Brief Summary of Business

GESCO’s primary business is the operation its ships on short and long-term leases to third-parties, many of which are based abroad. As one employee explained to me - It’s no different from an individual who owns 10 Innovas which are then put to use. Some of them are operated by the individual for short trips with the fare paid at the end of the trip. Some others are rented out to the customer for a month or longer. Similarly, GESCO owns ships and offers some of them for lease either on a per-voyage basis (e.g. transport crude oil from the Middle East to Europe) while others are leased out to customers for longer periods.

A secondary but related line of business is that of Off Shore Supply where the company operates a fleet of smaller ships transporting supplies, manpower and other support to off-shore oil rigs.

For all the kinds of ships operated by GESCO, the lesee can choose to use GESCO’s crew and maintenance (wet lease) or provide their own crew and maintenance (dry lease) - Wet leases offer higher margins.

Assets/Fleet

GESCO has a decent-sized fleet of tankers, bulk carriers and a single LPG carrier. They do not operate any container ships. The tankers almost always carry crude oil though they can be converted to carry other forms of oil with minimum expense & time. Bulk carriers carry bulk goods in dry form (e.g. coal, iron, wheat etc. that are not packaged into boxes or sacks). LPG carriers are basically floating gas tanks which carry refrigerated LPG fuel in sealed & pressurized tanks.

For off-shore support, the company also owns several small ships and drilling rigs.

Positives

The company’s focus on ships that only transport basic raw materials (crude oil, bulk cargo) has allowed it to survive the current downturn in the market with decent results. On the other hand, shipping companies which have a large proportion of container ships (i.e. carrying finished goods) have been badly affected.

The company is very aggressive in looking for opportunities to sell ships when they get good offers. These can later be easily replaced when other opportunities to buy ships cheaply comes along. For example: FY 2011-12 acquired 5, sold 6 and sold 1 under construction, FY2012-13 acquired 4 and sold 1, FT2013-14 ordered 1, FY2014-15 acquired 3, sold 4 and ordered 3

GESCO consistently keeps a large amount of liquid assets to allow them to quickly act on attractive investments or attractive deals on ships. They frequently lend funds to other companies as short-term loans (few days to a month duration) at attractive rates of interest.

The promoters are very active and recognized in the industry lobbying groups and councils.

The company operates a training center at Lonavala which trains new cadets providing a ready pool of employees of a consistent quality. The school is recognized as one of the top-tier schools in its field in India.

A large proportion of the earnings are in Dollars which is beneficial in the current situation.

The current government is actively encouraging the growth of the shipping industry. While the bulk of the government’s focus is on coastal shipping where GESCO does not operate, the improved infrastructure and goods movement over water will definitely have a beneficial influence in this sector.

Negatives

The bulk of the operational profits comes from tanker leases. This is very dependent on the quantum of production of oil by OPEC. A cut in drilling to stimulate prices will reduce margins.

Bulk cargo profit margins are already very low.

The current low oil prices are detrimental to their offshore services arm.

Senior crew are hard to find and expensive - as an Indian flagged shipping company, employees have to pay income tax in the top slabs which they would not have to pay when working for an international steamer line. As a result the company has to pay higher rates for quality senior personnel.

Management

Overall, the management is above average and is committed to the company as their primary business (other businesses are very small).

The middle-generation (Bharat Seth & Ravi Seth) is taking over the reigns with the partial retirement of KM Seth. The transition should go smoothly since Bharat Seth has been taking an increasing share of the operational responsibilities for quite some time now.

Below the director level, the management is extremely capable and experienced.

Other Points To Consider

The revenues of GESCO are linked to the rates of the Baltic Dry Index which indicates the worldwide trend of ship charter costs. Currently the BDI is at one of its lowest points. I cannot make any predictions on when it will improve since that depends on macro-economic conditions, but I will say that GESCO’s revenues will trail the performance of the BDI by a few months. e.g. If the BDI increases (worldwide average charter costs increase) then as the existing leases expire, the new leases take effect at the higher rates then prevalent.

The shipping industry is one of the few where the layman can easily track how well the assets of the company are utilized. I use http://www.marinetraffic.com/ to search for the current position of the ships in the fleet. A ship in port most of the time indicates poor utilization. Since ships have a very high fixed expenses (you can’t ‘turn off’ a ship like a car or aircraft) every hour in port is expensive. On the other hand the same ship running between the same port pair indicates that it has most probably been leased out. With leasing, the expenses of running the ship are usually the lesee’s responsibility.

Disclaimers

Most of the analysis here has come from my observations and interactions with GESCO and its middle/senior management over several years. I am otherwise not affiliated with them in any way.

I have purposely avoided talking about financials since that is not one of my strengths and I am sure others can do a better job than anything I can do in that matter.

