The quarter wise price trend is still northward (although eased a little bit in last few days but overall its more than previous two quarters) . As we have just 3 weeks left in this quarter, is it safe to assume that current quarter will also have impact on bottom line until unless management is able to pass on all impact to customers. I am aware that they confirmed that they pass on this burden with lag of a quarter.

Views from seniors invited, which seriously impacts our investment decision

Will get passed on with a quarter lag one way or the other, so no medium term impact. In any case things like acetic acid are probably more important than crude for their P&L. Crude can definitely impact on a quarterly basis but I would not think of this stock as one where there is any story in next 1-2 quarters, it is a longer play.

Not sure if it is a good thing or bad but I am pretty much incapable of thinking on quarterly basis for any company, I strongly believe that one should take a minimum 2-3 year view on a business. If the idea is to trade, one is better off looking at charts than numbers.

Management has guided for 19% ebita for first 3 qtrs of fy19 and 19+ margin for the last qtr. At the time of giving the guidance, the crude had already ran up from last qtr level so I don’t know what gave confidence to management to give 19% margin . With 1 qtr lag I would think that it would have some impact on this qtr as well before it stabilize

Agree. Crude technically has been correcting since 20/5 now and hopefully if any further meaningful correction will provide more impetus to Granlues at CMP…Believe they had a stronger pipeline deployment in 2019/20

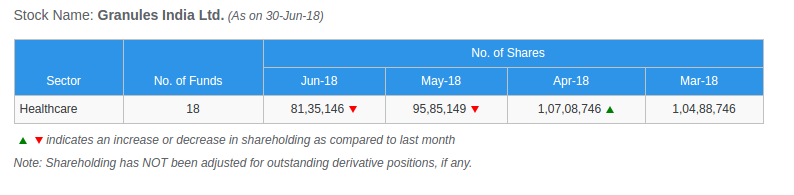

The shareholding pattern invites some interest as we see that despite prices being hammered promoter holding keeps on going southwards. They offloaded .05% which is passed on to public holding. Another point of interest is FIIs loosing interest on a fast pace as they have offloaded more than 2% of their holdings. Next point of interest for me is Individuals category, where Big individuals (More than 1 Lacs) have also offloaded 0.15% shares while the small investor category (up to 1 Lacs) has increased its holding by 2.33%. It clearly shows that big guys (including promoter, FIIs, institutions, corporate bodies & even high net worth individuals) have offloaded on cost of poor small investors who get attracted due to huge correction and are still hopeful of smart recovery towards life time high or even higher

As these are basic health drugs which Amazon sells, I assume this further reduces the margin of pharma companies and distributors.

Would this have a negative impact on granules or would the companies plan to procure the rm, pfi from low cost producer like granules… To stay competitive.

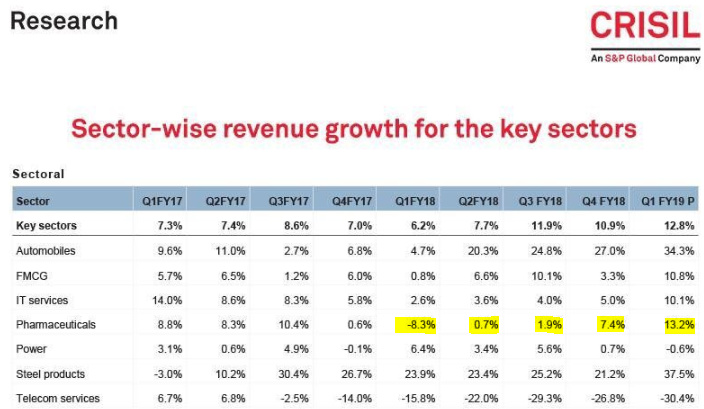

Revenue growth projected for pharma by CRISIL is encouraging for next 4 quarters. It shows that worst is almost over. Let us hope that our company gets better part of projection

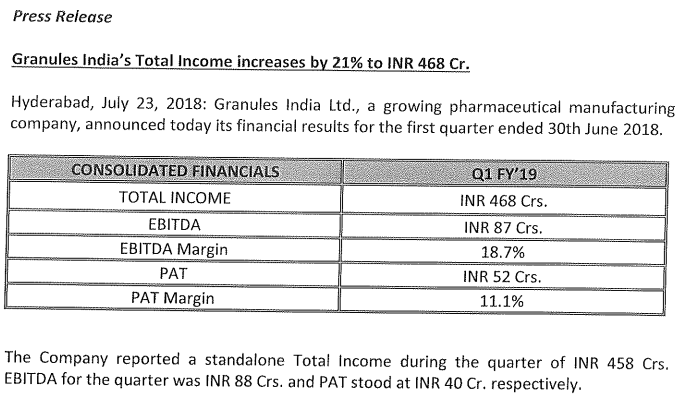

Fantastic bounce back by Granules. 18.7% EBITA margin from 8.6% last quarter. Profit from Joint venture and associates at 14.6 cr is a big suprise. This was 3 cr last year in the same year and 15.9 for entire last year.

Just putting the nos in my view & inviting serious discussion towards pledge in our company.

Market Cap is approx 2600 Cr (current valuation) & Pledge is almost 550 Cr (based on Jun valuation - we have seen some uptick since then). The pledge is more than 20% of total Mcap.

We can see that pledge % has seen major swing in last 4 quarters, where it went down to 31.6% from a whopping 78.1% but again started moving ahead at faster pace in last 2 quarters to inch back to 60.4%

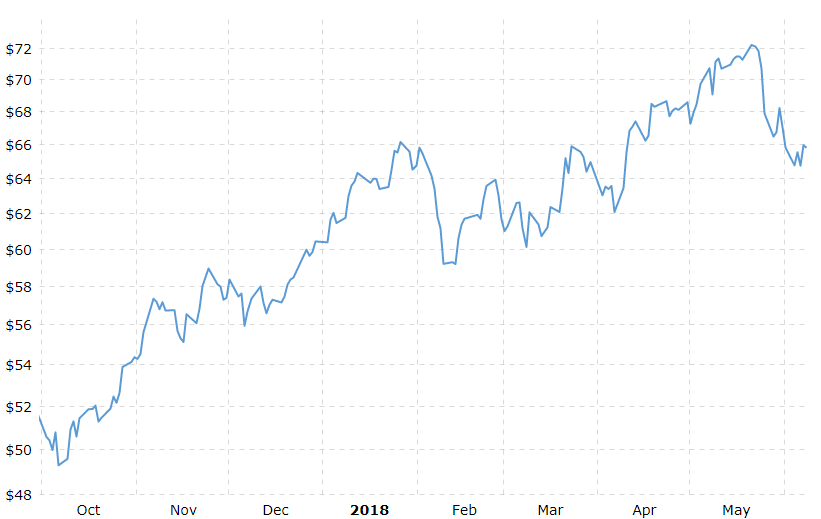

While comparing it with price movement (although prices don’t move ONLY due to pledge & are controlled by various other factors), we observe that price was stable during Jun’17 - Dec’17 (pledge was stable at 78.1%) & we saw big upmove in Jan’18 (pledge went down to 31.6%)… later Jan’18 onwards prices have nosedived alongwith increase in pledge. I am aware that Jan’18 was the key & has impacted most of midcap / smallcap badly due to other widely known reasons.

Can someone pull & publish historical percentage / graph of pledge percentage as it has been swinging up & down. We can co-relate the swings to market scenario / critical events impacting pharma business. This may give in-depth analysis and will pave way for long term investors.