Can this company grow its profit 25% for next 5 years on annualized basis? What do you think

Actus turnaround is the key and if that happens, this may chime for 1-2 years. 5 years is tough to predict in my view

@pumba22, pls go thru the earlier posts in the thread. Kalyan and other senior boarders has beautifully analysed the company business, expansion plans and future opportunities. You will get your answers.

Regarding the market mayhem, I see a pattern similar to the 2008 crash. In 2008, the big boys corrected and went sideways. However, the mid-caps corrected for a few months more, the correction continues for a longer period of time. Similarly, I believe all the mid-caps (including the good names) will correct further over a couple months, and will present good fishing opportunities.

Discl : I am not an expert in anyway (technical or otherwise), so pls do your own due diligence. Invested from lower levels and tracking to buy more.

Yes. It can grow sales at 20-25% and profit at 25-30%.

Discl: Holding as major % of portfolio.

Hi Amitayu.Yes GIL is a b2b. I don’t know specifics for fda observations for b2b. I do know that the observations could be as trivial as a leaky sink! Worst that could happen is that the fda could impose sanctions on a particular facility which won’t allow imports in the US (and maybe few other countries who rely on fda standards) from that particular plant (Jeedimetla in this case). Being a b2b company, it is rare to get serious fda observations which is difficult to rectify within 15 days as the big companies to which granules cater, do their own inspection and hence ensure that the facilities of granules are at their best standards.

Disc: more than 50% of my current portfolio. Would be gradually reducing the allocation through fresh cash pumping in other stocks.

1 Like

I got following response from Company “Nature of observations were related to procedural matters and you can seek further information from USFDA under Freedom of Information (FOI)” … Have not explored yet on FOI procedure …any idea?

@ SushilKC FOI precedure is sort of RTI in USA.

@nishantkandoi Did some scuttlebutt from a Pharma compliance guy .Came to know that 90% FDA warning which Indian company received is on Data Integrity Issue which could be resulted to import alert . By listening those type of issue , it appears it could be easily avoidable if they adhere some basic security guideline like shredding the document after use , justification on overwriting etc . As an IT guy , I just wonder why pharma company don’t take this security issue not seriously where as all the big IT companies knows well that US,UK take this data issue very seriously and to overcome this type of issue they have strategic partner with US compliance company who does very rigorous auditing before the actual audit take place .

2 Likes

http://www.moneycontrol.com/stocks/reports/granules-india-financial-resultsresults-press-release-limited-review-report-for-dec-31-2015-2725121.html

So so results…345 vs 320 and 27 vs 23.5 Cr (y on y)…could have better…at least on the lines of Q2

PS - invested

1 Like

Kalyan,

Operating performance is much better (up 21%YOY)

Higher taxes have taken the toll on net profits

Concall should be interesting

3 Likes

Here are my notes for the concall. Requesting fellow members to add/correct. I have missed some things.

FDA observation is procedural in nature

- Complaint investigation…how we investigate a complaint

- Quality (didnt understand fully)

- Cleaning of equipment

Track record of Granules has been good. In past few years they had a number of USFDA inspection out of which 50% were no observations and a few were cleared without any escalations. They are confident of clearing USFDA issue.

3 US DMFs are filed from Jeedimetla…Contribution to revenues? (didnt understand, but is important) 60% for 3rd party, rest for captive.

Lower revenue was due to 3 reasons…

- Rationalization of Auctus portfolio.

- Decline due to oil prices…selling price is linked to raw materials but margin is preserved as fixed absolute number per kilo.

- One of the Customers has some problems in quality and their sales slowed (maybe DRL/ Cadila??)

Confident of 15-20% revenue growth in FY17 and better bottomline growth (EBITDA margin >20%). Want to generate cash and use for long term growth.

Better product mix resulted in better margins. EBITDA margins will be sustainable for the full year, not Q-o-Q

Auctus(new API division) breakeven…made 20lakhs profit. There will be marginal profits only from here to keep the plant going. Real growth will be seen 2-3 years from now. Currently selling to emerging markets. Next yr revenue maybe 200cr. Phased out 2 low margin pdcts out of 14 pdcts.

Ibuprofen ANDA sales started (Q3 rev 15cr). Market size 2-2.5bn doses or 400-500cr. 150-200cr in nxt 2 years. Amneal, DRL are major players, now Granules too.

Tax rate 36%

- JV incurred loss of 1.31cr. Its an SEZ plant so cant take tax credit

- Third party R&D expenses are not eligible for tax exemption

32% will be tax rate going fwd.

Warrants…1 tranche fully completed, second tranche 25% money paid, some will come in Q4 (due to money requirement by company) and rest in 2017.