I have a small position (< Rs.20k) in the company and am looking to stay invested over a long term.

Thanks for the write up. I recommend mention as a % of portfolio rather than an absolute amount.

20k may be peanuts for someone with 1 crore portfolio, but 20% of someone with 1 Lakh portfolio.

I recommend mention as a % of portfolio rather than an absolute amount.

20k may be peanuts for someone with 1 crore portfolio, but 20% of someone with 1 Lakh portfolio.

It was about 10% of my long-term portfolio. The %age is even lesser when compared to the overall portfolio.

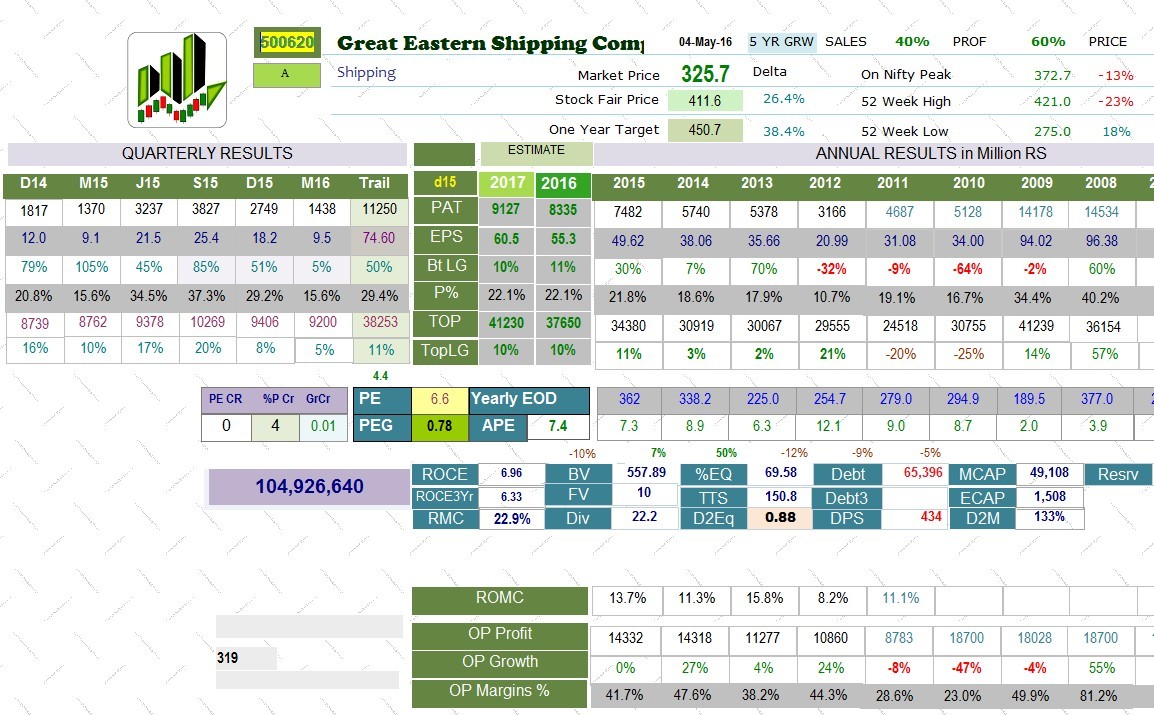

Asset value is at the lowest level of last 25 years

The Great Eastern Shipping Company held conference call on 5th May 2016 to discuss its March 2016 results.

G. Shivakumar, CFO addressed the call:

Highlights of the call:

Tanker markets are still strong after having slow start at the beginning of 2016.

Product market has been subdued.

Chinese imports are up by 800000 barrels per day y-o-y and 400000 barrels per day q-o-q. So tanker market is good.

Gas market is not strong.

Dry bulk market has been hitting the headlines. It hit low in Feb of 290 points. End April it was 700 points. Currently it is at 652 points down somewhat in last one week.

Lows hit in Feb in dry bulk market was very extreme. But dry bulk is not expected to be strong. It will be at current level or a bit lower. Sustained recovery will take at least 18-24 months.

Low price has potentially resulted in high import of iron ore. Also looks like Chinese stimulus is on.

40% price rise in iron ore and steel probably led to improvement in dry bulk market. This cannot last for longtime. The rates are not profitable yet, but it is much better than lows.

World oil demand growth seems to be slowing down. 1.2 million Barrels a day in Q1 against 1.8 million Barrels a day. This was expected anyway.

Crude tanker fleet grew by 1.2% which is quite strong. Last three years annual growth was 1-1.5%.

Average has been pretty strong for crude tankers.

Order book remains for 19% for crude tankers and 20% for product tankers.

