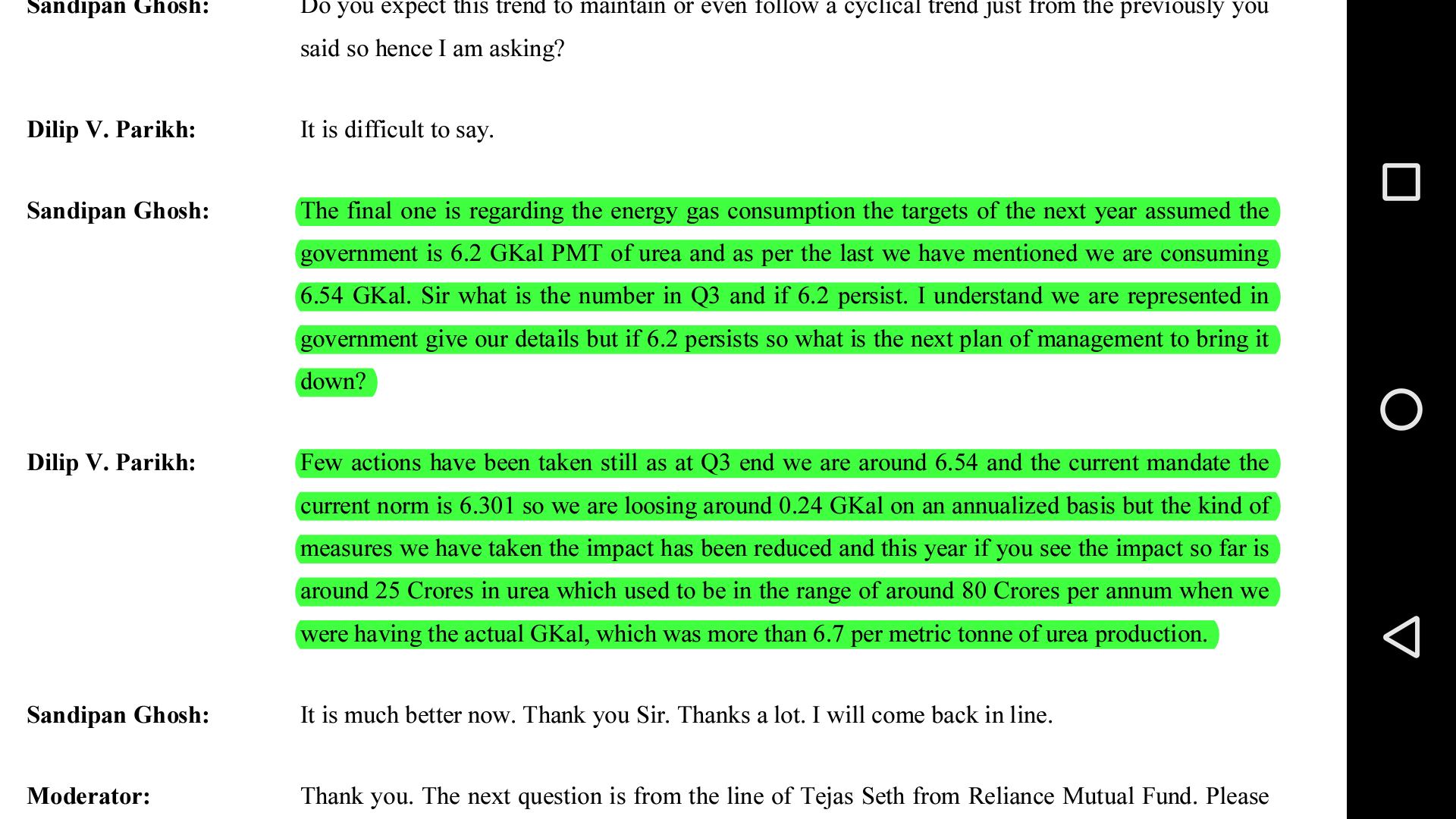

I have already asked the question in concall, that if this dispute still remains then what will happen, the management as usual said, we have brought down from 6.7 to 6.54 consumption , now all depends on the gov…

I can answer to your question, if this dispute continues, 2things will happen

1.we wont get 247cr contingency gain

2.we will continue to lose 10cr every quarter on the basis of this energy norm dispute…which btw we are still doing every quarter, so NO further downside from that…

ALSO NOTE , in 2009 the urea plant that was restructured can achieve 6.54 at the best using the best cpsu unit at disposal, further reduction cannot be done as told by management in q2 and q3 calls…

So i think that query is closed…

I have analysed tdi price crash and its effect in details previously… Also with good domestic capture volumes will not be hit if sadara comes into play…its better to analyse tdi effects after july , coz till july prices will be stable, reason explained in previous posts…

As per other chemicals, the chinese slowdown will keep the prices high as far as we know…rest even the management cant speculate… Still will attempt to do a analysis, thanks for the idea!!

No previous concalls have it… You can recheck and tell me if i missed it…

No one was paying attention to other income! Infact the other income was being dismissed to contain fertilizer subsidy! Thats why the grant got over looked… and deferred income in lia ilities with 3 figure also got overlooked coz all people was interested in borrowing section of liabilities…Yes, even Big analysts have tunnel vision!

I am not factoring in the neem play at all…

Next year if the gov changes, we can see all the neem stuff get cancelled due to some stupid reasons, so that prospect is bleak…

Recently i havr been a sufferer, in bls international, a huge punjab egov project whoch was getting very good footfall, started by the then bjp gov got suspended by now congress gov citing they are bankrupt and they cannot pay the operating concern bls international !!

So i am skeptical of what is to become of the neem project…

I hope i did throw some light, u really dont need ca guys in these matters, i think you are yourself good enough for it bro!