Godrej Agrovet Ltd. (GAL)

Introduction:

- GAL incorporated in 1991 as an Agro based company focussing on Research and Development. Company operates in five verticals namely animal feed, crop protection, oil palm, dairy and poultry & processed food.

- Company started its journey with three key verticals initially – animal feed to improve yield of Indian livestock, crop protection to address low productivity of Indian agriculture and oil palm business to benefit from PPP model to reduce dependence on vegetable oil imports.

- Later on company ventured into poultry business under “Real Good Chicken” brand and processed food under “Yummiez” brand and in 2008 entered into JV with Tyson India Holding Ltd., a subsidiary of Processed food giant- Tyson Inc., USA to grow its poultry and processed food business.

- To venture into emerging dairy business, company acquired 52% holding in Creamline Dairy in 2015 and spread its presence across value chain from feed to food

- Basically GAL is into 5 business:

o Animal Feed

o Crop Protection

o Oil Palm

o Dairy business

o Processing food

Business reviews:

- Animal Business:

- In animal feed business, its portfolio of products comprises cattle feed, poultry feed (broiler and layer), aqua feed (fish and shrimp) and specialty feed.

- Company’s animal feed products are manufactured at 35 facilities, of which 10 facilities are owned by the company, and seven are operated by the company. These facilities are located near major consumption centers across India, with an aggregate production capacity of 2.36 million MT per annum, as of June 30, 2017.

- Company’s pan-India distribution network for animal feed products includes approximately 4000 distributors, as of June 30, 2017. Its 50:50 joint venture, ACI Godrej, was incorporated in 2004 and produces cattle, poultry and fish feed in Bangladesh. ACI Godrej operates two manufacturing facilities with an aggregate production capacity of 0.57 million MT per annum, as of June 30, 2017

- Installed capacity and Utilization:

2015 2016 2017 Q1 FY 2018

Installed capacity 35,280 35,280 47,880 47,880

Utilization 40.28% 46.69% 36.46% 42.27% - Company will be focusing on achieving cost leadership by improving the operational efficiency of animal feed business through R&D as well as cost rationalization.

- Company’s R&D efforts are also focused on developing innovative livestock nutrition products that gives the product differentiation, which will help in improving profit margins and market share.

Industry Outlook: (Analyst Meet) - Feed industry has been valued at 26 lakh crores as of 2015 globally and China is the largest producer of animal feed contributing 19% of total sales volume, followed by US and EU.

- Poultry Feed accounts for the largest share at 45% followed by pig segment at 20% and cattle and other at 20%, aquaculture which includes shrimps and fish feed accounts for 4%, others at 5%.

- Animal compound Feed industry in India is valued at 72,000 crores in FY17 and is expected to grow at a CAGR of 13% to reach 106000 crores by FY20.

- Among the 3 segments aqua Feed is expected to grow the fastest at a CAGR between 15% to 16% followed by poultry feed at a CAGR of 14% and cattle feed at a CAGR of 10% by FY20

- Crop Protection:

- In crop protection business, company manufactures a wide range of products that cater to the entire crop lifecycle including plant growth regulators, organic manures, generic agrochemicals and specialized herbicides.

- In October 2015, Godrej Agrovet acquired a majority equity capital in Astec LifeSciences and currently owns 56.82 percent of the outstanding equity shares of Astec LifeSciences.

- Astec LifeSciences manufactures agrochemical active ingredients (technical), bulk and formulations as well as intermediate products and sells its products in India as well as exports them to approximately 24 countries, including the United States and countries across Europe, West Asia, South East Asia and Latin America. Astec LifeSciences also undertakes contract development and manufacturing services for other agro chemical companies. Astec LifeSciences sells all its products to institutional customers, while the Godrej Agrovet sells its products primarily to retail consumers

- The distribution network of Company’s crop protection business in India includes approximately 6000 distributors, as of June 30, 2017.

- Company’s R&D initiatives have increasingly focused on off patented chemistry synthesis and also plan to focus on increasing the market share of our existing core products by developing products for additional crops and increasing our geographic presence

- Oil Palm:

- In oil palm business, Godrej Agrovet produces a range of products including crude palm oil, crude palm kernel oil and palm kernel cake.

- Company purchase fresh fruit bunches (FFB) from palm oil farmers and work closely with them by providing planting material, agricultural inputs and technical guidance.

