Aniline…

Finally i have got a solid recent evidence which solidifies suspicion of gnfc expanding into mdi production as there was MoU signed in this regard…

Have a look…

The dical phos plant is already done, the 40mw project with alfanar is also underway…

What do we guess for the next!!

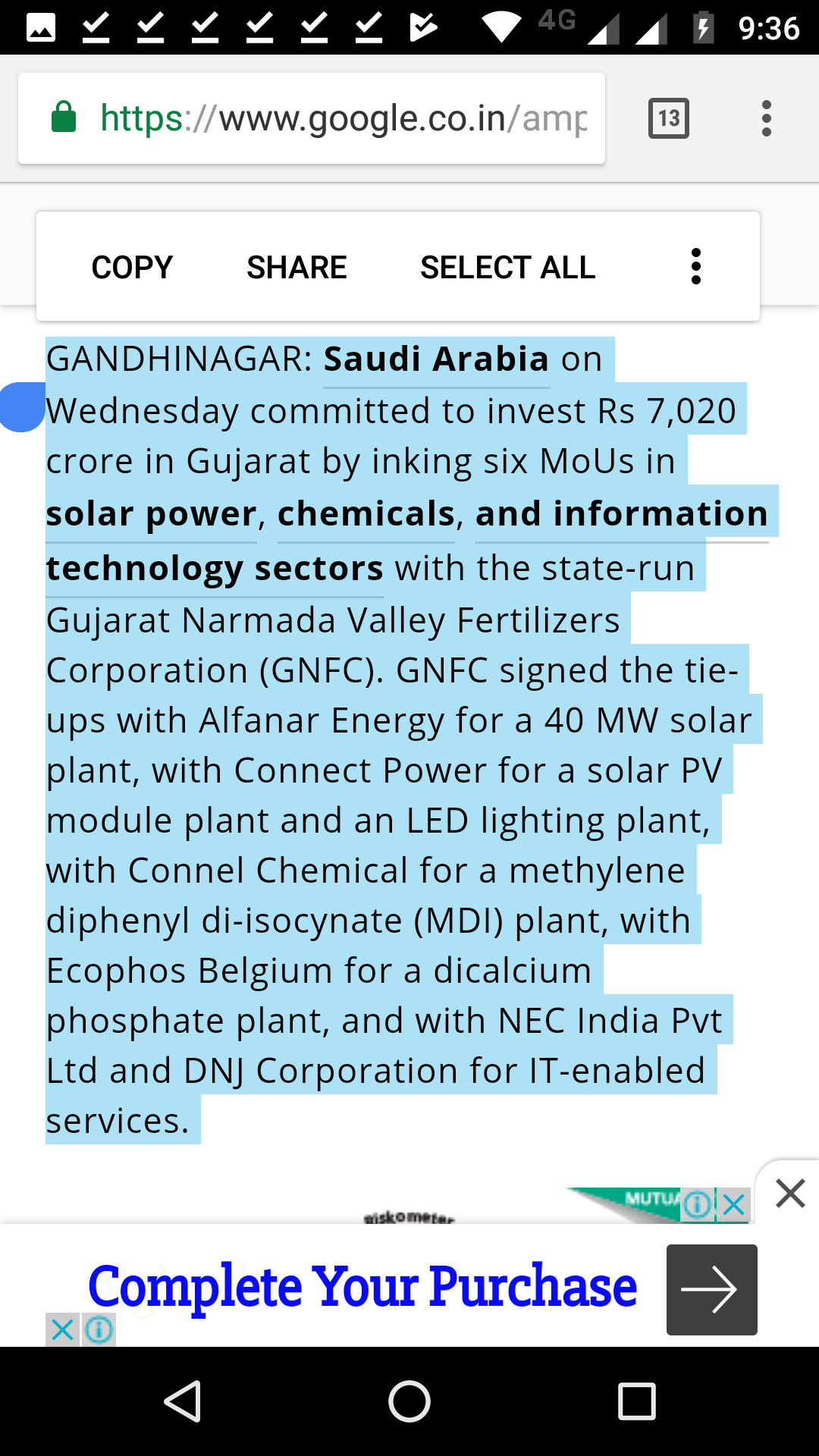

Also note this event happened during vibrant gujarat session, the same time they published the mdi project through vibrant gujarat publications…

Source…

Also, some other articles…

The next one is similar to the first, but it mentions the mdi investment is actually coming from china…

Also i will ask you to check the last 3 yrs annual reports,

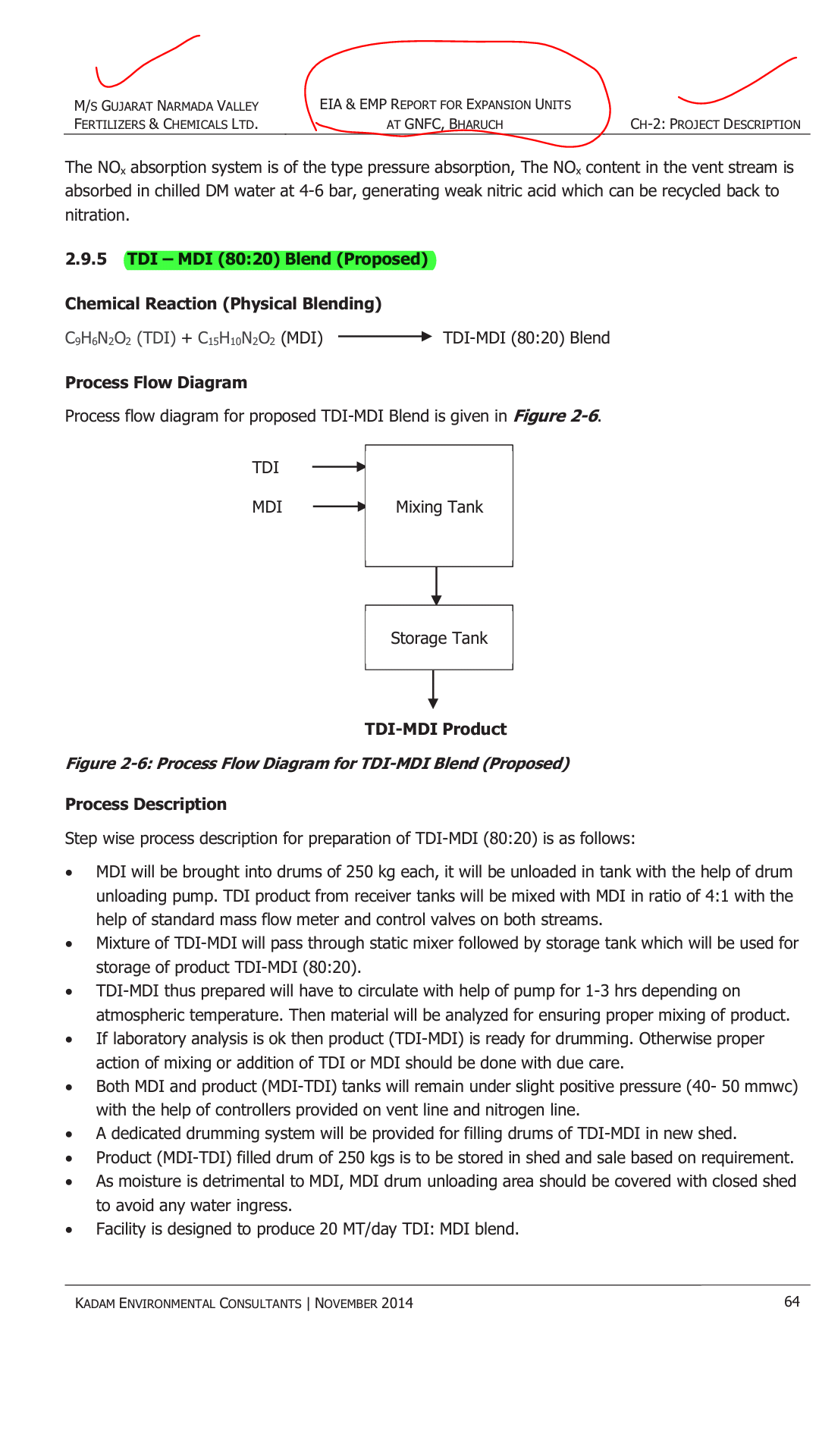

" . The Company is planning to market TDI-MDI blend. This will open a new avenue for business. Production of TM80 (TDI/MDI blend) on regular basis is envisaged for supply in automobile, insulation sectors. "

