we need to be careful with gnfc now…

The harmonics are not showing a great short term trend…

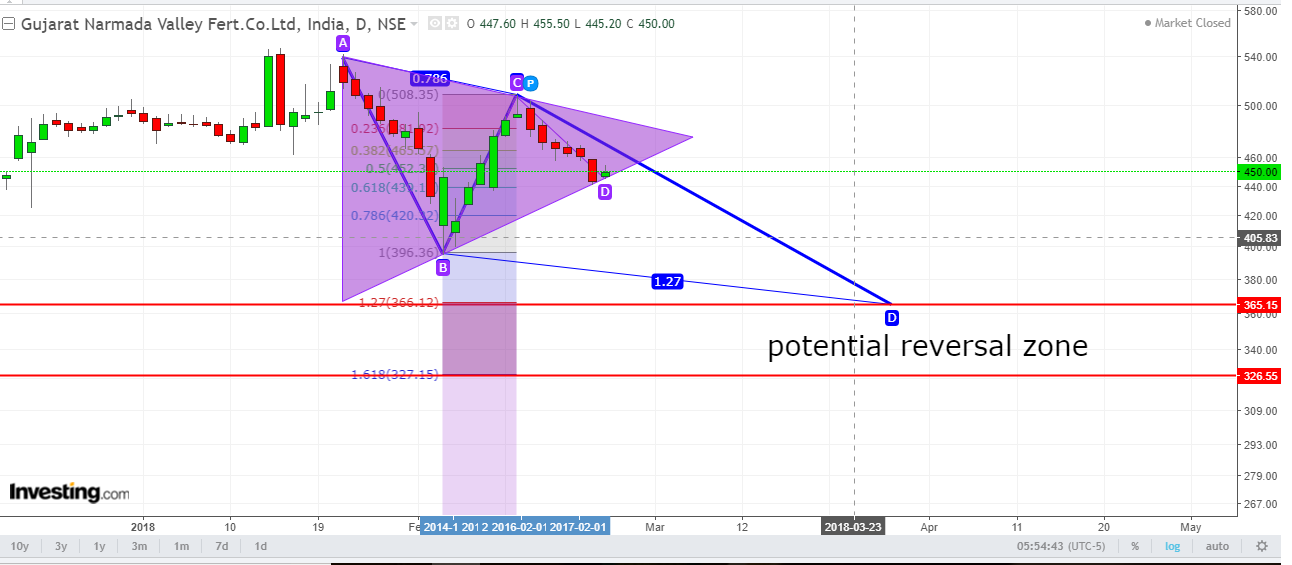

Although the symmetrical triangle is very near its apex and a good break out can totally invalidate this pattern…

Disclaimer… invested

we need to be careful with gnfc now…

The harmonics are not showing a great short term trend…

Although the symmetrical triangle is very near its apex and a good break out can totally invalidate this pattern…

Disclaimer… invested

Another interesting thing to watch

GNFC

Symmetrical triangle vs bearish ABCD rendezvous

If symmetrical triangle is broken out we can have a completely different scenario upwards upto the PRZ…

It can also be that it’s forming textbook bearish butterfly pattern. If you replace A by X, B by A, C by B, and D by C, then the AB leg retraced exactly at 0.786 of XA leg which is the criteria for butterfly pattern. In that case, XD will be 1.27 or even 1.618 of XA. Which means, first the price will cross the all-time high (also we have symmetrical triangle forming) before reversing from the potential reversal zone. Will be interesting to see if it develops into a perfect bearish butterfly pattern.

