Can clock FY18 revenue over Rs 1000 cr; margins sustainable at 11%: Gravita India

Gravita India is in focus after reporting a good set of Q2 numbers. In an interview to CNBC-TV18, Sunil Kansal, CFO of the company spoke about the results and his outlook going ahead.

3 Likes

2 Likes

China banning of importing recycling materials from US few days ago. Could this be a huge business tailwind for Gravita ?

Here is the news - https://www.npr.org/2017/12/09/568797388/recycling-chaos-in-u-s-as-china-bans-foreign-waste

1 Like

This is why I am fan of this company… Continues upgrade in business… Looking for vertical growth. What more need shareholder need…dividend is peanut against company growth and converted to share Price

1 Like

Gravita hits 52-week high, starts commercial production of Red Lead Oxide from Jaipur plant

Download moneycontrol app: http://m.moneycontrol.com/mom

2 Likes

Edged out of the downward trendline this week and breakout showing strength today. Close above 172 will be nice.

Disc: Invested

Sales Growth = 50.09

Profit Growth = 83.86

ROE = 23.26

Dividend = 0.6

CF Operations = 6.24 cr

Debt To Profit = 35.3%

EPS = 6.67

News is a bit old (March 20th, 2018) however very relevant for Gravita…

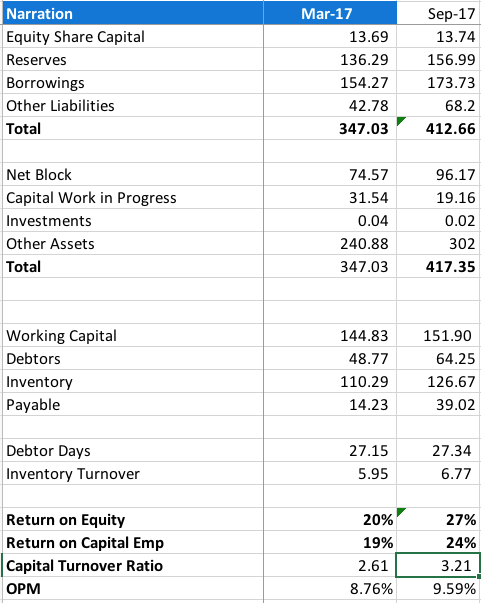

Going by the half-yearly balance-sheet and TTM figures, RoE and RoCE are already visibly up.

Capital Turnover ratio is the main contributor and that has to do with better capacity utilisation in the Chithoor plant along with better realisation for Lead. I think on average Q3 and Q4 figures for lead realisation should be identical and as long as it stays at these levels, the company should be doing good. Have to wait and see how PPCP contributes to the bottomline. With the increased lead capacities going into FY18, if lead prices stay up, FY19 should be just as good but got to be watchful.

Disc: Invested

3 Likes

Hi All, The question may not be related to Gravita but related to the recycling industry in which Gravita is placed.

Are there any players in the copper - recycling space, this is keeping in mind the revolution of EV and the demand of copper in the future.

Any inputs much appreciated.

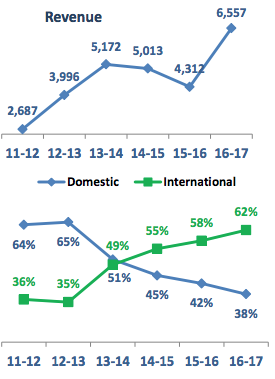

Gravita’s export revenue contribution has gone up in the last few years and last year it stood at 62% (404 Cr exports vs 656 Cr Overall).

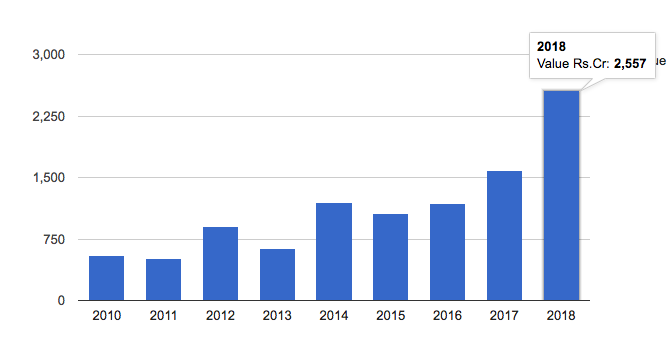

Indian Lead exports from FY17 to FY18, have grown at a whopping 61% (1586 Cr to 2557 Cr)

In that, Pondy Oxides’ Annualised growth based on last 9 months has gone up only about 20% between FY17 to FY18. Their capacity utilisation must be at peak, going by last year’s AR.

For Nile, the annualised growth is at just 8% which means they must be at peak utilisation as well.

Meanwhile, Gravita’s Annualised growth based on 9 months is at 33%. Gravita’s Lead capacity for FY18 is at 1.07 lakh MTPA and the company was using only about 65% of its capacity. There seems to be a good chance hence that Q4 numbers could show very good growth for Gravita.

This is of course completely priced in, since Gravita is trading at 28 P/E vs Nile and Pondy’s 8 P/E levels.

6 Likes

Gravita India Limited, a leading recycling company having its manufacturing presence around the globe, is glad to inform that company has signed a contract with Amara Raja Batteries Limited for Lead Acid Battery Scrap Collection and Recycling arrangements. Under this contract Gravita shall collect/purchase Lead Acid Battery scrap from designated locations of Amara Raja.

Gravita targets supply of approx. 8000 MT of Lead to Amara Raja under the said contract which will help the company to strengthen its top line in FY 2018-19 coupled with cost effective recycling and long term business association with Amara Raja.

Gravita India Ltd Board to consider Final Dividend on May 28, 2018

2 Likes

Gravita credit rating improved/updated (brickworkratings):

Long Term: BWR A

Short Term: BWR A2+

I think Nile’s poor showing in Q4 with Amara Raja as their main customer - 80% of all revenues coming from them has something to do with this. They anyway lacked pricing power with Amara Raja. Gravita’s Chittoor plant being 70kms away from Tirupati must have played a part is grabbing that market share from Nile. Its also important to know what sort of contract they have gotten into because Nile definitely didn’t have one that was advantageous for them as Amara Raja has squeezed them well in the past. Nice development nevertheless.

Revenue growth has been very strong. Although, margins have disappointed. Mixed result.

However, the current order book of 500cr to be executed in FY19 (FY18 revenue 362cr) and the tie up with Amara Raja warrant a buy/hold.

Disclosure: invested

Investor concall was positive on current capacity utilization, new capacity addition (about 45000 tonne incremental capacity for lead by Dec 2018) and future prospects (growth in turnkey projects contribution).

Company also focusing on working capital days reduction (current 84 days, target 45 days in 2 years), debt restructuring (int rate going forward 8.5%) etc. to bring down finance costs.

Besides, due to the roll out of GST and Eway bill, scrap sales are moving from unorg. to org sector. Due to this the company is getting more scrap than it can handle (7000 tonnes from 5500 tonnes earlier).

On the lower margins for Q1, following explanation was provided by management in the cocall:

For Q1FY19, lead volumes were around 15,500T. Out of that around 5000T aggregating 33% of Q1 production was using Re-melted Lead + cable scrap. This has lower margins of around 4% compared to 8-9% for battery scrap. Company had to use RML due to limited availability of battery scrap, combined with high demand of lead. This pulled down the EBIDTA margins for the quarter

what could be the reasons on huge difference between cumulative CFO and Cumulative PAT.

Cumulative PAT from Mar’08 to MAr’17 = 144cr and CFO for corr…period is only 42Cr

1 Like

Very interesting observation. Could you pl share the source of data.

I picked it from screener.