This quote has been repeated each year…

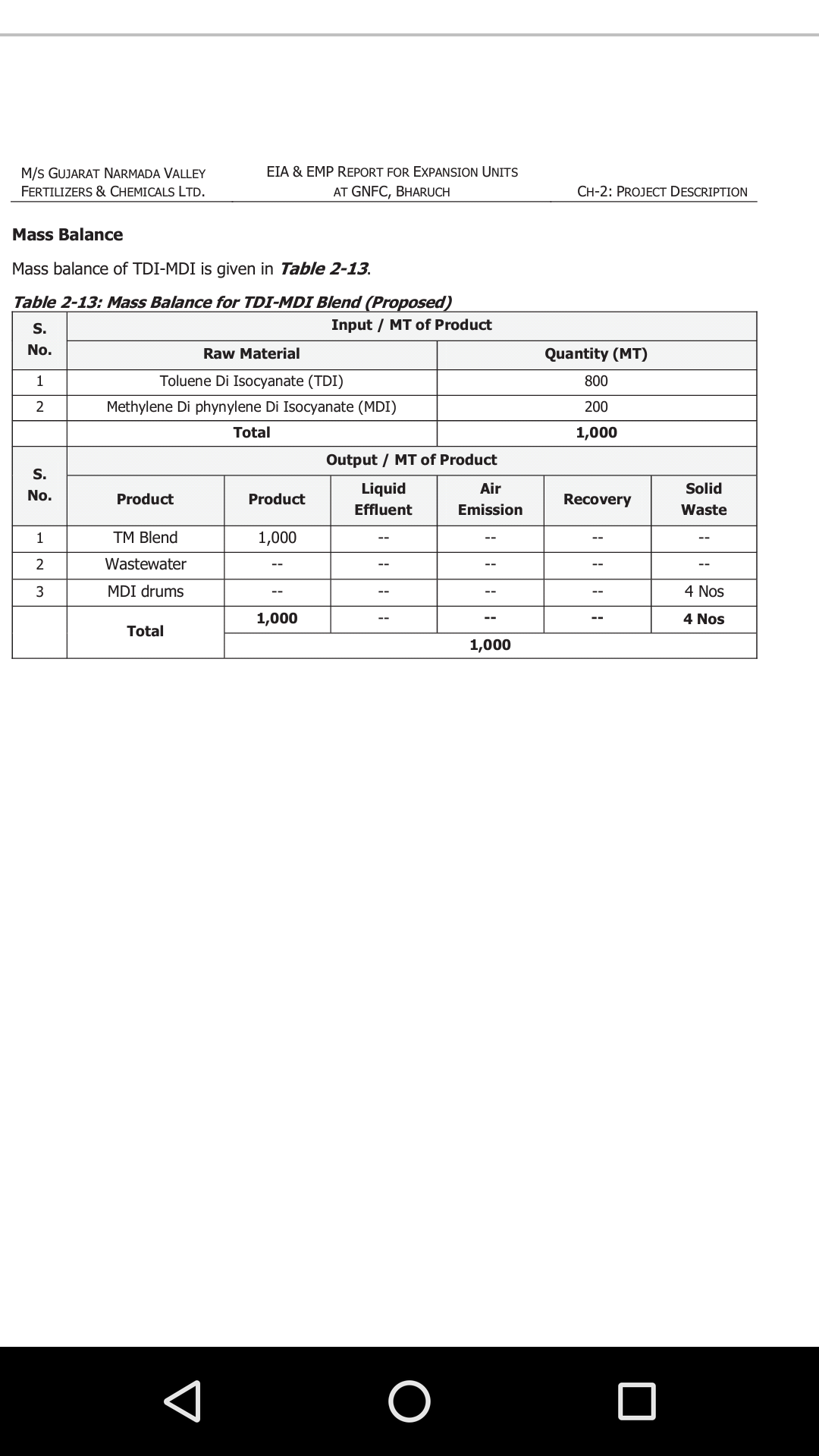

The mdi/tdi blend we are talking about is called TM80 , i found a 2014 gnfc plan layout proposition…

There is no TM80 producers in south east asia, and rarely produced(citation needed), none of the leaders manufactures in adequately(citation needed)

3 Likes

The ecophos capacity is 200,000 tonne per annum, and the price of the product is around 380usd per tonne…considering a minimum of 20percent ebita margine and a usd to rupee of 64, and given the fact gnfc has 15percent share of ecophos profits, amd given the expense saving on hcl… We will have roughly 65cr added to bottomline on an annualized basis… Thats a total of 4 rs eps annually…

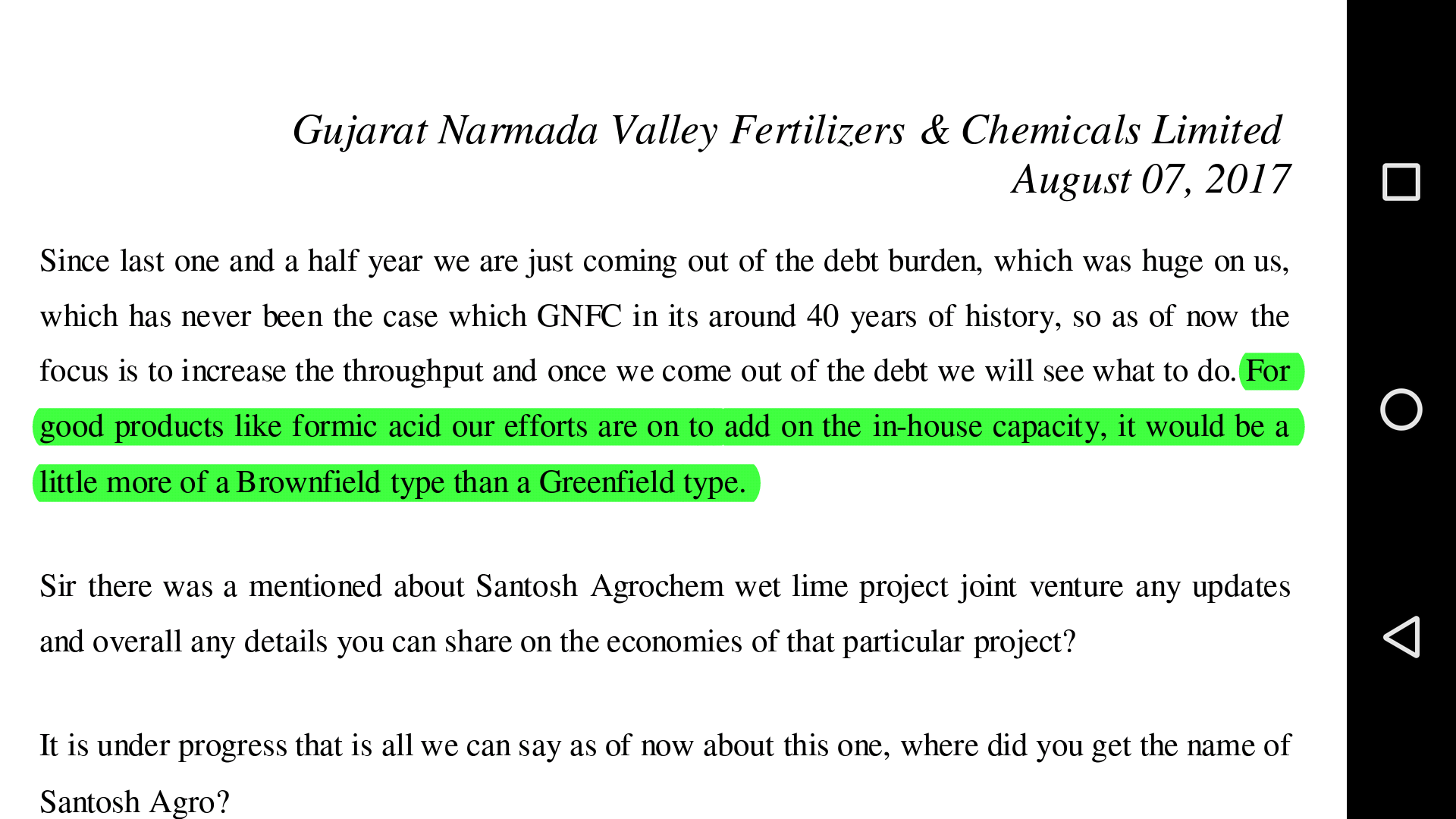

In Q1 concall of gnfc, the management gave a bit of hint regarding capex in formic acid which will be brownfieldtype

In q3 they menrioned they are considering vaious options, so formic acid can also be a part and as i previously mentioned…

The global Formic Acid market is expected to reach USD 878.7 million by 2023 at a CAGR of 4.94 % during the forecasted period…

But as of q3 concall we also heard the mangement say, formic acid prices are going down…

I sincerely wish either TM80 or mdi will be a part of this capex in this cycle itself…

Disc…invested

Thank you all for sharing these details. Love the passionate investors on this forum.

Just a quick thing: I may have overlooked but most of these are from Jan 2017 and from August 2017. trying to understand if that market has already factored this news and growth plans in the price of GNFC stock today…

Some more knowledgeable folks can respond to my query…

2 Likes

@nkabra

I am trying to answer with a different take on this…

I was wondering the same question, and what completely baffled me is the huge mutual fund exit that happened post q1 to q3…

I was listening to q1 and q2 concalls…

I found the management very immature in handling the market, all during this time all the analyst were pinned in attention to were

1.tdi volumes and realizations

2.whats the capex plan

3.why is the fertilizer segment not doing well as compared to peers on a relative basis

4.whats the plan with cash, any dividend plan

5.whats the outlook with dow sadara effect

6.ecophos

7.neem prospects and marketting strategies

8.capacity utilization of tdi2

In each and every of these vital points the management ducked big time…

Ecophos was a big disapointment, as 540cr of investment was done, but the output was just a 15pc share of profit…

About the constant tdi2 underutilization…The management only mentions often monotonously that its a complex process in the plant we have to take it slow, , just when the tdi prices are skyhigh, they want to take it slow…

Clearly the firms didnt get any visibility from gnfc management and neither do i still… In each of the concall nothing is said with which we can do a future tracking…

On top of it,stock prices shot up like anyting…

And the big guns left…

Coming to your specific question,market is too unreasonable in short term to understand BUT even at the current valuations, how can these effects be factored in… Infact all the potential of gnfc that it has, is not put with any clarity in the concall or in the press…

So actually the markets have really nothing to factor in…

On top of that, with tdi2 1 week production loss, whats the next quarter gonna be like, that has also become invisible and add the dragging fertilizer to the mix, we have nothing solid to factor in even next quarter…

Add to that its a commodity stock…

Plus a psu…

The sympathetic valuation that gnfc is trading in is not a chance but very poor handling by the management…

Recently i had a telephone conversation with bls international (a major holding of mine) cfo mr.ajay, which was by pure chance that i got to talk to him,…i am telling you, they are a class apart, they give visibility, timelines, assurances and knows to handle the investors well…

As much as i love to be invested in gnfc, i am really disapointed with them in the concalls…

I donot expect any rerating as long as they come clear with at least some of the queries, capex being one of them…

While i admire the intentions of the management to be strict with the disclosures, do it and then say it…but… Thats not how a good management attends the situation in market…

On top of that, the md was mentioned once that the stock prices were up, he went on record to say thats is not our main concern but a byproduct… This is not a wanted approach , though innocent , others generally keep shut or applauds the market upmovement…

Just to mention, tata power, which has one of my fav management, the recently ex md anil sardana specially… You can listen to their concalls, specially the q2, an analyst from icici direct asked about the ev charging stations they are putting up, allthough they basically laughed at the question in a cordial manner stating that its embryonic now to talk of this, but went on to give his take on the future how this ev charging stations will be set up and what are the different factors which will be determine how the model is going to be… Thats the kind of management the market like…

Disc… Invested

1 Like

Company updated Concall details.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/a9cc9c0c-9589-4be5-89f5-fb53d496df7a.pdf