- Company has entered into memoranda of understanding with nine state governments, which provides us with access to approximately 61,700 hectares under oil palm plantation, which is equivalent to approximately one-fifth of India’s area suitable for oil palm cultivation, as of March 31, 2017.

- It has set up five palm oil mills in India with an aggregate FFB processing capacity of 125 MT per hour and a palm kernel processing capacity of seven MT per hour, as of June 30, 2017.

- Company wants to grow its presence in certain regions, create additional revenue streams from oil palm, biomass and continue to focus on R&D to improve FFB yield. The Government of India regulates the oil palm business in India and they participate in the Oil Palm Development Programme (“OPDP”) for accessing the FFB produce from farmers in areas designated to them. They will opportunistically evaluate tenders issued under the OPDP and apply for additional areas to increase the area under oil palm cultivation that is accessible to them.

- They intend to diversify oil palm business and create additional revenue streams and lower operational costs, including through the use of oil palm biomass in our animal feed business, which they believe will reduce dependence on the prices of crude palm oil and crude palm kernel oil. They intend to grow their presence in certain districts of Andhra Pradesh and Tamil Nadu, both organically and inorganically, and increase the area under oil palm, which is accessible to them.

- Dairy business:

- In dairy business, which it operates through a Subsidiary, Cream line Dairy, it sells a majority of milk and milk based products under the ‘Jersey’ brand across the states of Telangana, Andhra Pradesh, Tamil Nadu, Karnataka and Maharashtra.

- As of June 30, 2017, it owned and operated nine milk processing units. For its dairy business, company’s supply chain network includes procurement from six states through a network of 120 chilling centers, as of June 30, 2017.

- As of June 30, 2017, Company’s dairy distribution network included approximately 4,000 milk distributors, approximately 3,000 milk product distributors and 50 retail parlours, as well as direct sales to institutional customers.

Company’s focus: - Increase market share by growing in southern states of India

- Increase value-added product portfolio

- Automate a majority of operations

- Increase procurement base

- Processing food:

- Apart from this, the manufactures and market processed poultry and vegetarian products through brands Real Good Chicken and Yummiez. After starting in 1994, in 2008, with an objective to grow its poultry and processed foods business, it entered into a joint venture with Tyson India Holding, a subsidiary of Tyson Foods Inc., U.S.A. The management believes that the joint venture with Tyson India Holding provides it with the technical and operational expertise to compete successfully in India.

Company’s Focus - Company intends to introduce new products and increase product reach. They sell poultry and processed foods products and have a diverse customer base comprising retail customers, QSRs, fine dining restaurants, food service companies and hotels. They intend to continue to provide variants of existing, and new, value-added poultry products.

- They believe that value-added products will continue to be one of the fastest growing and most profitable segments of the processed foods industry in India. They expect considerable growth in demand from QSRs and modern retail stores. They believe the QSR market has been growing rapidly and provides a market for processed and value-added ready-to-eat and ready-to-cook products. Modern retail stores, which include super markets and hyper markets, are expected to increase demand for hygienically processed food products.

Competitive strengths:

• Strong Presence with Widespread Supply and Distribution Network - Company has a pan- India presence with operations across 5 business verticals: Animal Feed, Crop Protection, Oil Palm, Dairy and Poultry and Processed Foods. Since several of its facilities are located near major consumption centres, it is able to ensure product freshness by reducing delivery time to customers and transportation costs. Its nationwide footprint allows it to leverage the competitive advantages of each location to enhance its competitiveness and reduce geographic and political risks.

- As of June 2017, it had ~4,000 distributors for the animal feed business and the products are produced at 35 facilities, of which 10 facilities are owned and 7 are operated with an aggregate production capacity of 2.36mn MT p.a. It has ~6000 distributors in crop protection business.

- In Oil Palm business, it has entered into MOU with 9 state govt. which provides an access to 61,700 hectares under oil palm plantation, i.e. 1/5 of India’s area suitable for oil palm cultivation as of FY17.

- In dairy business, its supply chain network includes procurement from 6 states through a network of 120 chilling centres, 4,000 milk distributors, ~3,000 milk product distributors and 50 retail parlors, as well as direct sales to institutional customers as of June 2017.

