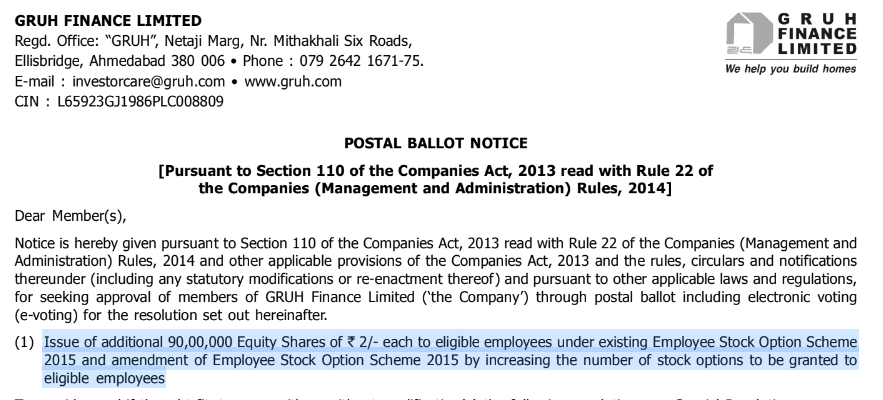

The outstanding number of shares of Gruh is around 73 crore. Thus the additional 0.9 crore esops will just add 1.23% to the existing number of shares which is not worth fretting about.

I believe that Bandhan-Gruh would like to retain Gruh’s existing top and middle management post merger and thus this decision to increase the number of esops to be granted. Overall, a wise decision.

If you go down the Postal Ballot Notice on page 7, it mentions:

"The maximum dilution that could take place in future, if all the aforesaid options are exercised, would not exceed 1.25% of the expanded issued and paid-up share capital of the Company, taking into consideration the un-exercised stock options as on date. "

Looking back, it was worth doing a ‘Rip Van Winkle’ on Gruh. Stock up 50% since. And up 60% if I take the price of Bandhan into account (based on merger ratio).

Probably the lesson is: Never underestimate the power of a great company to bounce back. The way of doing business is permanent, the stock price action is temporary.

A note from Bandhan Annual results on progress made on Amalgamation process

On January 7, 2019, the Board of Directors of the Bank approved a merger of Gruh Finance Limited with the Bank in an all stock transaction through a Composite Scheme of Arrangement. The Scheme has been approved by Reserve Bank of India (RBI), the Competition Commission or India (CCI), the Securities and Exchange Board of India (SEBl) / Stock Exchanges, and is only subject to approval from National Company Law Tribunal (NCLT) and respective shareholders and creditors of each entities. The appointed date for the transaction is proposed to be January 01, 2019 and the effective date shall be based on the receipt of the aforesaid approvals. Pending the same, the proposed transaction does not have any impact on the current financial results or the financial position of the Bank as at March 31. 2019.

Why wud Hdfc keep on holding 9.9% stake? Or the direct selling by Hdfc is over for now? Once Hdfc receives Bandhan Bank shares post merger they may sell Bandhan bank shares itself and the overhang of sale of Gruh shares is gone for now.

Remember that they were trying to hold on to their post conversion stake of about 15%, which was not allowed by RBI. So, they seem to be interested in Bandhan. HDFC may hold on to their stake for at least few years.

I am planning to buy Bandhan Bank share but I found GRUH is available at some discount to it. So my question is should I buy GRUH in place of Bandhan to gain this arbitrage or I am missing something here ?