Regards,

Suhag

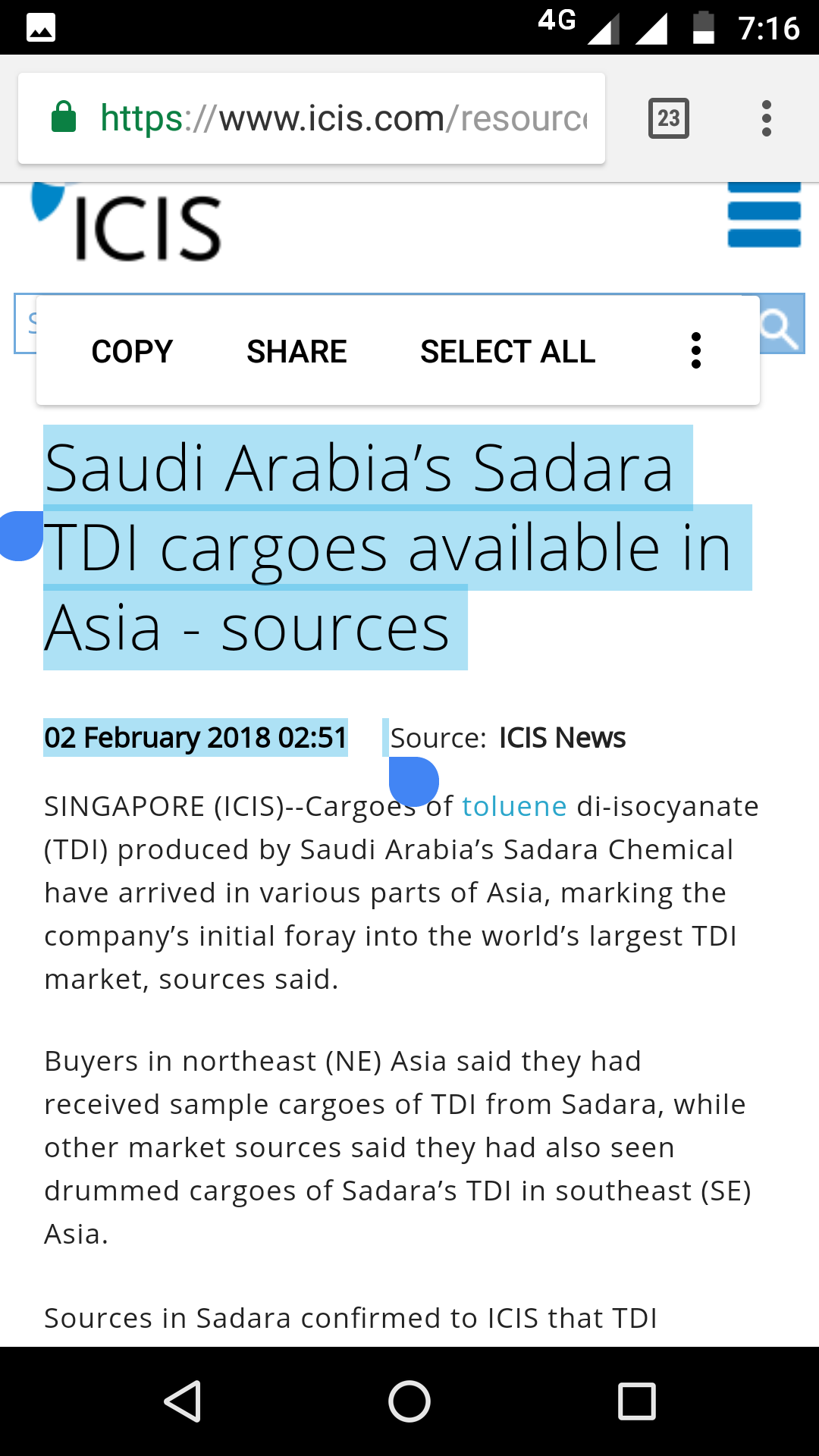

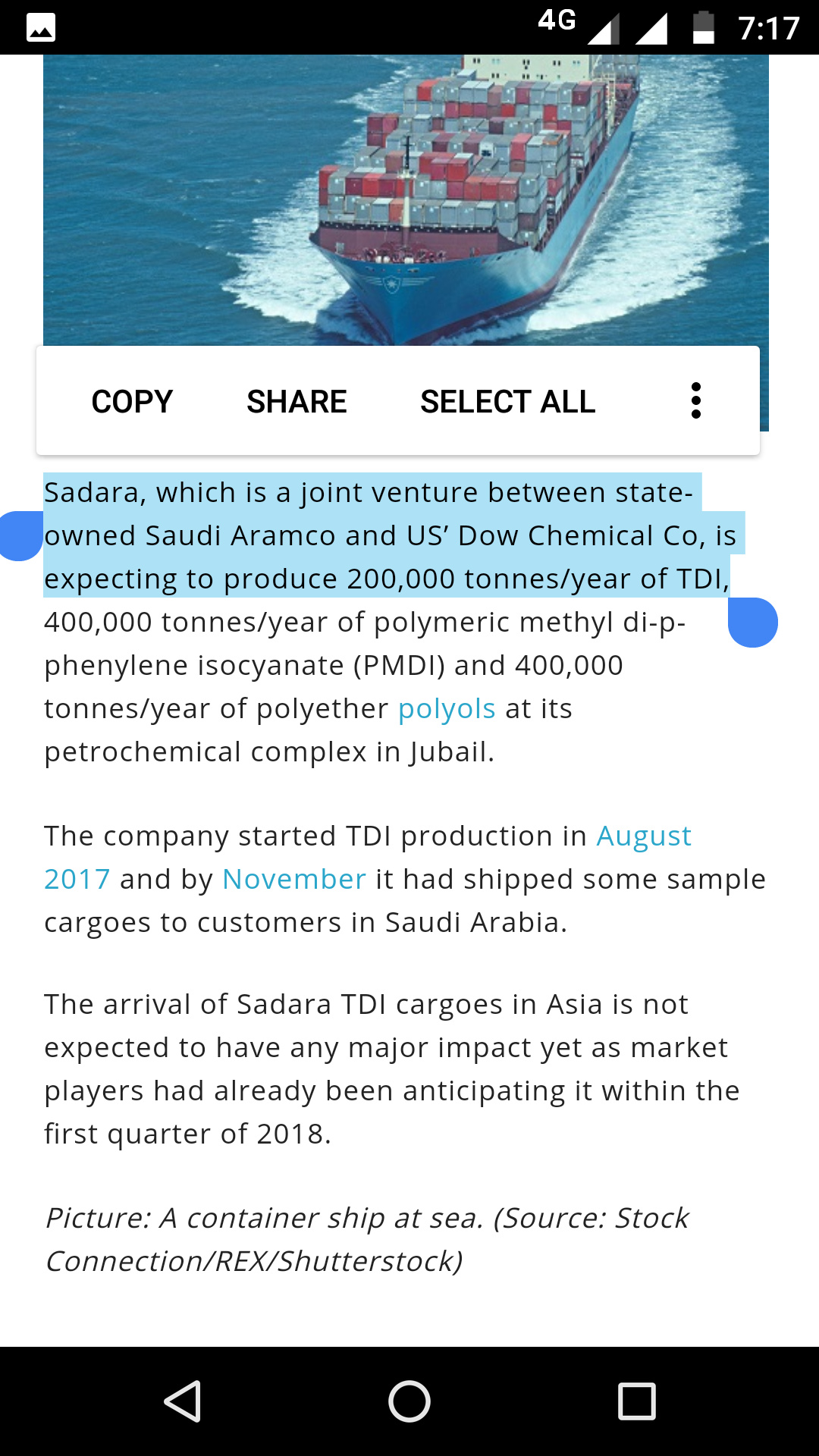

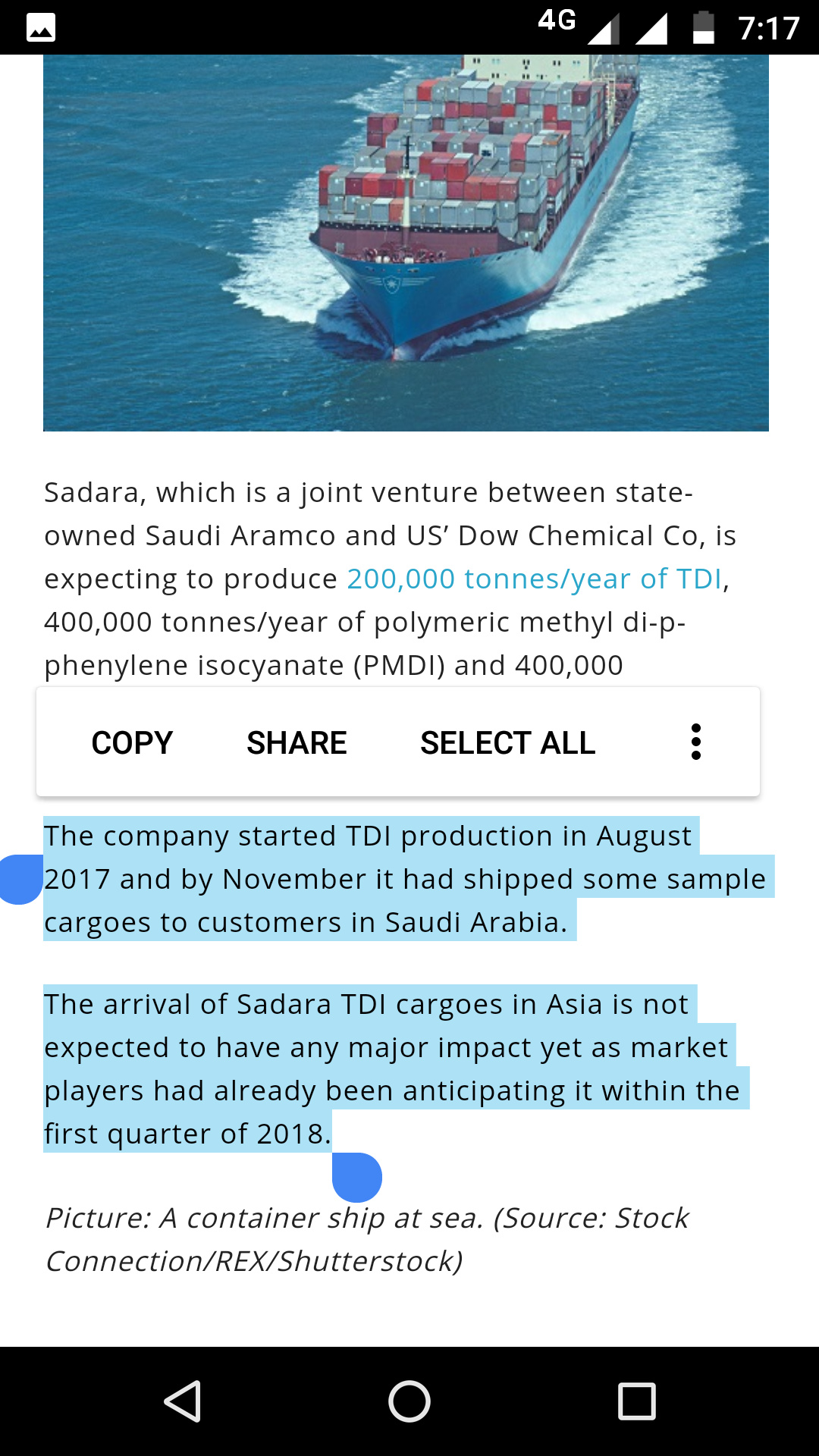

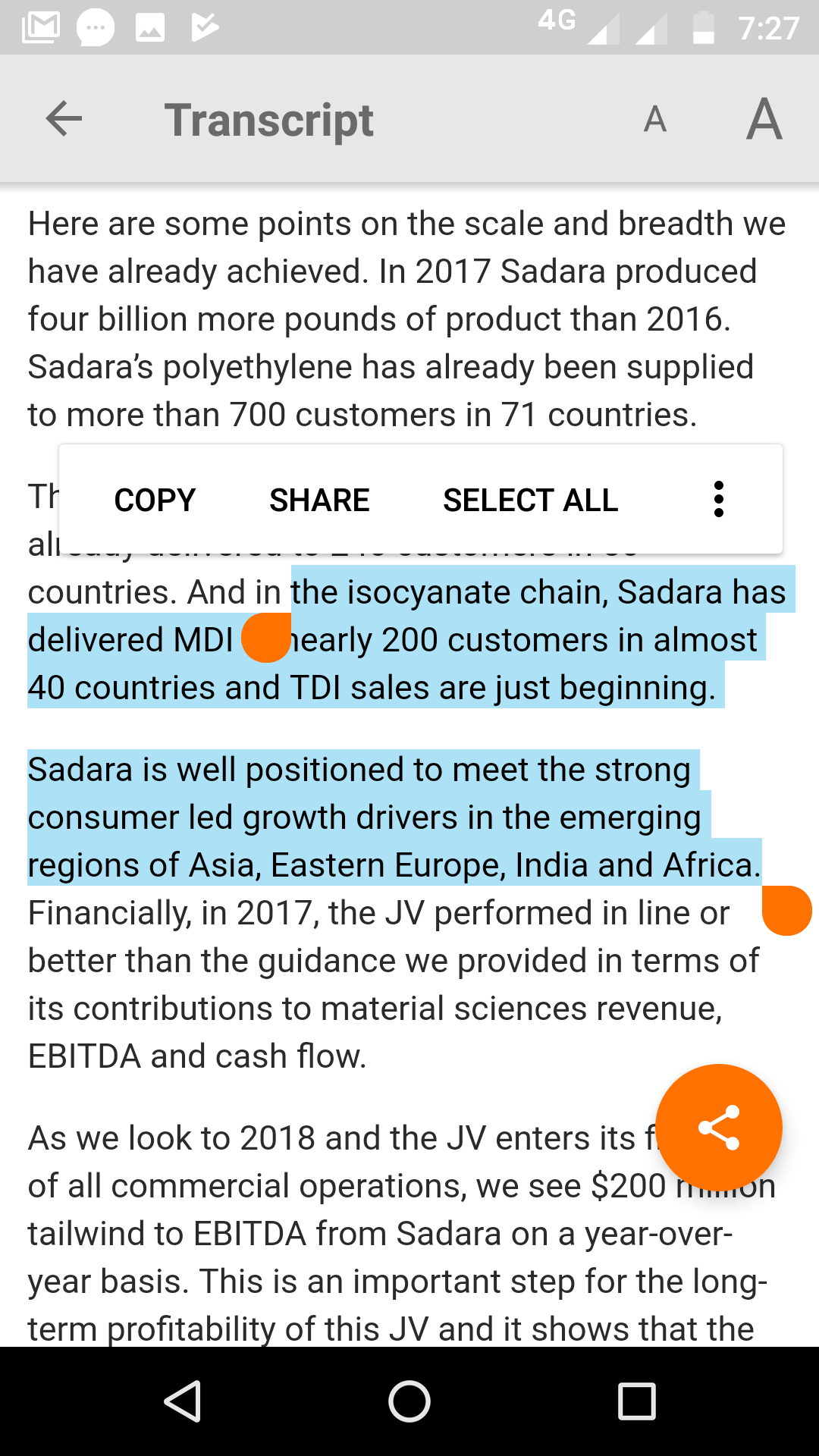

