How does pledge impact the stock price? So long as the interest n principal repayments are ok, pledging shouldn’t impact

@vagator10 : Answer is there in your statement itself. Its safe as long as Interest and Principal are going. Assuming promotors majority income is from Dividend and Salary. Incase of any short term downtrend company doesnt do well for couple of quarters then dividend income could be hit and repayments affected.

Another scenario which happened recently, due to overall downtrend in market itself, share price got hammered and Promotors had to pledge more shares as collateral for the borrowed money. What if promoters didnt had more share, bank would have sold the pledged ones in open mkt severely affecting the stock price.

Operators can take advantage of situation 2 and try hammering the stock so much that Promotor runs out of options and eventually Bank had to sell to safeguard its money.

Excessive Debt in any form is bad !

7 Likes

Very well said. The eps growth seems to suggest that the business is earning above the cost of borrowing,( of course we know that they’re capitalizing the interest cost). With the stock price having rebounded, it remains to be seen if pledge goes down or the promoters use the price rise to raise more debt.

1 Like

D/E is ~0.8. the ratio per share matters

I couldn’t get the debtors ageing in the AR. It’s an area of concern. Can someone share it if u have?

I looked up sales of zantag but couldn’t get more info. This is used to treat heart burn and stomach ulcers or acidity

It seems that it was about 125 million USD last year https://www.statista.com/statistics/194544/leading-us-antacid-tablet-brands-in-2013-based-on-sales/

However I am unclear on multiple accounts and so not able to infer something meaningful. Here are the reasons

1- The title of the article says that stat is for 2103 while the page content calls out distribution for 2017 (may be a trivial content issue)

2- I do not know what percentage of this sales could come to Granules over the next one year or so. Typically when generic drugs are launched then price falls by about 60%. In this case I am unaware if generic drug is already launched or this is the first one. If there are other generic drugs already in the market then price would not fall else price would correct. In any case Granules has to fight out to capture market.

Nevertheless, it’s a good news.

Cheers,

Krishna

2 Likes

Did anyone attend the AGM? based on recent upswing in price / volume… excited to know management’s views / future plans

Price action doesn’t mean anything relative to an event. There was no news to back this move so the stock might go back down.

It’ll be more productive to discuss the AGM takeaways if anyone attended.

MF holdings have shown north ward movement from last 2 months… it is interesting to note that it was on decline during May-June & has turned reverse in July-August

The no of MFs holding our company has gone down from 18 to 16. Interesting entrants are Kotak & BNP while L&T and SBI have made exit

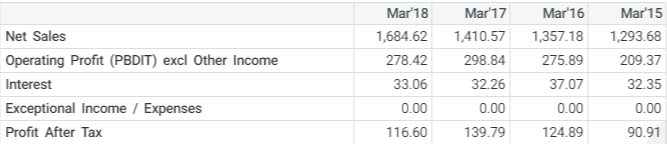

Super Result

https://www.bseindia.com/xml-data/corpfiling/AttachLive/a0334bb2-4f8b-47c5-af2d-477ccc416ab5.pdf

2 Likes

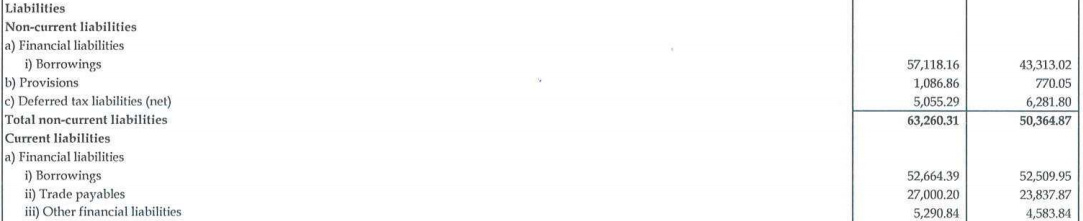

The balance sheet is concerning. Debt increases over each quarter. People who rejoice blindly seeing the net profit growth should analyze more.

1 Like

They capitalize portion of the interest and hence it appears optically lower.

Last 4 years the interest paid has not seen major change, where do you track the other outgo w.r.t. capitalized portion of borrowings

Few positive notes from Q2 concall

- U.S. sales were INR 46 crores, EBITDA of INR 16 crores

- Management is confident that debt will definitely not increase

- Debt reduction of 200 Cr by 2020

- Share pledged : Planning to reduce almost like 30% or 35% of the personal debt (pledge) in this financial year and reduce / remove it totally in the next fiscal

- Our company borrows in dollar, pays back in dollar. So overall, ForEx fluctuations don’t effect us

5 Likes

How do you think he will reduce pledge by 30% in next 5 months and by 100% in next 1 year from then ?

- By selling his existing real estate holdings ( if he has it )

- By selling a portion of his equity stake to interested buyers (big pharma )

- any other ?

1 Like

Thanks mrai74 for putting short notes from the earnings call. I too attended the call, and would like to add some more notes (sorry about some repetitions)

1- The topline growth (48% yoy) came from Paracetamol and FD contribution. Bottomline grew 49% yoy.

2- The margins on APIs would improve once the newly added capacities are FDA certified. It should happen by Q4. At present a lot API coming from the new capacity is being sold to domestic players (reflected in results) which do not give premium price.

3- Increased depreciation because of new capacities.

4- GPI contributed: Sales of 46 crores, EBITDA 16 crores, and PAT 7 crores. Major part of R & D expensed to P&L and so optically margins look lower. (Nice that they are charging P&L for R&D). Overall at consolidated level out of 54 crores of R& D in first 6 months of which 27 crores charged to P&L.

5- Validation of Onco APIs will start from the last quarter of current FY.

6- Rx market - Metformin and one more tablet launched in US with own brand with no support from external marketing company. Shall increase the profit margin.

7- Pre-approval inspection of GPI, Two procedural observations. Will reply within this week. Will expedite the approval process in future.

8-Biocause: For Q2: EBITDA = 38 crores, PAT 15.5 crores and Granules share half of that.

Omnichem: Sales 17 crores, PAT = -5 crores, Granules share: -2.5 crores

9- CRAMS is cyclic and expect upturn from Omnichem in next quarter. Next four years we can see 30% CAGR both rev and PAT from Omnichem.

10- Capex guidance => No new Capex except the routine maintenance stuff. When Onco capacity comes to traction then this would be used. All this would be handled through internal accruals.

11- Total debt about 1120 crores. The debt will not increase further from here. The debt to come down 900 crores by end of year Mar-2020.

12- Pledge: The debt was taken to fund the growth. Reducing the pledge by 30-35% in this FY. And next year will completely remove it.

13- GPI => The approvals will start coming from Q4/Q1 .Metformin the approval will come by Q4

14- Constant increase Q-O-Q from China, but company was able to pass on the increase to the customers with a lag of one quarter.

15- 19% EBITDA margin is something we should be seeing in few quarters. As soon as the utilization of capacities increases.

@reacher: Fair question but I do not know the answer. But promoter would get dividend along with other shareholders, and he may have other sources of income. Equity dilution was not discussed and I believe is not something promoters are thinking of at all.

@vagator10: In the last two earnings call promoters have been talking about 1100 crores of debt and bringing it down to 900 crores by Mar-2020. The recent increase was for Onco and was per plan.

Finally, I both reduction of pledge and debt need to be watched carefully, along with growth.

Cheers,

Krishna

Disc: Invested

5 Likes