One can conclude that Gruh is expensive to be bought right now. It tends to hover at PE <45 most of the time, and now PE is close to 60!

However, if it has been in the portfolio and is now in profit, then it makes less sense in booking profit as we see the EPS growing at a decent pace. Any further fall in price and PE will probably be an opportunity to buy more.

All in all its a good stock. Even if you bought it today, then one year forward PE comes to around 45, so it is a decent bet. In fact, a much better bet than most of the stocks.

EDIT: While we discuss which expensive stock to buy or not to buy, there are some really good stocks selling at rock bottom…

Good stocks at good prices:

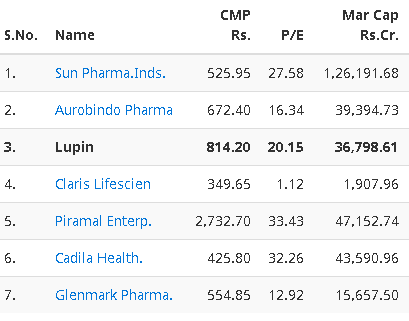

Glenmark selling at 13 PE

Lupin which consistently traded for several years at PE upwards of 35 … is now at PE 20…

Aurobindo at 16… another great prospect.

Judging based on past PE’s or PB’s doesn’t give you the right picture even if they were of very recent period. Reason being, we are looking at based on one dimension which is PE or PB. But the fact of the matter is the price is determined by multiple dimensions.

Over the last three years, the Govt housing subsidy scheme, the drop in the inflation particularly the supply side action by the government (which is long term in nature than the monetary policy based outcome), demon induced liquidity, economy becoming more white and the black economy slowly fading away, both FDI and FII inflows and improvement in govt finances are all playing a large part giving a lift to the financial sector and that is why the prices are appearing to be high, but they are not.

So logically the current price appear to be decent if you are not expecting the price to double every two years.

I am even considering loading up in a gradual manner @500.

Some people here in this thread are in the camp that Gruh is expensive.

Well lets ask when it was not.

Investing does not require only numbers. Its the individual style that counts.

There is no need to prove that gruh is expensive so no need to buy. Its individual money and individual style of investing.

Lets discuss something we don’t know, like what is gruh not doing which others are doing etc.

Or something which others are doing but Gruh is not.

Disclosure - Gruh is 60% of my portfolio and gives me peaceful sleep. I holding this from 2010 and ready to hold another two decade. My expectations from the stock are not much - Just a 15-18% compounder for another two decades.

I have a very small tracking position in Gruh and I took that when the price was half of current price about a year or so ago. I don’t regret my decision for two reasons -

Gruh is a great business - no doubt. But is Gruh a good stock bet particularly when the upside is limited. Can Gruh go up 5x from current levels in say 5 years?

Gruh has margin of safety from business strength perspective (Pedigree et al) but does Gruh have margin of safety from time correction perspective?

For me, the trick is that I want to get into a share when I see potential for valuation multiple change + Growth compounding resulting in a 100%+ appreciation with reasonable comfort on downside.

Most of us invest on gut, that should be clear by now. The very few who do professional Investing, have the latest info, attend AGMs, thoroughly analyse ARs of the company and its competitors. They even meet the management and visit factories and offices. It makes perfect sense for them to concentrate investments. They even buy the products and meet the supply chain people and get a feel for brand strength. That is how these Investors get conviction.

Most of us, on the other hand, invest on gut. We read on the internet, and ask opinion from other IDs… this shouldn’t count as research. We are making an informed bet at best.

Being comfortable with a bet is no measure of depth of research. Concentrating investment as much as 60% in one stock is clearly a big bet. Which like any bet, has probabilities.

Gruh was Trading at 35 PE only a year ago. A good time to make fresh investments.

Our decisions are dependent on what we are capable of and how much time bandwidth we have. Just because we have have various parameters in front of us doesn’t mean, we will become better decision makers. More than all the parameters, our emotions play a big part in what we end up doing. Several times deluge of information can lead to confusion, unless you know how you can structure that information in a meaningful way.

So it is smart decision making using the fair amount of information combined with experience and staying power not being swayed by various emotions which sprout in our mind.

Just one thing I would like to add here…

Many times what you hold is also the function of what all else you hold.

Hence, one thing which fits in one person’s portfolio construction may not be suitable in that of others.

Portfolio construction is an outcome of many complex inputs. And hence, some where that plays part in the selection and sizing of the bet.

One question for you and everyone else. When high growing reasonably valued (compared to Gruh) company like Canfin is down 30% from closing monthly highs and even the recent market darling PNBHF is down 20% from closing monthly highs, why is Gruh down less than 5% from its monthly closing all time highs? There is something the market knows and that’s why Gruh is valued so richly and still performing the best in a downturn. In a bull run, a Canfin or PNB or even DHFL may beat Gruh for a while but the peace of mind you have while holding Gruh is incomparable. As I said earlier on this thread as well - if Gruh corrects 20-30% percent then other HFs will probably end up down 50%. And as long as HFCs’ bull run continues, Gruh will not do too bad.

I agree with you. I sat on sidelines for many years arguing high valuations for many high quality high P/E stocks like Eicher, Page, Bajaj Finance etc and was hoping for them to come down to so called “reasonable” valuations so that I could buy them. But looking at what happened in last 2-3 years, clearly I was wrong.

So now I learnt a lesson. As @us121 mentioned in his post, as you would need few big hitters (high risk stocks) in your portfolio, there is need to have few “marathon runners(compounding machines)” in the team also. These stocks provide great stability to the portfolio.