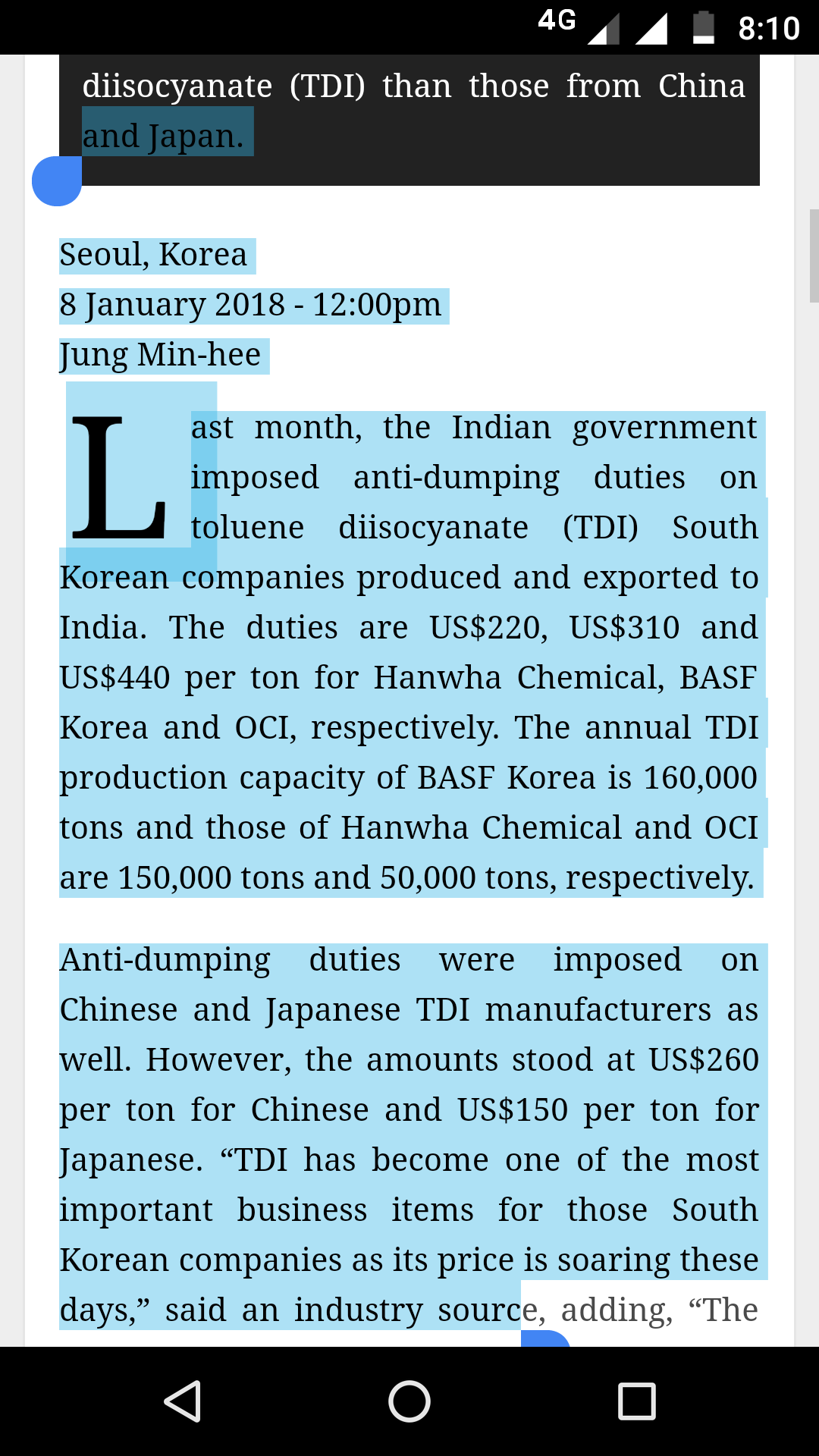

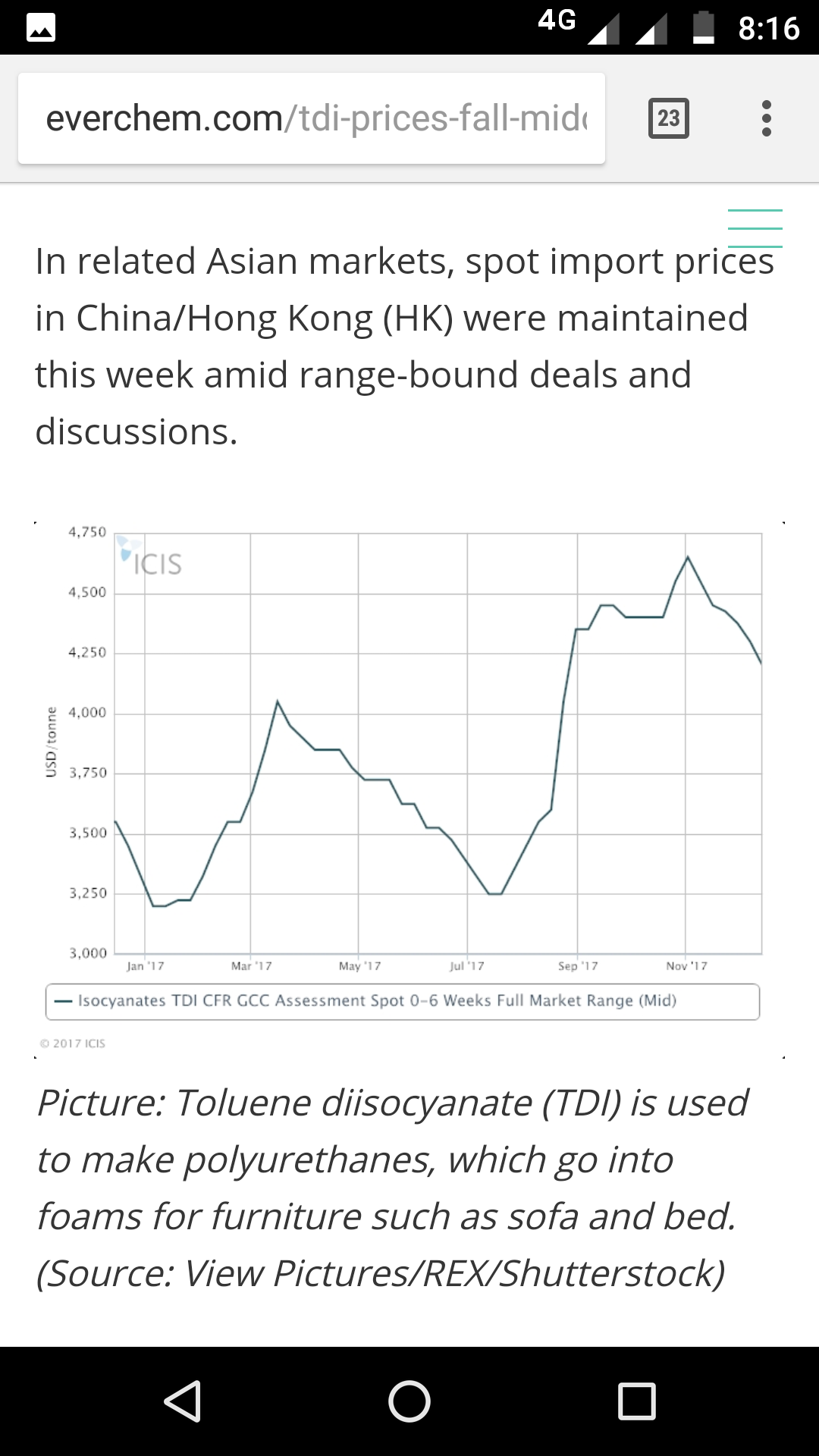

TDI UPDATES INTERNATIONAL…

1.Dow Sadara…

Following is relevant picks from the concall transcript of DOWdupoint q4 resultsnon feb1 2018…

