This is a good point and I think we are already beginning to see this with Bajaj Finance. They have classified the mortgage business as a “scale builder” as opposed to a profit maximizer (unsecured loans). They expect RoE of only 15% in these kind of businesses that means for a HFC that is leveraged more than 10:1 you are looking at a spread of not more than 1-1.2% so soon others might have to follow to win new business and also to prevent customers from transferring their home loans…

Gruh Finance Ltd has informed BSE that at the meeting of the Board of Directors of the Company held on April 14, 2018, inter alia, the following businesses items/ matters have been transacted / approved :

-

The Board recommended Dividend of Rs. 3.30 per equity share of face value of Rs. 2 each for the financial year ended March 31, 2018. The dividend, if approved by the Members, will be dispatched / remitted within five working days commencing from the day after the ensuing Annual General Meeting.

-

The Board also recommended the issue of Bonus Shares in the ratio of 1:1 (i.e. 1 equity share of Rs. 2 each for each equity share held as on the record date to be fixed for the purpose) to the shareholders of the Company, subject to the approval of the shareholders of the Company. Such bonus shares, if approved by the members of the Company shall rank pari-passu with the existing equity shares, except for entitlement of dividend for the financial year ended March 31, 2018.

3 Likes

Gruh trading a meagre trailing P/E of 62 times and trailing P/B of 16 times  . This coupled with just around 22-23% of growth in PAT and BVPS in FY18.

. This coupled with just around 22-23% of growth in PAT and BVPS in FY18.

1 Like

Is it right time to buy GRUH Finance? I was thinking of buying NBFC and confused between GRUH or Diwan Housing Finance.

“Good companies become under valued over time” - Prof S Bakshi.You can buy it on dips and hold for long time and let the CAGR play.Good management,affordable segment ticket size only 9 lakh.18% EPS growth yoy assured. As PSU banks are dying NBFC are good choice.

2 Likes

Some more positives:

-

Zero net NPA’s (fully provide for all NPAs)

-

Over provides (even though RBI has reduced provision requirement for standard housing loans from 0.40% to 0.25%, Gruh continues to provide at 0.40%). This can be read from the notes of the March quarter 2018 results.

Gruh should give steady returns. It is not a cow boy stock like HEG. It will also test your patience and may not rise for a long time while your other stocks may be shooting up.

I feel each portfolio must have a little Gruh in them

7 Likes

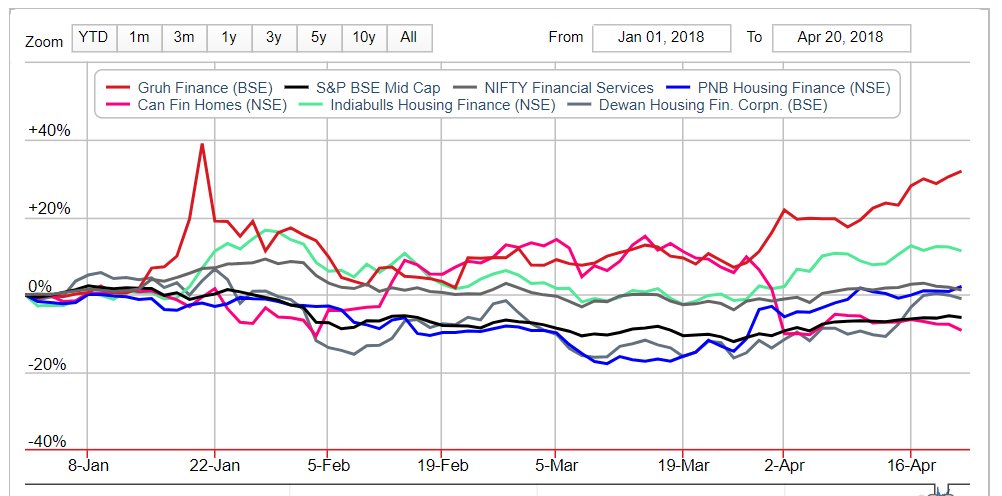

Having read the whole thread i can see a consistent message which states that Gruh is very expensive and despite that the stock has returned a YTD return of around 30%+ while the other HFCs have returned no where close to this figure. Twitter user @DIY__Investor has done this analysis to show that Gruh beats other HFCs by a mile

The question which begs to be answered is that Gruh gets super high valuation because of a simple reason. This is because the company has shown growth consistently for at least last 20 years now. This consistency and backed by the HDFC parenthood which means it has the positive association with the HDFC group. Its net profit has grown by the CAGR of 32% in the last 10 years and is now slowing down but that is expected as the base has grown to significantly in the last few years. Given this there is a huge expectation that it will keep delivering the growth of more than 20% in the coming years.