• Diversified Businesses with Synergies in Operations:

- Company has presence across 5 business verticals that have enabled it to grow its revenues over the last 5 years. A well-diversified business along with the geographic diversification provides a hedge against the risks associated with any particular industry segment or geography. This synergy provides the ability to drive growth, optimize capital efficiency and maintain competitive advantage. For example, the animal feed team frequently collaborates with dairy and poultry and processed foods businesses for sale of compound feed to the farmers. Further some of the biomass produced from the oil palm business is used as an animal feed ingredient, which provides additional source of revenue to the oil palm business as well as strengthens the cost competitiveness of the animal feed business.

• Strong R&D Capabilities:

- Company undertakes R&D in the existing products primarily with a focus to improve yields and process efficiencies.

- For example, its acquisition of ALS provided an access to strong R&D capabilities in the agrochemical active ingredients category, which it leveraged to introduce new fungicide products such as “Kemplar” and “Casper”. It developed layer concentrate for egg laying hens in crumb form which is an important input in automated feeding systems. For oil palm business, it has set up an R&D facility at Chintampalli, Andhra Pradesh, which is focused on improving FFB yields. It spent INR 3.22mn in Q1FY18, INR 18.25mn in FY17, INR 16.88mn in FY16 and INR 29.35mn in FY15 towards its research activities

Financials:

- Total revenue grew from 2771 cr in FY13 to 4983 cr in FY17

- PAT grew from 97 cr in FY13 to 274 cr (250 cr attributable to equity shareholders) in FY17.

- Net cash Generated from operating activities

FY 17 897 Crores

FY 16 168 Crores

FY 15 109 Crores

Income Statement (Consolidated)

RS Millions FY13 FY14 FY15 FY16 FY17 Q1FY18

Income from Operations 27,609 31,025 33,118 37,550 49,264 13,633

YoY (%) 12 7 21 59

EBIDTA 1,946 2,415 3,060 2,967 4,392 1,244

YoY (%) 24 27 23 82

EBIDTA (%) 7 8 9 8 9 9

PAT 967 1,566 2,101 2,611 2,744 743

Balance Sheet (Consolidated)

Rs Millions FY13 FY14 FY15 FY16 FY17 Q1FY18

Total Debt 4,755 6,203 6,845 12,814 6,604 7,155

Other Non-Current Liabilities 287 534 698 2,023 2,226 2,061

Current assets 5,800 7,787 8,569 14,679 14,224 17,143

Current liabilities 2,964 3,838 3,582 6,239 10,677 12,769

Cash Flows

Rs Millions FY13 FY14 FY15 FY16 FY17 Q1FY18

Cash Flow from Operations 445 2,099 1,088 1,683 8,973 168

Cash Flow from Investing -1,670 -1,908 -1,307 -4,278 -868 -664

Cash Flow from Financing 1,246 729 -790 2,784 -7,881 333

Per Share FY13 FY14 FY15 FY16 FY17 Q1FY18

EPS - Basic (rs) 5.23 8.46 11.35 14.1 14.82 4.01

Book value (rs) 22.35 28.02 34.59 42.31 54.54 57.94

Debt-equity (x) 1.15 1.2 1.07 1.64 0.65 0.67

ROCE (%) 39.42% 21.10% 21.84% 13.49% 22.44% 18.94%

RoE (%) 23.39% 30.18% 32.81% 33.34% 27.18% 27.70%

Investment Note:

GAL is one of the major company under the brand of Godrej (which is known for its quality and excellence), 75% owned by Godrej Industries. It is operating recently under 5 verticals namely Animal Feed, Crop Protection, Dairy business, Oil Palm and Processed Food.

Out of which, Animal Feed is the largest revenue contributor and Processed Food is the emerging one which can be the next growth driver for the company along with its JV Partner.

Some peculiar features for investing in this company are: -

- Bullish outlook on Agriculture Industry as India being an agrarian economy which will help grow this company.

- GST implementation is beneficial as large market of their business is unorganised and added to it is the brand of “Godrej”.

- Proven business model which has showed good growth in profit and revenue in previous years with healthy ROE. This gives confidence for its next leg of growth.

- Expected higher margins mainly on back of Animal Feed business and Processed Food business. As there is good demand for Indian Foods (like shrimp, frozen foods) outside India, good exports should bring higher margins in low double digits.