Speaking of the dow sadara plant…

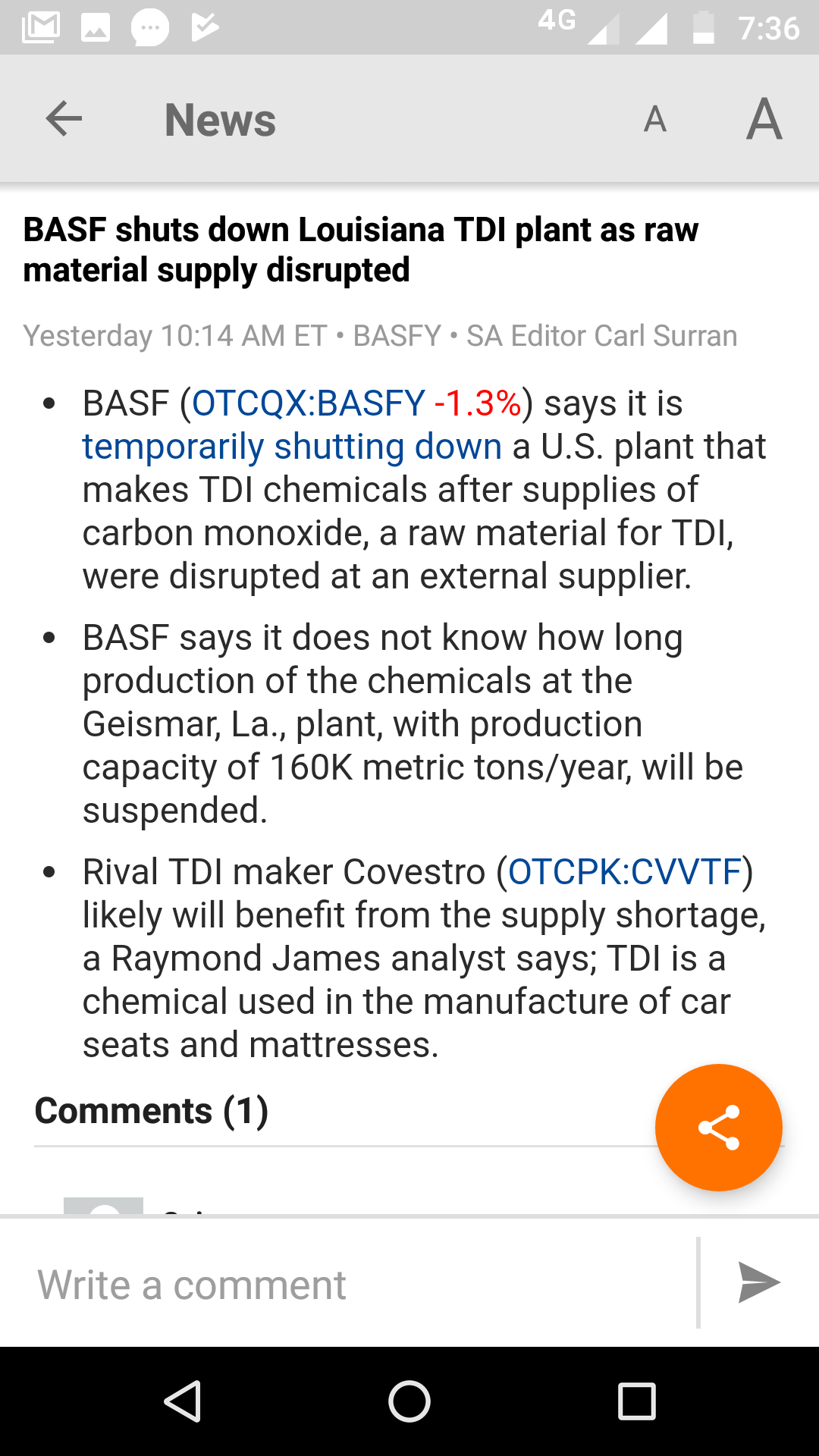

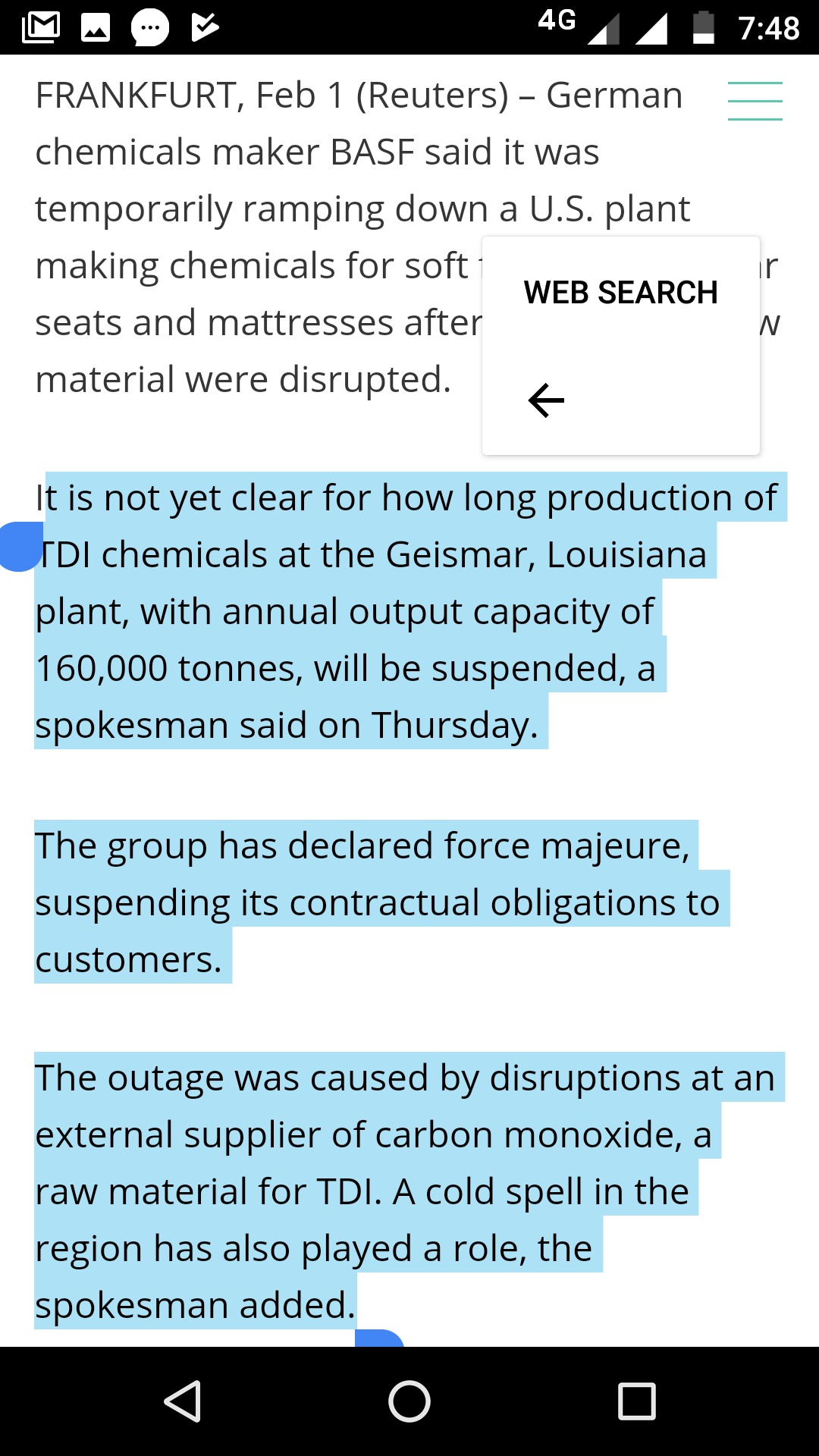