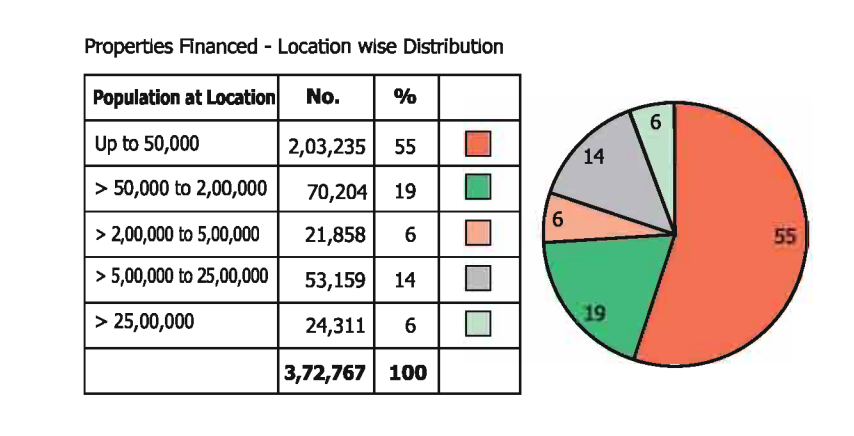

If there is any company which has understood the bottom of pyramid in India it is Gruh as they have a very good % of loan disbursement in the smaller towns. The below graph shows this very well

Disclosure : Invested from 400 odd levels.

2 Likes

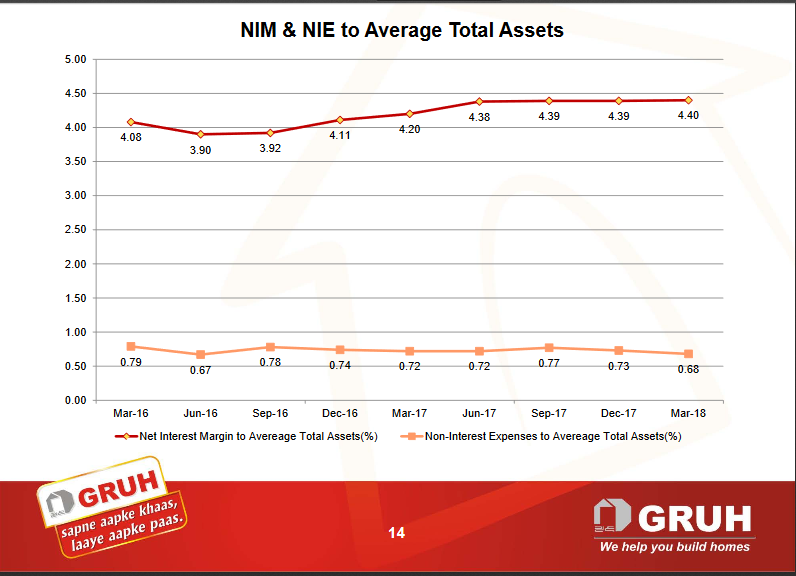

Beauty of Gruh…!! Just compare these with any other HFC…!!

3 Likes

Vivekvikramsingh:

Apart from increasing NIM’s and reducing cost to income ratio of Gruh mentioned by you, this is what is keeping the price of Gruh red hot…the expectation that growth will pick up further from 3rd quarter onwards with supply of affordable housing increasing…

Incidentally, Gruh remains probably the only lender in the world I know of, which does not need to raise equity capital to grow…profits reinvested in the business are good enough for growth…along with that, it pays out around out 30% of its profits as dividends…

4 Likes

Record date of 7th June for 1:1 Bonus issue

1 Like

Price of share will also halve and so the ratios will be constant.

At the outset, let me mention that my interpretation may be flawed. If so, please excuse me.

Bonus is issued from the profits the company has accrued over its existence. It increases the share capital. Liquidity improves.

And, it could be indicative of the management’s confidence to grow revenue and profits to compensate for dilution in earnings per share.

Bonus, inherently, is neither good nor bad.

Declaring Bonus shares is a sign that GRUH is increasing its profitability. Normally companies announce issues of bonus shares to their shareholders by capitalizing their free reserves . Shareholders have benefited tremendously, even after accounting the inevitable reduction in share prices post-bonus, since the floating stock of shares increases.

Bonus shares do not directly affect a company’s performance. Bonus issue has following major effects.

- Share capital gets increased according to the bonus issue ratio.

- Liquidity in the stock increases.

- Effective Earnings per share, Book Value and other per share values stand reduced.

- Markets take the action usually as a favorable act.

- Accumulated profits get reduced.

- A bonus issue is taken as a sign of the good health of the company.

3 Likes

In addition to what @mrai74 explained above, I think another crucial aspect to consider is “dividends”. When company takes decision to double its share capital, (in case of 1:1 Bonus), it is indicator of company’s confidence about its future profitability to service this larger capital base in future. So if dividend per share remains constant, company has to pay twice the amount of dividends paid pre bonus issue.

3 Likes

Yeah i agree as companies strive to maintain consistency in Dividends year on year if the business is doing well. This is one of real tangible benefits of the Bonus shares. But there is enough anecdotal evidence to see that the market views this a positive vote of confidence.

When the bonus quantity will reflect in the demat?. Share Price has been reduce but no of share still showing previous no.

Check with your demat account provider. Rules say that you need to deposit in 21 days. But a few folks have already got it. Am yet to get it . I use ICICIDirect.

Latest interview of Rakesh Jhunjhunwala on CNBC.

‘People are underestimating the impact of Affordable Housing on India in general and the subsidy the Govt is providing. In 2018-19, we are going to cumulatively build 3 times the houses we built in 2016-17 and 2017-18. Sector is ripe for good times ahead in the next two to three years’.

I tend to agree with him. The best for Affordable Housing is yet to come in the next few years.

(4th minute on the attached video)

6 Likes