Dry bulk the scrapping has been running at a high rate. It expects scrapping of 50 million DWT for the full year.

Order book for dry bulk remains at 15%.

Standalone NAV was 337 per share, down by 10%. Asset value has come off significantly. It has come off by 10% in product careers and 20% in bulk careers.

EMP spending saw 25% cut.

Global Utilization levels are terrible. Global Rigs utilization is 60%. For supply vessel is 50% or so.

The company has priority to look business for idle vessel.

Consolidated debt is under $ 400 million.

Dry bulk accounts for less than 10% of sales. Around 25-30% of its fleet is dry bulk. The company is getting 4 more dry bulk vessels by the end of FY.

Last year Tankers of all kind were very profitable. This year it will be low. A 2% difference in demand supply balance could result in 50% change in rates.

Global Tanker fleet is expected to grow by 5-10% in this year. To absorb this 5-10% the world needs 5-10% trade demand growth. The management does not see this demand coming from anywhere.

During the quarter the company’s oilfield service subsidiaries have recognized impairment charges of Rs 145 crore in respect of 5 offshore assets. In one case the impairment is taken on the basis of the price at which the subsidiary has contracted to sell the asset and in other 4 cases, based on an estimate of the recoverable value of the asset.

The impairment is on all offshore supply vessels.

The management feels that there is good reason to buy assets. Its good to have long term money for long term assets.

Crude tanker has fallen by 10% in past 3 months and it will drop further. Asset valuation will follow trough.

During the quarter the company took delivery of a Medium Range Product Tanker named Jag Padma of DWT 47999 MT. Its built year is 2005.

The company had 11 vessels which were re-priced before 2016.

Provision for cancelled contract happened after the balance sheet date but was provided for during March 2016 quarter.

The company is busy in bearish market because they are tempted to buy at lower levels and the management is contrarian buyer. They might not make money in 6-18 months but is confident of making money in the long run. This is why the company is raising money thru debentures.

Cons book value is 550 per share.

It is not in a position to give consolidated NAV because it has not been able to get valuation of its rigs.

Asset value is at the lowest level of last 25 years without even adjusting for inflation.

Other income contained treasury income. Sometimes the company books it sometimes it does not book it. There is nothing extraordinary in it.

Scrapping was 28 million DWT last year. In four month it has done 17 million DWT of scrapping. Last year also the company started strongly but it slowed as the year progressed .For the full year it expects 50 million DWT of scrapping.

The company is not considering any IPO for Greatship (India) Limited.

Entire market of VLCC ship is 175 ships and in a year 5-10 ships gets transacted.

Total consolidated debt stands at Rs 2884.10 crore against Rs 3069.33 crore in FY 2015.

Subsequent to the quarter ended March 2016 the company

took delivery of a newly built Medium Range Product Tanker named “Jag Punit” of DWT 49700 MT.

contracted to buy a Very Large Gas Carrier (Year built : 1996) of 76,931 CBM for delivery in first quarter of Financial Year 2016-17.

contracted to sell an Aframax Crude Carrier named “Jag Laxmi” (Year built : 1999) of DWT 105051 MT for delivery in first quarter of financial year 2016-17.

cancelled construction contract of one Kamsarmax Dry Bulk Carrier of DWT 82,000 MT, which was scheduled for delivery in financial year 2017-18.

contracted to buy two new shipbuilding resale Kamsarmax Dry Bulk Carriers of DWT 82,000 MT each, for delivery in second quarter of financial year 2016-17.

The revenue visibility for the shipping for FY 2016-17 is around Rs 597 crore.

The operating days in the Shipping division were covered at the following levels–crude at 32%, product carriers (including gas carriers) at 52% and dry bulk at 31%.

Greatship (India) Limited has revenue visibility for FY 2016-17of around Rs 1318 crore.

nice write up bro. Book value more than 550 is definitely a downside protection for the company. At such a low P/E, it is a very good value bet. Also Net Debt to Equity is less than 0.2.

Co has made arnd 2500 cr free cash flow in the past 4 years which they have used to reduce its debt, paying decent dividend (dividend payout ratio is 23% incl dividend distribution tax in FY16) and some money is also used in buyback.

I had a look at this company trading at attractive valuations. As far as I can see, shipping Industry all over the world is struggling due to economic slowdown. Just two days back world’s 10th largest shipping company Hanjin declared itself bankrupt. In India also, Only two shipping companies GE and SCI are profitable and the rest are just struggling. Ship prices are at 30 year low, so SCI and GE are increasing no. of ships they have. Now there are three main revenue areas from ship - Cargo, Charter the ship and resale the ship. Since Hanjin was declared bankrupt there will be a temporary increase in fares for 3 months or so. But overall trend is that shipping rates are coming down due to oversupply. http://www.cnbc.com/2016/03/14/shipping-rates-hit-new-lows-on-excess-supply.html . Ship charter rates are also on downward spiral after a brief surge in 2015. Also there is change in top management of SCI, so that might also be a concern.