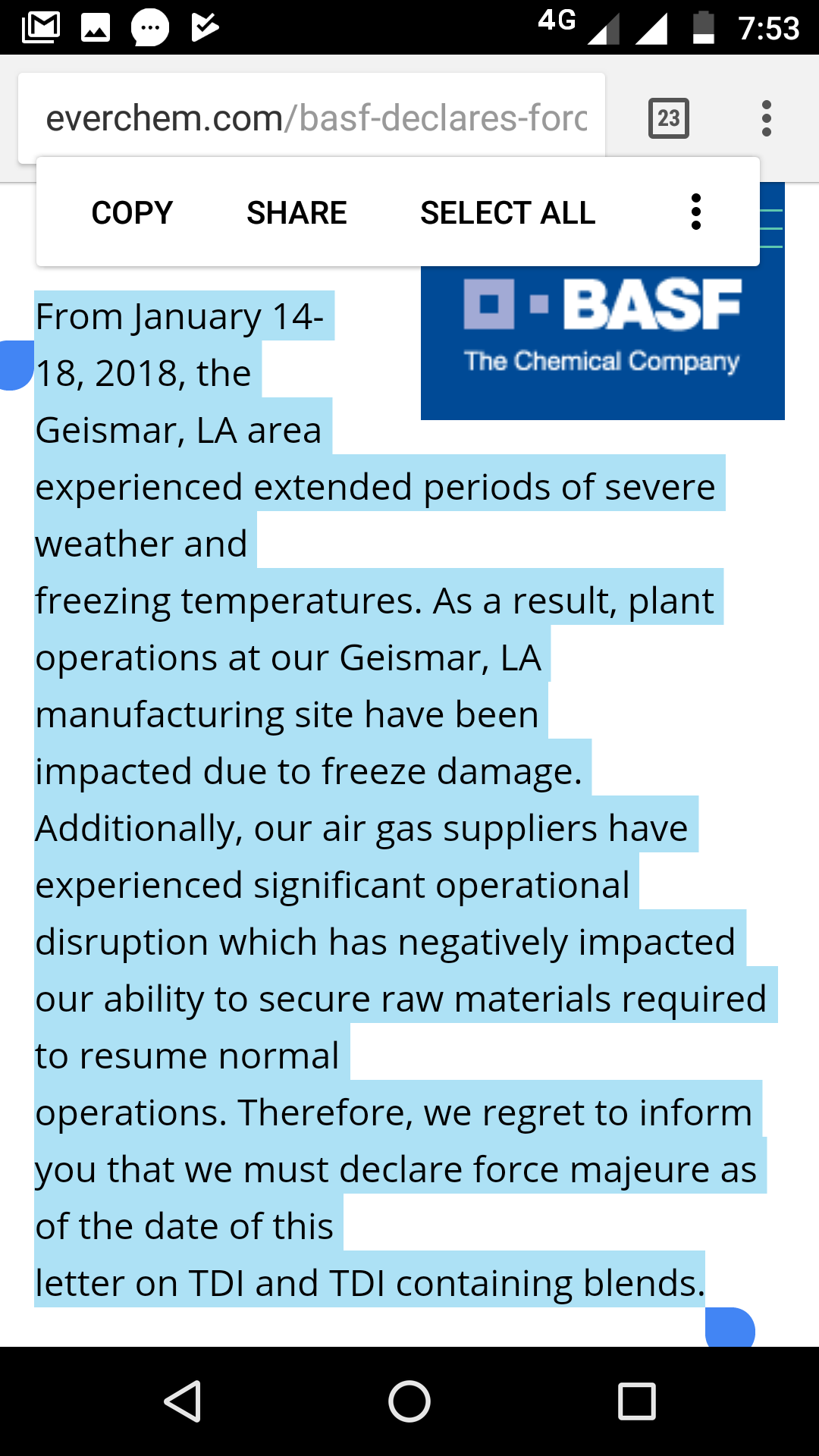

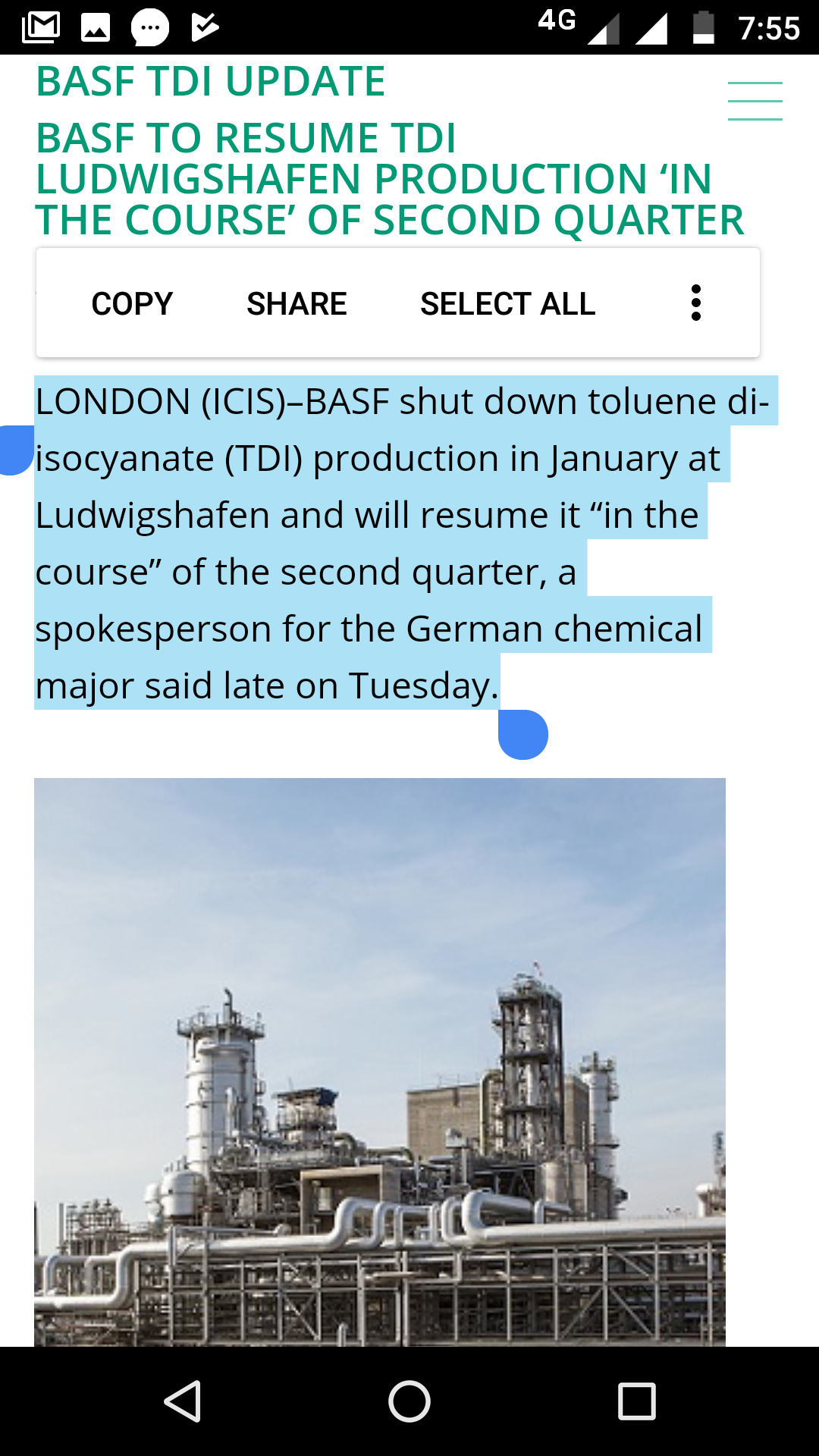

MORE TDI PLANTS SHUTS DOWN !!

AND THIS TIME BASF! Event time-yesterday!

