GRM is an basmati exporter founded in 1974 , based out of Panipath,Haryana

Markets:

Gulf Region,

Europe

North America

Primary export market is Europe(couldn’t find the split, sent out a query, will update once they reply)

Products

**

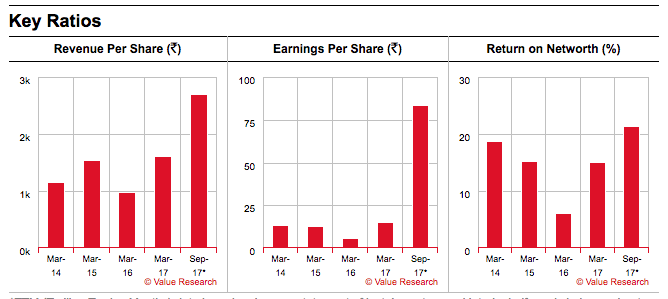

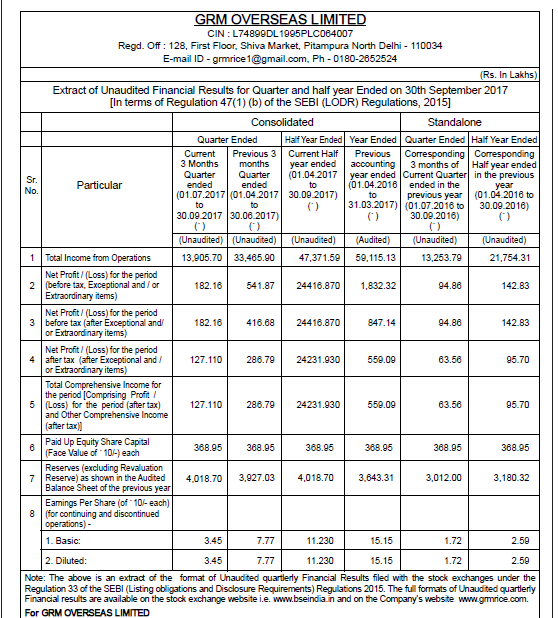

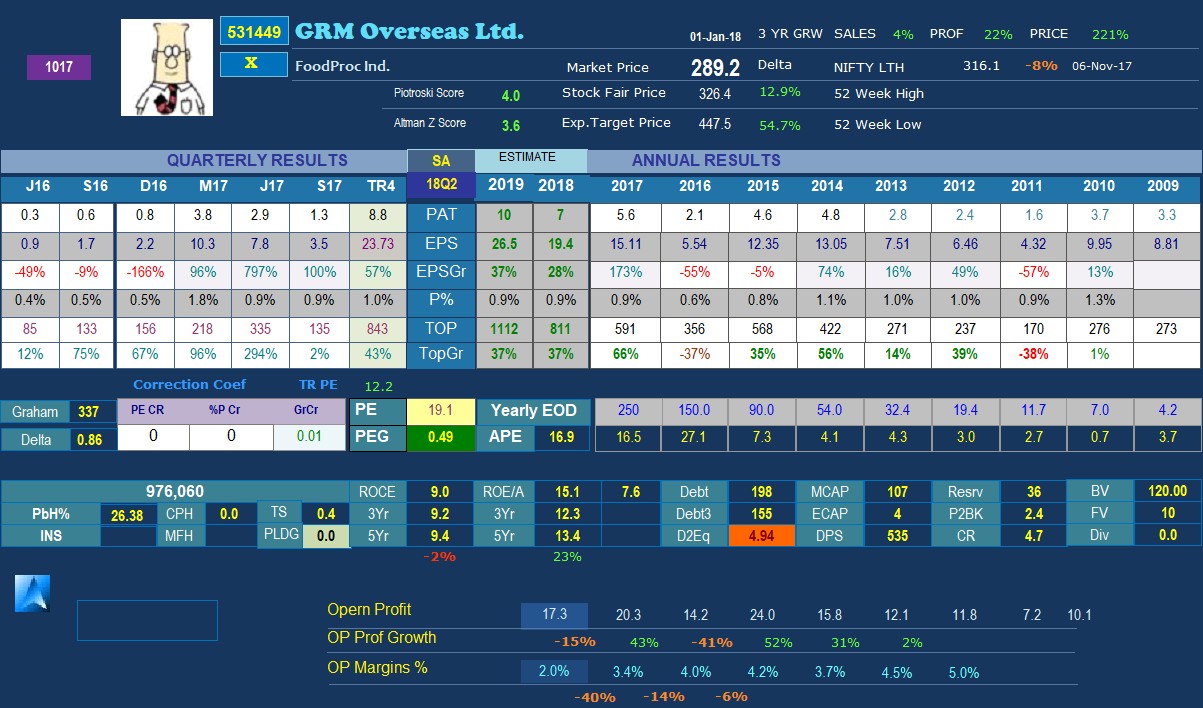

Financials

Board of Directors:

Director Hukam Chand Garg

Chairman & Managing Director Rohit Garg

Independent Director Chetan Kapoor, Vikram Malik, Kiran Dua

Joint Managing Director Atul Garg

Company Secretary Tanushree Agarwal

Share holding pattern:

Promoters: 75%

Public:

Institutional: 8%(All DII, no FII holding)

Retail: 15%

Risks:

Declining Rice demand

Currency risk

High Debt

Low ROCE

Triggers:

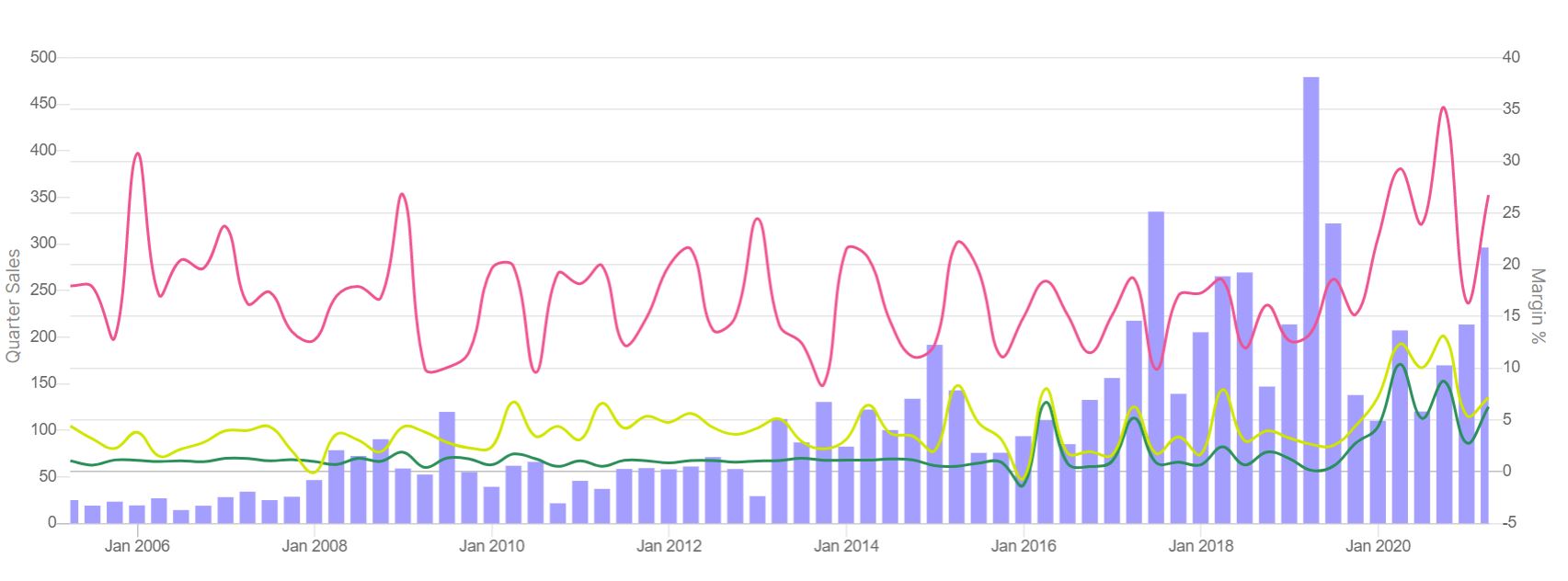

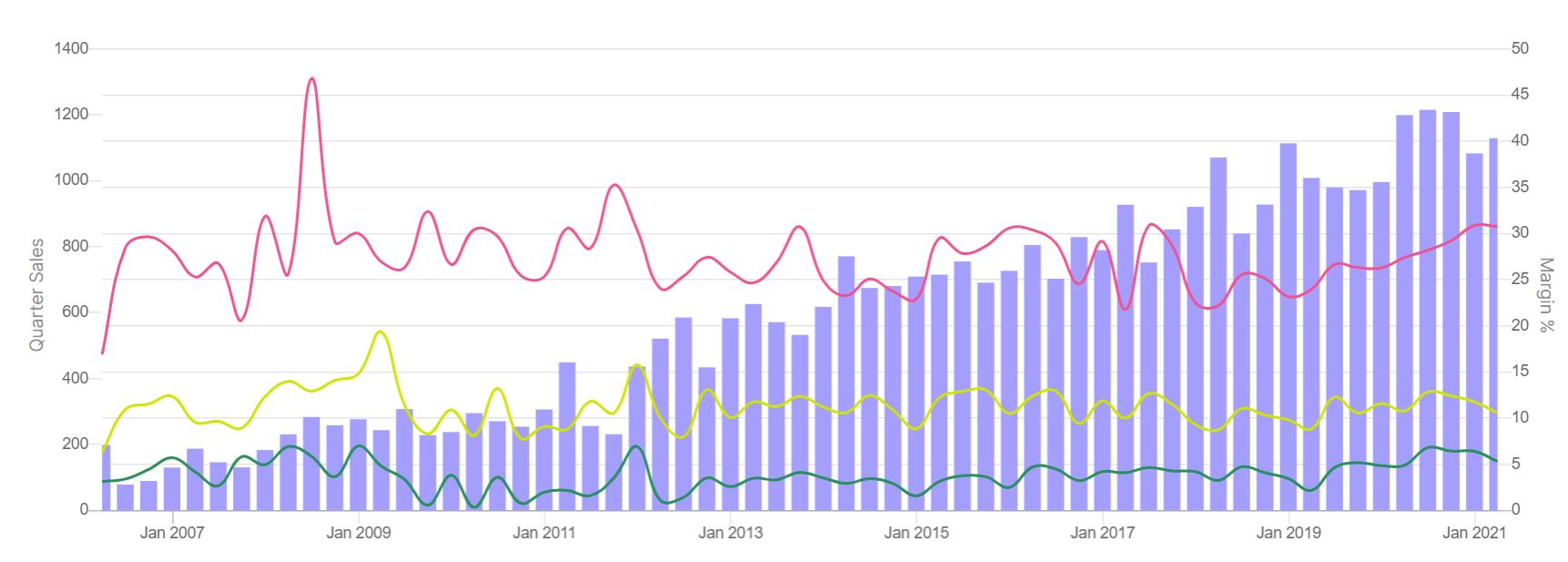

In last two quarter sales have doubled and tripled respectively.

Valuation:

A company giving 840 Crores of sales available at mere 125 Crore is cheap even though the stock have gone up 7-8x in last 2 years

Enough scope for Margin expansion, PAT is mere 1% of sales, OPM in low single digits. If you compare with LTFood, KRBL their PAT is around 5-10% of sales and OPM around ~20%.

KRBL with just 4x sales is valued 120x of GRM Overseas . If you try to valuate by P:BV or EV:EBITDA it’s still half of KRBL.

Some old numbers: https://www.youtube.com/watch?v=jv6f_fMUS6M

Only Sriram Mutual Fund seems to be holding around 2% equity. The other FIs are HFC and HSFC which may be carrying it from early days or it may be debt converted into equity, who knows.

Another important question is that the stock appreciated 5-6 times in last one year. What changed in last few months so spectacularly?

They might face some challenges in the coming season as basmati prices have shot through the roof and they just have 25 crores of inventory left (as per 30 september financials). This is where KRBL and even Chamanlal will have advantages as they will get decent inventory gains.

That being said, they should have had much better Q1 and Q2 I think, wonder why they did not post better results like other basmati companies.

Any views on the management?

GRM OVERSEAS has very good fundamentals and even presentation is excellent but only worry is how come top line sinking and bottom line increases many fold. See June 2020 result v/s June 2019 result.

The valuations that were attractive last year have now become expensive, and GRM is currently trading at 8x its historic valuations.

This said, margins have expanded from 3-4% in 2018 to 7-8% presently. They have been repaying their debt steadily quarter after quarter. Metrics like RoCE and the inventory turnover ratio have improved from 11%/4.03 in 2018 to 19%/8.15 in 2021. Their asset turnover ratio is also 22, almost 4x higher than Daawat’s.

On the corporate action front, they announced a sizeable dividend of Rs. 20 / share earlier this year, and they’ve just announced a 2:1 bonus. They’ve ventured into spices as seen earlier in the thread, but these spices can’t be found on the internet or at any store, so I’d guess that they haven’t launched the products.

They’ve started selling in the domestic market, but they announced this in a very strange way - they said they’ve formed a partnership with JioMart, selling their rice in 45 distribution centres.

At the same time, there’s been some equity dilution this quarter:

**

**