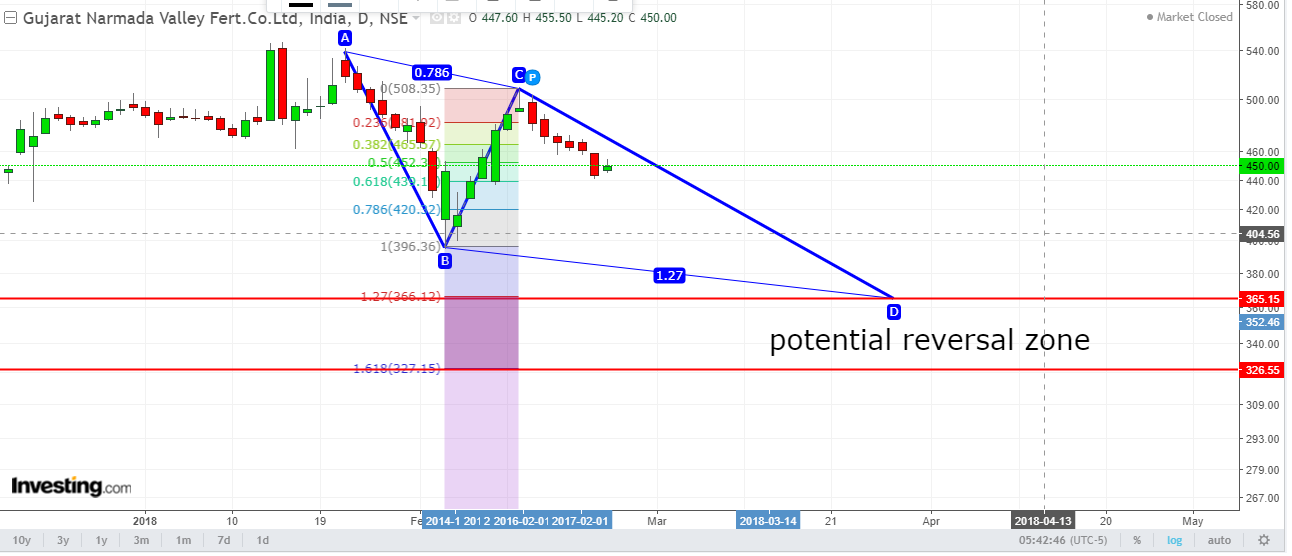

bro dont give more pain with bearish pattern!

And you ate right i dint look at the bearish butterfly hsppening, most likely the boader market is going to down down on monday on the back of oriental bank fraud news, if the market dont recover the only bullish ope of getting a symmetrical triangle will also vanish in air if this week the price degrades

Domestic TDI Price trend in CY18 (Rs/Kg).

299 10-Jan

325 15-Jan

335 01-Feb

325 22-Feb

315 28-Feb

310 01-Mar

Looks like it has peaked at 335/kg for the time being.

Regards,

Suhag

TDI is Rs. 300/Kg now.

Clearly the trend is down for almost 2 months now. @Capsule91 do you have any update on the international trend?

Regards,

Suhag

In march the highest prices of 4600usd per tonn is prevailing…

Still, i think it would not affect the topline…

Also note the premium placed over this base and the recent hike in premium is also been done in jan…

@suhagpatel, whrever u founf this info i am assuming it is the spot prices right? That means we get another 40rs premium on this base price…is thatbassessment correct?

This price is charged to Sheela form. I already shared that link twice in my earlier posts.

Even if we consider it as base price and add premium on top of that, the base prices is going down which will eventually reduce the overall price charged to customer. Obviously there is a topline impact. From 335/kg to 300/kg. There is more than 10% reduction in price.

GNFC raised prices on 15th Jan 2018 by 8%. Price before that was 299/kg. We are back to that level now.

If the international prices is going up or firm then why domestic trend is down. Any clues?

Regards,

Suhag

No i am concerned about Q4 in particular…

Although data from nov is only there in terms of domestic prices, i beleive the avedage was below/around 300 , so in comparison we have got a price hike from that levels only, so the topline wont be affected in terms of price…

The obvious worry is the volume and sales…

International prices have been hiked by basf, covestro and hanwah all, in february and march, and which has led to traders readjusting the market price and hence the present scene…

Broadly speaking, the prices will return to the pre hurricane harvey situation , that is half from now almost, as the supply flow starts…expected to be in equilibrium by the end of this year…

Essentially, the business cycle has peaked, and its time to see a downleg…

Note production of tdi in china is starting in yantai by the end of this year and east china has restarted production of caustic soda and ither chemicals like aniline and acetic acid…

Sheela form link has data from April’16 so you can very well compare Q4’17 with current prices which are higher. However, when we invest, we do not invest for a quarter or two. We invest for a longer duration. Even though stock is trading cheap now IMO, the market will not re-rate it upwards if TDI prices start falling below Rs. 300/Kg as TDI acconts for close to 60% of GNFC profit.