GE has offshore oilfield services forming more than 50% of its profit. It operates in the offshore segment through its wholly owned subsidiary Greatship (India) Ltd comprising ~45% of total revenues. The global utilisation level for offshore segment is at alarming 60% levels. Jack-up utilisation has dropped to 70% or lower from ~90% at the start of 2014. In addition to the same, roughly 40-50% of AHTSVs and PSVs are idle/stacked or working spot. Given the exploration and production (E&P) spending marked down for second consecutive year by ~25%, the demand for offshore is expected to remain subdued. The current order book for offshore vessels continue to remain elevated, subdued demand would continue to put pricing pressure on renewals of offshore assets.

For me this company is not very exciting. No matter how good this company is… It’s price didn’t went up in the boom period of 2013-2015 and opportunity cost can be huge in such a case. I’m not expecting it to blow up suddenly. Also this company is affected by slowdown in world trade, so in case of recession, it will be directly affected in a big way.

Disclosure: GESC forms 10-12% of my holdings. Buy Price: 369.

GESC is mainly in two businesses:

Crude and Product shipping + Gas

Offshore Drilling + Logistics through its subsidiary.

What I feel positive here is that when the crude oil prices are up, bringing the Baltic wet tanker index down, the offshore drilling+ logistics business should pick up…since people would be wanting to Drill more oil then.

When the crude oil prices are low the Crude and product shipping business should shoot up, owing to the increase in crude stock piling and also refinery products. Also the fuel charges would decrease improving the margins.

Also most of the crude and product tankers are on a Time charter meaning on a contract for about 3-4 years and hence the ups and downs of the freight rates shouldn’t ideally affect the revenues. But it does anyway. This could also be negative for the company because in times of very high freight charges the company might be forced to ferry for the already agreed rates according to the contract.Since most of the ships are bound in a Time charter.

The Dry bulk business is down due to China having reduced the imports of iron ore due to the steel fiasco. Since iron ore imports used to be the main item of trade here. But this business contributes to a very small amount to the revenue. Hence I am not sure if this is important here.

I feel the trouble of the company is during times such as presently. Right now neither is the crude rate too low nor is too high. Hence stock piling etc is down affecting business 1. Similarly due to the price not being too high I feel the drilling activities too are hit, affecting business 2.

In other scenarios GESC seems very well prepared to handle the two extremities with the only difficulty being in times of moderation such as these.

I have a very different approach in looking at GE Shipping.

As has been mentioned above, the company is at a historically low NAV, is a very efficient capital allocator and has acknowledged operational capabilities.

The high discount to NAV is where the margin of safety comes in from. Also, in shipping industry the NAV of assets is a function of the shipping rates and the new asset addition globally. GESC in this terms has a clearly stated goal of buying assets when they are cheap and disposing them off when they are expensive. In addition, the strength of the balance sheet helps them to pick up assets in the downturn easily. In the latest con call, the management also expressed desire to take up debt if they run out of cash and still see assets available at cheap valuations.

If you want to bet on a good management + great capital allocator + efficient execution, GESC is a good candidate.

Now, if you buy now, how will you make money. So, my thesis here is as follows. The recovery in shipping may take time but it will be there as its supply-demand economics. With recovery, two things will happen simultaneously. The NAV will rise and so will profits. This will be a typical cyclical play, and if one keeps track of NAV and company actions, there will be a good opportunity to exit with a handsome return.

Came across your post wherein you have taken a position in GE shipping last year. Wanted to seek your views to understand this better.

I like this company and it is possibly available at good valuation. Keen to understand views from experienced members to understand why the mcap will rise even if profitability were to improve

As you can see, across a long period 10 years, the market has not rewarded this company. Market cap has not grown much. Wanted to understand your thought process why do you think market will reward this company with growth in mcap ?

The steepening in oil price contango and filling up of land based storage is positive for oil tanker companies. Most US and Asian listed tanker stocks doing well today.

Good insider buying in GE Shipping recently as well.

I was also following the oil contango and feel that tanker rates are going to go up significantly benefitting GE shipping. But dry freight prices may go down. But that may be manageable considering the cost of fuel. But the company has a good income from E&P activities in offshore oil rigs. This is expected to come down due to lower crude oil/ natural gas prices. Came across this in Hindustan oil exp management disclosure to exchanges. We may be able to make a better decision if we have a percentage wise contribution from each of this segment viz, wet freight, dry freight and E &P activities