More on this…

Now this part is interesting…

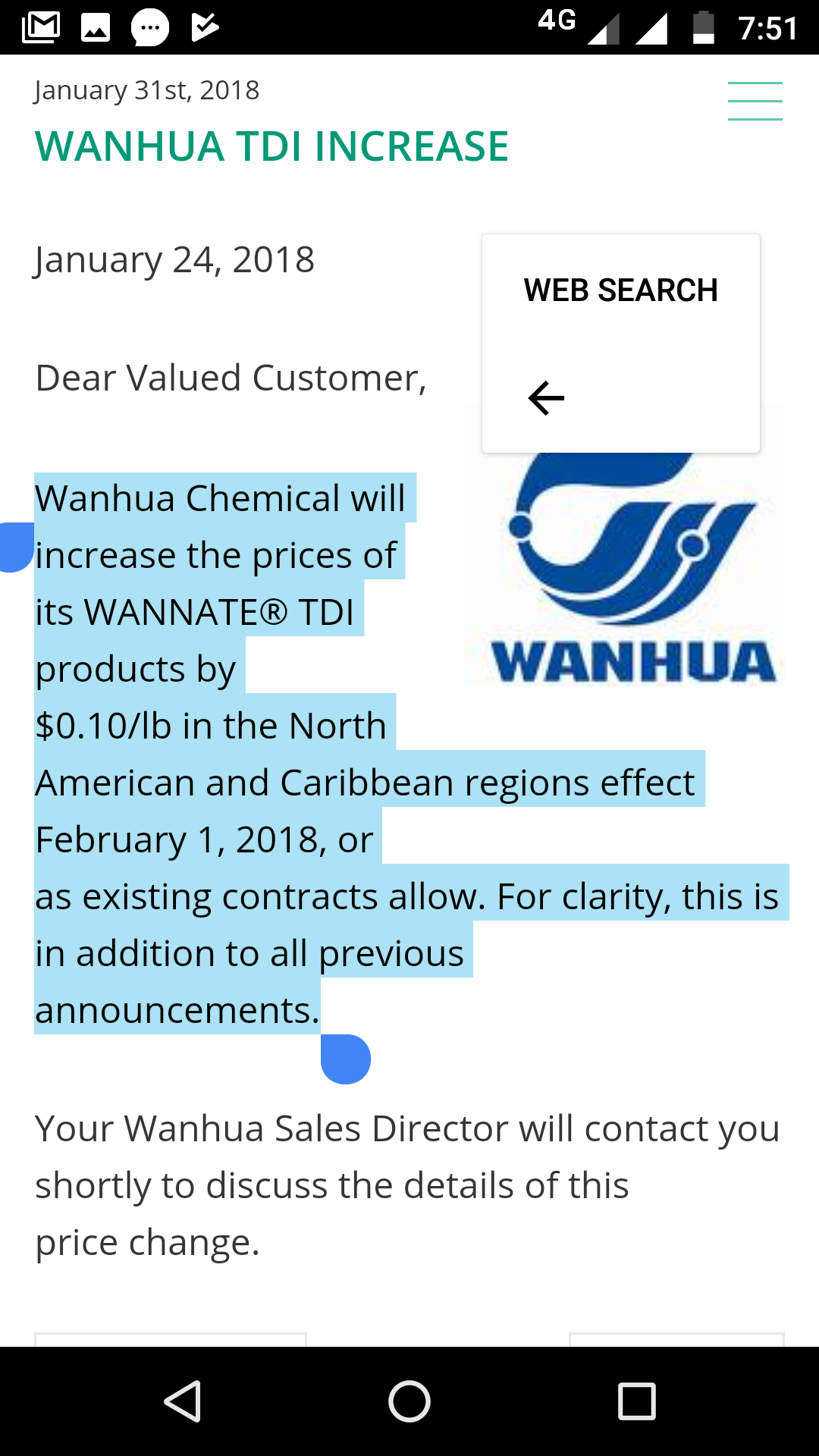

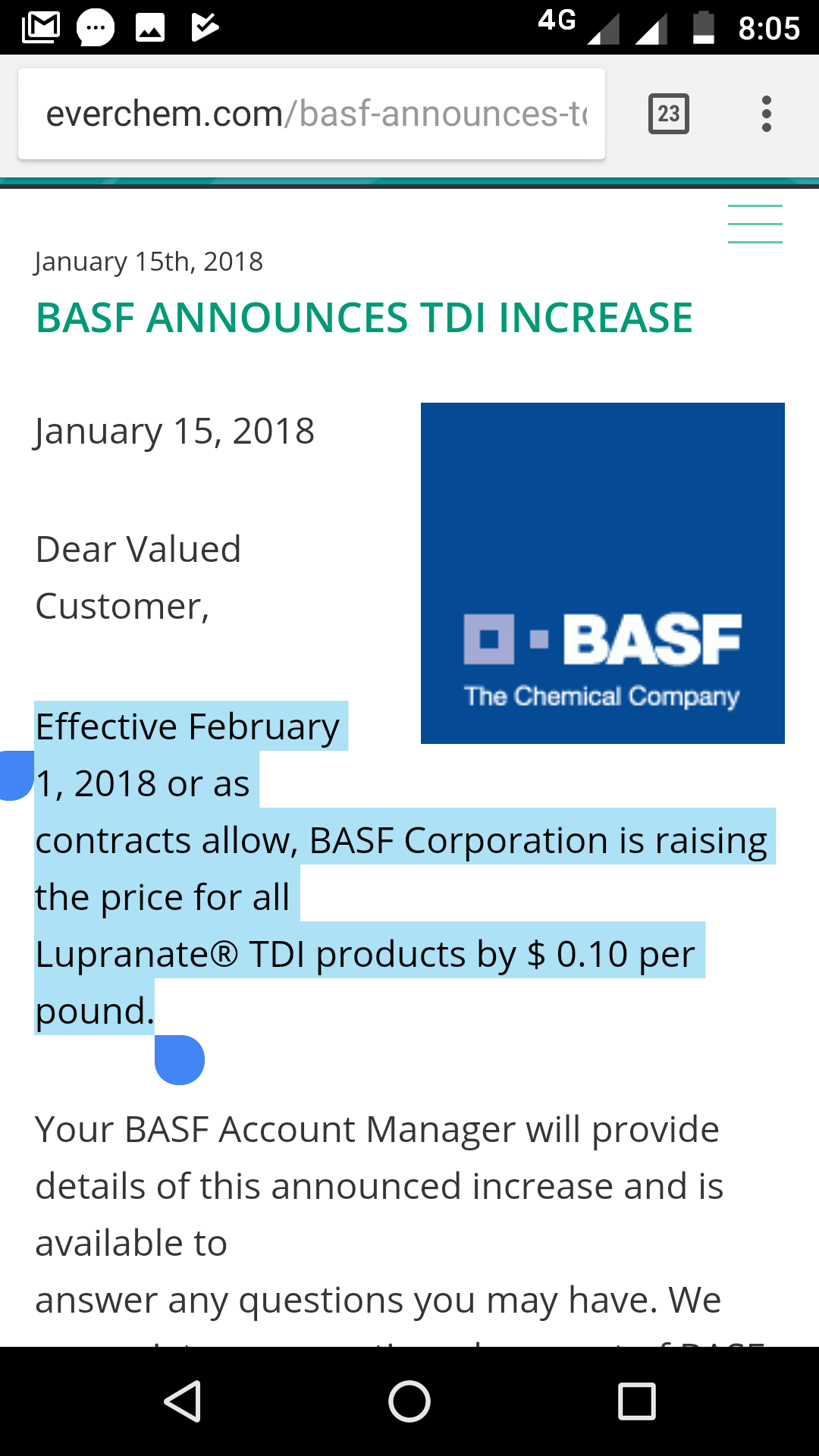

3.INTERESTINGLY MORE TDI PLANTS ACROSS THE WORLD ARE HIKING PRICES!

This one from WANHUA AND BASF

4.A SUSPECTED OPERATIONAL DIFFICULTIES IN ANOTHER GERMAN SUPPLIER Covestro!

5.just for info on numbers…

6.HERE IS A MIXED BAG REPLY TO THE QUESTION WE ARE CONSTANTLY ASKING!!

also its very recent report from 4th jan…

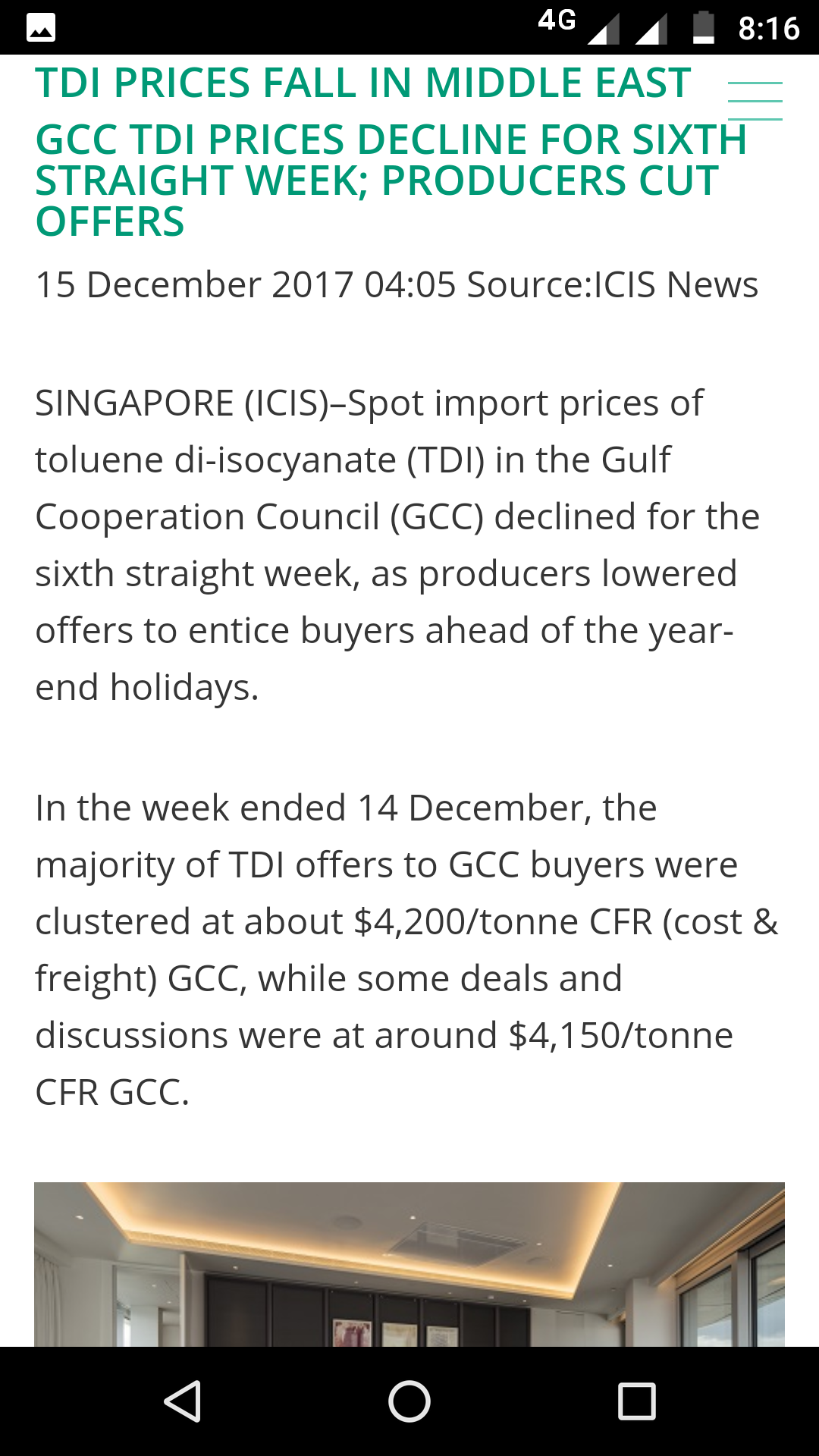

7.I THOUGHT I COULD ALSO INCLUDE SOME Q3 PRICES OF TDI, WELL LOOKS LIKE, GNFC PULL OFF MAGNIFICIENTLY AS THE TDI PRICES DID SOFTEN…

NOTE: the dow sadara upcoming plant can start a price disruption in the middle east by lowering margin…

Although as of now, all the major plants have increased prices in jan, hope dow sadara wont start a jio menace in our tdi cloud9 situation!

And concerns are there, i got a news report but cant find it now, where the consumers are even lower down their purchase volumes as they cannot afford tdi to make foams any more…Some greedy & sympathetic com came come to cater them and down we go…

8.ANOTHER TDI EXPANSION IN HUNGARY…

Construction of the new unit has begun at the plant. Start-up is expected in Q3 2018.{Q3 MEANS OUR Q1}

T65 and T100 grades are largely used in the polyurethane industry for flexible foam, coatings and adhesive production.

BorsodChem is part of Wanhua Group, which is the largest MDI producer in the world

9.A short aummary of the event in US which contributed to the tdi skyrise…

10.FINALLY, THERE WERE MANY PAID REPORTS WHICH I COULD NOT ACCESS, BUT FROM HEAD LINE OF 15 SUCH REPORTS, 1 THING IS CLEAR, TDI PRICES ARE STABLE ON SPOT BASIS, BUT NOW COMPANIES ARE CHARGING PREMIUMS, LIKE GNFC, EITHER FOR MARGINE OR AS A PASS THROUGH…

Inconclusion, the tdi prospects are still bright till july, we have to see what happens from Q2, dow sadara and basf are starting capacity around that time…

I cannot count the number of reports i saw regarding MDI production…GNFC should join the race… Even if it dosent enter mdi per se… TM80 is produced by very very few plants… That being in the gnfc wishlist, can become a game changer for us…!

Also, plant outages, under utilization, raw material shortage, gas leaks, fire has happened all over the world… So even if capacities come online, these issues will come up , so supply will always be bottlenecked…

Disc…invested

8 Likes

@ayushmit @hitesh2710 and other senior members inviting your views on this company. I am a novice and would like to learn from your viewpoints.

Regards

Aditya

Great Job…indepth analysis…

1 Like

Thanks @naveenbk…

To every members, gnfc has got export orders from additional 11 countries in this 9months compared to last year, can you put your inputs as to which are these 11 countries??

My rationale is with dow sadara coming online, some of these countries may source from sadara rather than gnfc if sadara is geographically located close to them and we may lose potential topline…

If we can sort down these countries, i plan to ask about the percentage of topline these countries are adding to our financials in q4 concall…

We can project the loss of topline due to sadara in the process…

Thank you…

@aditya, you can get all the queries about this company from the past posts in this board which is very very informative…

We can comfortably reach an eps of 65 in fy19, if current run rate in all the departments is maintained,now depends what valuation market is prepared to give us…at basic 10pe multiple, we can reach 650 or more…

1 Like

I know but there might be some reason the stock is still not re rating post q2 and q3 results. Also the company has strong cash flows which will become free cash flows by the end of this fiscal. Given that all factors are in favour and the stock is still not performing, I just wanted to get a view from the seniors as to what maybe some factors which are preventing the run up. Also I wanted to know whether according to seniors the stock is fully priced or not.