Jan-March 2017 price range was Rs. 240-275/Kg. We are getting closer now.

In these scenarios their expansion and capex plan will be crucial. CMD said they will do capex on Acetic acid and IT so we will have to see what value that brings it on table.

Regards,

Suhag

Hope the capex comes online before 2019 or along with ecophos…

But i have significant doubts how much a brownfield capex in a single chem segment will accure, although the management said in call that a good contribution …

Thats too speculative…

The pre hurricane harvey tdi prices were at equilibrium in 2500 to 3000 usd rangein i ternational market…

So apparently the hype is more in international spot price than domestic…

@suhagpatel

We are investing in a very cyclical business here…

And this business has maxed out on production and prices…

Be careful… Traditional investing principles dont hold for such a business…

With diversification gnfc will come out of the cyclical nature somewhat and stabilize margins cycle in future, hopefully, but as of now i am keeping a very sharp eye on the company…

U are correct market will not rerate if any dent happens on tdi front…

I dont fear a nonrerate…

I fear the peter lynch saying," low pe ratio can get lower", wrt cyclicals…

Please maintain caution…

Thanks for the updates…

Although old news but don’t think it was posted in forum.

India has imposed anti-dumping duties on toluene di-isocyanate (TDI) from China, Japan and Korea. The duty will run from 23 Jan to 2023. The duty was imposed after sole producer of TDI in India, Gujarat Narmada Valley Fertilizers and Chemicals (GNFC) approached DGAD.

SOURCE: http://www.european-rubber-journal.com/2018/03/07/erj-business-story-tracker/

THis happened too fast, this is a 1.6lakh tonnepa plant which is coming back onnline…

When it went kff line we saw a tempoemrary spike inthe market price of tdi… Now all that shoks absorbed and demand supply again back to equilibrium, now this extra supply may change the scene for worse…

CMD Spoke about Capex in Acetic acid and MDI recently. Rest of the things are known.

http://www.thenewsmanofindia.com/an-unprecedented-journey-of-gnfcs-turnaround-pride-of-india/

Last month he said Acetic acid and IT now he says MDI. They need to make it official soon to avoid confusion.

Regards,

Suhag

@suhagpatel

The Mdi expansion is a clear game changer, n is a monopolistic play … And what i knw is the gov of india is actually interested in domestic mdi production and in future there may be an antidumping morale if that starts…

Gnfc had plans of setting up a 50,000mtpa Mdi capacity since 2007 and when a financial stability has come now, this might materialize…

Also gnfc has signed a MoU with connel chemical china regarding this…

But therenis a problem, this mdi is a greenfield expansion, and we may not get the capex in the next 3 years… May be in germany n europe chem norms are more stringent than india, but as i have posted earlier , he covestro md said they are looking for only brownfield mdi capex right now as a greenfield capex to get license takes 7years…Any ways that is although a apple to orange reference…

Lets wait fr q4 concall for more clarity

Thats true. Currently its a pure TDI play no matter how hard CMD tries to convince market that GNFC should not be valued only based on TDI. Its their bread and butter.

Do you have any idea how these cashless townships they are setting up in many states help them revenue wise? One is farmers are doing casheless transactions in those township and that may reduce GNFC’s receivables cycle but what else? What is the overall model and does it help their IT business to get a pie?

There are some references in the below article even though the article is almost a year old now.

Regards,

Suhag

Fertilizer company doing good because of gov. approved subsidy on urea till 2020. How it will help GNFC in future.

wow, here is a bit of relief to the constricting cash flow possibility on the fertilizer sector…!