Capex 450cr for following

- API Metformin expansion

- Green field API facility in Vizag (construction to start next yr, total 150cr capex )…

- Prodct development

- USA subsidiary GPI (bought last year, renovated, started R&D) etc

70-80cr capex done yet in FY16. Total this year will be 90-100cr. Next year will be higher. Gross debt= 348cr long term, WC loan 114cr. Started paying 15-20cr per year.

Utilizations levels-

PFI- 70-75%

API - 100%. Paracetamol capacity expansion of 3000MT started in December

FD- 50-55% utilization. (Metformin and Ibuprofen are 50% of total FD sales)

PAR pharma agreement for in licensing of their prdct. Marketing on profit sharing basis in USA. This will be for OTC market going to Walmart etc chains.

OTC is very small and building up. This will be a big market in 3-4 years. FY18 will make us happy for OTC. Till now OTC market was dominated by 2 players. Bidding process takes place but Low price is not the only criterion. They have Very short delivery times and consistent supplies (logistics) are very important. Currently 4 pdcts, will go upto 10 in 3 years

Omnichem depreciation loss of 1.7cr on 1.3cr revenues. 150-200cr target in FY17. EBITDA margin target 20%. Plant and product waiting regulatory approval. Currently supplying intermediataries to Belgium. Ramp up with intermediataries will be visible in Q1 FY17 even without approvals. After approval it will be higher. 40-50 cr for the 2016 on JV level.

Abacavir sales 4.1cr. YTD basis. 30-40cr target is too optimistic and wont be possible

Next year will be flurry of ANDAs filings. Launches will take some time unless there is in-licensing of some ANDAs.

ANDAs filing fee will be charged to P&L. Development cost will be capitalized.

10 Likes

As per ,Granules Board Meeting , They have approved further investment of USD 1.8 million by way of debt/equity in Granules USA. I have some questions .If the investment is through Equity dilution then I am calculating the effect on EPS . USD in 1.8 million means 12.24 crore which is basically 0.5% of total market capital of Granules i.e 2400 crore . So will EPS be affected by 0.5 % ?

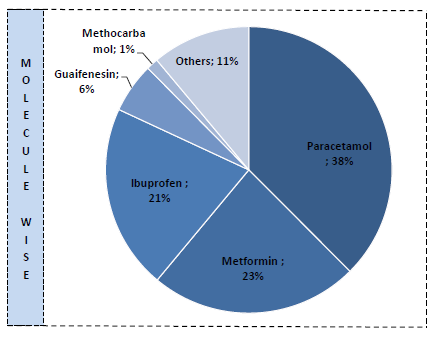

Other info from presentation

Future Growth from existing portfolio

- Increasing emphasis on finished dosages will increase revenue and profitability

- Growth will be driven by larger wallet share from existing customers as well as new customers

- 4,000 TPA PFI capacity added during the current year.

Capacity augmentation of APIs in base molecules: (already under implementation)

-Addition of 7,000 TPA in Metformin capacity to reach to 9,000 TPA

-Addition of 2,000 TPA in Guaifenesin capacity to reach to 3,200 TPA

-Addition of 3,600 TPA in Paracetamol capacity to reach to 18,000 TPA through debottlenecking

Omnichem Progress and timelines

- Project is completed and commercial sale has started.

- Supply of API intermediates to Omnichem (JV partner) till the facility is approved by regulatory authorities.

- Currently working on 4-5 products

4 Likes

IMO the Granules’ mgmt was never a top notch but they are into simple products so it did not matter much. They are not into developing any exclusive IP. Whole investment thesis was based on capex and efficiency led growth and if it starts faltering, one might have to look for alternatives.

Disc: Invested from lower levels

1 Like

Dear all, refer: http://www.thehindu.com/todays-paper/tp-business/new-us-rule-a-blow-to-indian-pharma-exporters/article8185521.ece

As per this, my understanding is that the formulations which are purchased by US Govt are expected to have their APIs manufactured locally in the U.S. Earlier, I believe, they were only insistent on having the final formulations to have been manufactured locally in the U.S.

Indian institutions are taking up this matter with their US counterparts. However, suppose, this rule comes into effect, then I wanted to understand the impact on say a company like Granules India.

For this, I was thinking, who are the API customers of Granules India.

Even if I’m able to collect the names of companies which source their APIs from Granules. We still don’t know if those companies finally end up selling to U.S. Govt. If yes, then these type of contracts that Granules has with US companies to supply APIs, might be impacted, as this new rule wants the APIs to be manufactured locally.

Could someone throw light on what is the potential impact or a way to go about estimating this. My intention is to be able to categorize if this is a non-serious issue or not.

Discl: Invested in Granules India

1 Like

This might be applicable to only government suppliers.

Nothing to worry about i guess.

If any one have better understanding, please share your views.

1 Like

post API supplies the formulation is made in US only , so the criteria is already met

All countries are getting into protective mode.

India is also opinion of restricting API import

Disclosure: Heavily invested in pharma