- Sustainability of revenue provided by crop protection, dairy business and oil palm business.

- Complimentary diversification – As all business verticals of GAL touches other verticals through some or other function which reduces their cost and also helps to manage company when one of verticals is going through tough times.

- IPO proceeds will be used to reduce debt and other internal purpose which will give both operating and financial leverage to company over a period of time.

- Low capacity utilisation – as utilisation is low till now, it gives headroom for higher growth with minimal capital.

- Currently we are buying a company with 5 well diversified businesses growing its Revenue at 16% CAGR over FY 13 – 17 and Operating profit growing at 23% and Net Profit at 30%. With 30% ROE and 20% ROCE, D/E at 0.65X (FY 17), valued at PE of 32x, P/S is 1.8X.

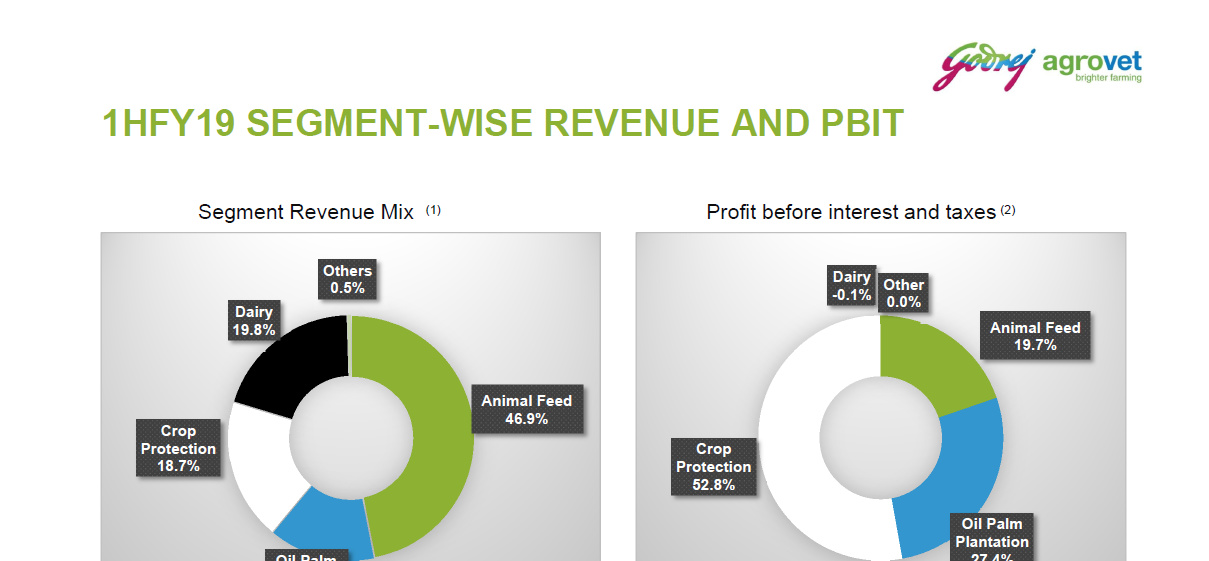

- Segmental Revenue:

Segmental Performance – Revenue Break Down (INR mn)

Business Vertical FY15 FY16 FY17 Q1FY18

Animal Feed 25,430 25,442 26,208 6,345

% of total 77.7 68.4 53.5 46.9

Crop Protection 3,352 4,959 7,647 2,781

% of total 10.2 13.3 15.6 20.6

Oil Palm 3,938 4,042 5,066 1,309

% of total 12 10.9 10.3 9.7

Dairy* 0 2,729 10,099 3,082

% of total 0 7.3 20.6 22.8

Risk:

- As company is dealing related to perishable products, quality is utmost important. Some variations or deterioration of quality in raw material for ex animal feed business which gives a major share can be a black swan event.

- As some part of business is seasonal in nature, it can be a matter of concern if that season doesn’t go as per expectation.

- We might be buying this company at a PE of 32 times while its growth guidance is 15% – 20% which looks overvalued. (This will always trade at a premium as it is backed by Godrej Group and product diversification )

- Geographical concentration - Company’s operations are concentrated in the state of Andhra Pradesh, any Black swan might be a big problem for them.

Disc: Not invested as of now.

{kind=link}