@adityaagarwal

I have already given my view on thia 1 day ago…

Read the forum thoroughly…

For now here is the quote of my prev post…

1 Like

I am sure most of the learned members already have factores this in, still i want to mention…

Going forward, if we are to maintain the present eps every quarter of 15, amounting to a total of 60 in a year, and incase the chemical market turns soft due to increased supply, we will fail to do so…

There is increasing concern about this in social forums and people are preferring to trade in position rather than investing…

Please note the following…

The present eps of 15 is optically reduced…

- A contingent liability provision has been made in the other expenses of 40cr in q3 and q2(38cr)…

If topline situation decreases , they will definitely continue with this, so we have 160cr annually out of the expense and added to bottomline…

2.the management mentions they want to maintain working capital of around 150cr plus 50 to 60cr capex debt if required, so total 200cr debt we will be financing… At 12 percent pa interest rate, we will be financing just 6cr per quarter…

So that is 67cr savings to be added to the bottomline…

3.Ecophos, i have already detailed the calculation parameters in a previous post, please refer, from there annually we will get 65cr to the bottomline…

So 1+2+3= 292cr to be added to bottom line going forward, that is much more than a quarter, and in eps terms Rs.18 !!!

More is there…

The present 247cr contingent gains due from the gov due to energy norm deficit, i dont expect gnfc to book it as an one time gain in other income, but o maintain a steady addition, as we can book this as and when required…

So 292cr+247cr=537cr

Eps=18+15=33rs

So we have a buffer to any disprution to chemical topline in the amount of 33rs annualized, and if the current eps guidance of 60rs continues , we can get 93rs as a annualized eps…

There is more…

#1… A 50rs per metric tonn of hike in subsidy of urea is proposed to the government in light of the increased operational cost by all thr major fertilizer company…

The full capacity of 636000 mta is used and this hike is approved, we get an bottomline of 3cr from this… This subsidy hike mayb in terms of dbt or capital subsidy…

#2… Capex is planned but we have no clue except the comment of good addition to topline by doing this capex… Now what is good addition, 10percent? 20?.. Lets take capex will enhance 15percent of chemical topline, and lets assume for conservative analysis this is going to be in one of the basic chemicals , most probably formic acid…

Considering 2016 q3, when tdi2 was closed, and when the capex comes online the basic chem prices go back to 2016 levels, we will be running at 20percent ebit margine compared to current 36percent,

So the quarterly contribution to bottomline from that capex will be 30cr and 120cr annually after tax , depriciation and amortization…

From these two points we get another 123cr of bottomline annually…

Finally, we can estimate a total buffer of 413cr (without contingemcy ) to 660cr { with contingency}…

Eps buffer of rs.26 to rs.40 in calender yr 2019…

This is in addition to the current runrate of 60,

Amounting to rs.86 to rs.100…a more than 100percent pure growth from ttm eps…

What valuations will gnfc get?

Let the market decide, try to discount this eps with current price, a pe multiple of 5!!!

I rest my case here…!!

Will try to update the board with new information…

Disclaimer… Invested

2 Likes

Expect the upcoming expansion plans to be one or more of the following segement…

In 2014 kadam consultants were hired to evaluate and explore and follow up recommendations for the following areas of expansion which are of interest to gnfc…

In addition to this expansion of the inhouse name plate capacity of FORMIC ACID and expansion/modification related to inhouse dahej tdi plant pertaining to increased operational efficiency without increase in nameplate capacity is mentioned in concalls…

Disclaimer-This is a document with full copy right to kadam consultants, and mentioned here with reference the original document which is available in the public domain and has been procured via internet source…

Most of the points discussed in Q3 concall have been covered by fellow boarders in detail. Few additions along with my take -

-

Rise in Toluene prices have not taken place vis a vis crude. Though, GNFC has taken a price hike recently. This might be in order to preserve current TDI spreads due to any future rise in toluene prices. Will be positive in near term till Toluene prices indeed rise.

-

Q3 TDI combined plant utilization was 101%. My take is that in FY19, overall TDI utilization will increase, but it would be hard to beat this 101% overall utilization attained in Q3. Though, this is hard to predict, as they have been operating TDI I plant at 120+%. I don’t know if that might be possible for TDI II as well. Even if they ramp up overall TDI production to 100% for the full year, would be amazing.

-

Sales loss in q4 due to plant closure will be 30cr (1000 ton). They said this closure will definitely affect scheduled delivery if not the total sales. My take - this means they do not have much TDI inventory to recuperate this loss in Q4 itself. So probably these sales are going to be postponed to next qtr maybe.

-

TDI revenue this year will be close to ~1300/1400cr. (crossed 1000 cr in 3 qtrs). Anyone got any idea about actual profits (PAT) from TDI alone?

-

All chemicals in general are pretty much bullish (both in terms of offtake and realizations). Cannot say how long this bullishness will persist.

-

538 cr fertilizer subsidies outstanding as of Dec 31. Forms part of other income.

-

Energy norm dispute outstanding 248 cr (outside books). Will just effect BS/Cash Flows, not p&l. Management was not sure when this will come through.

-

Reg TDI, they keep some premium to the landed price in India considering the antidumping duty and the immediate availability. As far as exports are concerned they do price it very competitively. Realization vary from country to country.

-

Capital subsidy that they are getting in fertilizer segment especially in case of urea where they have converted their plant from naphtha to natural gas was 108cr as of Dec 31 2017. Will be getting this by Oct 2018. This capital subsidy is probably not part of the overall fertilizer subsidy of 538cr. Also, this is not part of other income and is not recorded on books.

-

No plans as of now to increase nameplate capacity in TDI. Want to improve plant utilization by 10% in FY18-19. This year they have done close to 87%. So, they are targettign close to 95-100% next year.

-

Fuel and power prices are on the rise. Due to imported coal/rise in gas prices. Trying to get into long term contracts to reduce procurement prices.

-

TDI market is governed by supply and demand and that this plant is very corrosive and specially guarded technology which is hard to operate; so capacity utilization worldwide normally remains between 80-85%; if one looks at the scenario for world production/demand capacity, a gap exist even after Sadara production. So this gives the leverage in higher prices. (What is the utilization levels of Satara)?

My take -

- Fertilizer business is going to struggle. No respite in sight at least as of now due to higher fuel/energy costs, ANP issues, product mix improvement taking time, urea woes, etc. Moreover, working capital was said to be improving with DBT implementation, which as per management will take time. Instead, in the beginning, working capital requirements will increase a bit. Counter-intuitive!

- Neem business is immaterial as of now. Will remain immaterial for next 3-4 years (even if they ramp it up to 500 cr by 2020).

- IT is doing well; i am positive this vertical will keep doing well.

- Chemicals is obviously doing well and is predicted to do well in next few qtrs. But no one can comment on chem pricing and cycles. Their profits and cash flows depend a lot on this vertical. Any slowdown in realization or offtake might dent the profits. If crude stays where it is now or keeps rising, Toluene prices will increase. Sadara, well, it has just started and utilization ramp-up is yet to happen. It might effect global prices, which will hurt GNFC’s international sales as well. If international TDI prices take a hit due to additional capacity coming in, how will domestic prices get impacted despite insulation in terms of anti-dumping duty? TDI price rise actually happened in last few years due to supply issues. So, on the same logic, can’t we assume that if supply gets restored, prices will come down despite this being a tough plant to operate?

- Ecophos will only start contributing from March 2019, so still 4 -5 qtrs away. 50 odd cr contri to PAT.

- Capex - We will have to wait and see! Obviously will come at some point in the near future. They said in Q3 concall that it would be greenfield and will significantly improve topline, whenever it happens. MDI seems to be a right fit (GNFC - Turnaround Taking Hold).

The company had amazing cash flows vis a vis valuation in last 2 years; in FY18, cash flow situation will further improve obviously. Though, taking a long term call whilst chemical realizations and offtake being at very best (it can further go up, who knows) is tough. Needs a constant monitoring.

Disclaimer - Invested. Did positional trading couple of times in last 6 months.

2 Likes

Mridul… Take note of this…

subsidy is not a part of other income at all, or am i missimg something…?

And fertilizer subsidy figure of 538cr excludes 247cr due to energy norm dispute…

And the contingency gain of 247cr which they are considering in receivables has not been booked yet, but the true capital subsidy is already included in the fertilizer revenue, so that only goes to the balance sheet not the pl, so 247 if settled wil be added to fertilizer revenue first and then accounted as receivables in balance sheet, on receipt which will be free…

You cannot simply add 247cr in ur financials unless it is officially scantioned…

It revenue is consistently coming down…

I think there are three parts to this, which i have listed separately.

One, capital subsidy for fertilizer segment (naphtha to natural gas conversion), which is 108 cr as of now and will be booked in cash flows by Oct 2018. This is of course outside book.

Two, energy norm dispute which will not be part of the other income and will not be booked under P&L. Mgmt said - “We have taken it strongly with the government and this time also we have decided that we will go all over in that and take up with the Department of Fertilizer but these are government related matters and we cannot say for certain but we have insulated our balance sheet because of these issues. These are all sitting outside of books, which was 238 last quarter which is now 247 Crores as of Q3.”. So whenever this amount comes, it goes straight to cash flows. No P&L impact, no other income, no exceptional gains? or will come under exceptional gains?

Three, fertilizer subsidies (this is not capital subsidy…different than point one) as of Dec 31, and will form part of other income whenever it comes. Three excludes two is what they said in concall, so i listed it separately.

Correct me if i am wrong.

1 Like

@Mridul …

Agreed but i am not sure with the 247cr, as that will be a contingency gain… but on the otherside they mentioned this yr they incurred 25cr loss in terms of energy norms

, Are they saying all this losses are cumulatively amounting to 247crs over the prev yrs, coz they told previosuly they were consuming even 6.7gkal pmt urea whi h has cone down to 6.54…

If that is the case they they might just add the cash flow to the balance sheet … But contingency gains are included in pl statement as per best of my knowledge…

I have another question, specially from you, since you take a thorough negative stand on the other income …

Even if the fertilizer subsidy stops, and dbt is rolled out… As per dbt model they will add the subsidy as per pos sales in weekly basis and book receivables until discharged by the gov, which they are skeptical of , related to timely discharge of subsidy…

In that case although receivables will get increased, but optically we will still get the subsidy in other income booked, so no fall in other income will be seen…

Downside to this will be the working capital requirement, which they are saying , the cycle will get increased initially, origin of this is completely based on the timely subsidy payment which they are skeptical of…that incurs a bit of finance cost… But that will be post october, by then we will be debt free, and we dont hv to rely on receivables for anything… We already have enough internal accrualsa nd by then i will expect the expansion will be done…

So the only downside is fin cost mild increase due to working capital cycle getting prolonged and overlapped…

Other income will continue to be shown in pl as it is…

So no effe t on the total topline

So where is the problem you note…?

Also note, if they can convince the gov about the energy norms , then we may also stop losing 25cr a year on account of this in thr urea segment…that will be a win win situation…