Price climbing is never linear. It has moves in wave. If Gruh falls 20 % in one year, profit may grow 20-25 %in this period. PE will come down below 35 making stock attractive as one can expect yields at 18-20% and dividend yield more than 6% in next 10 years. High quality great company rarely gives this opportunity. Gruh having sustaonable wide moat is a great company. Good finance businesses are “Good company”. Very difficult to get “Great business” in finance sector.

ROE is 28-33 %, it depends on prepayments, dividend payouts, loan growth etc. Presently loan growth came down because company stopped loan against property. Profit growth came down because of DTL. Now low base will take care of growth. Gruh has self sustainable potential to grow at 30-33% because of ROE. But company grows less, it is good for company as it can manage it’s assets and can pay dividends too. High growth hides NPA so GRUH NPA is believable. Long term investors like me can not sell as this great business is part of core portfolio.

In long term stocks give return like bonds. One day if DCF calculation proves that GRUH is going to give return like bond, long term investors like me may think to sell.

I was reading the article about how people who saw great depression had a very different risk outlook for market vis-a-vis people who reached their teens before the great bull run. If Ben graham - whom most of us consider semi-God - had seen these valuations (granted that these are great companies but great business is not a corollary for great investment), he probably would have puked. Yet- we are taking the experiences of just 4/5 years and calling PEs of 35-40 cheap!!! These very stocks were available in 2012 in low teen valuations and nobody was buying.

Sometimes it would be good to take a step back and do some time travel… Would You of 2012 have bought the same stock that You of 2017 considers cheap. I.e. Are we being lemmings!

In Graham’s time, a company with trillion dollar MCap would be freaking unbelievable. Not any more. Times have changed. And Buffet is buying Apple stock heavily - a company already at MCap in touching distance of a trillion dollar. And here people don’t buy HDFC Bank because its too large to grow fast.

Right Gary. I too feel folks are throwing caution in the winds lately.

There are years to buy stocks, years to hold them and years to sell them. Most people who have washed their hands of the stock markets get this timing mixed up, for reasons they best understand. It has nothing to do with intellect. We all have enough synapses to process the essentials of investing.

Normally we discuss whether the stock is at a discount, so that one can buy it. Here in case of Gruh, we all are agreeing that Gruh is “Richly” valued, yet some want to buy it as it best quality. This is not value investing. But, may succeed over the very long term.

If you will, look at Yogesh Sane 2018 portfolio. It makes great sense from a value investors perspective. All low PE stocks, low hanging fruits, yet good stocks. Such a portfolio will almost assuredly give positive returns in the next 5 years.

I believe, it is not about how well the stock will do in good times. Success depends on having the ability to survive the bad times, when the tsunami hits your door step. And it surely will, have no doubts about it. It always does. Another Lehman crises or a Gulf war is always around the corner. That is when weak hands are shaken out of the game. In that situation, the Price of Purchase becomes very important.

Let us be strategic to not become those weak hands. Gruh, too, may fall 50% from its top in severe bearish markets. It is a midcap afterall. And realty market is not exactly booming. It has fallen 30% several times in the past.

The real question to oneself is, If I buy this stock at CMP of 500 then:

a. Will I have the willingness to hold the stock if it crashes 50%? Here the test is not only the percentage of crash but also the stretch of time till the stock gets back on track. If it is 60% of your portfolio, what state of mind will you be in?

b. Will I have more money to buy the stock, when it falls 25% to 50%? This will matter more than any other purchase made.

Hi @pkk123,

First market cap is not the question - valuations in terms of ratios is.

Second, Apple to my mind is one of those non linear bets that are rare and no comparison to HDFC or Gruh. One is pure innovation story and the other is efficiency. E.g millions pay atrocious prices for Apple phones even if cheaper alternatives are galore but would same people pay 1% extra on home loan? Irrespective of how efficient and consumer friendly they may be.

We are creating a halo when none exists to rationalize these valuations. Sure, these are well managed businesses but are they extraordinary where they have extreme pricing power or strong loyalty, I don’t think so.

Let us take a scenario where the Government decides on the following:

Lenders (NBFC’s, HFC’s, banks) will from now on, not be allowed to raise any equity capital for their growth. Capital markets are shut FOREVER. Lenders will have to manage growth through their internal accruals only. No QIP’s, private placements for raising fresh equity for growth.

All lenders will have to compulsorily payout 30% of their profits as dividends. No questions asked. They will have to manage their growth capital with the balance.

All lenders will have to keep their books absolutely clean. Provide for all NPA’s and come to nil NPA reporting. Apart from that, they will have to get a AAA rating from the rating agencies to be in the lending business.

Now with all the above, please grow your business by around 20% each year. Otherwise, your license will be revoked.

The business model of most, if not all, lenders will collapse. Gruh meets all the above criteria. That is why Gruh is special.

Incidentally, Gruh is probably the only lender in the world which has not raised and has no plans to raise equity capital for growth forever.

Management quality is the key. Right now opportunity window with low cost housing is enormous. Company has seldom faltered on delivery front. First mover advantage will maintain Gruh’s premium. Loan is a experience and credibility always goes longer way than me too companies,

The fact that there is nobody as good as the HDFCs and its concerns is already priced in. The current state of expanded PE includes this feature. Now, what happens if at all the PE contracts. Are you prepared, or are you a weak hand and are likely to “fold”? Is the question you need to ask yourself.

And they pay devidends also and generate superior return ratios than most of finance companies.

One has to study and understand how these guys able to do the above i.e; being a lender - no equity dilution, dividend paying and generating high returns…simply their business model is superior than their compititors - This is the crisp answer to the valution puzzle all r discussing.