Thank you Suhag for the details. That helps.

TDI 2 Plant issue is temporary as per my informed sources. Most probably will get sorted out in a week or so. Company certainly is on a path of making future revenue stream in like MDI, Methanol. Once it becomes debt free, we may hear big ticket capex from management or stock buy back announcement. I am expecting PAT of north of 200 cr in Q3 FY18. Since IT numbers are not part of standalone quarterly results, we can see spurt of around 60 cr in yearly numbers+decent numbers from FMCG vertical+Govt push in Methanol blending for Auto fuel+ interest saving of around 200 cr annually+ever highest global prices of TDI, Aniline, formic acid, weak Nitric acid and other chemicals (thanks to Anti Dumping Duty & China pollution crackdown) +Fertilizer DBT roll out in Gujarat from Feb 1 will make overall EPS more than 60 to 70 in coming 2 years. These all should rerate the stock sooner or later.

Informed sources? Which source is that?

Couple of people working in other chemical plants of company also said (on social media forums, can’t validate the authenticity of their claims) that issues are temporary. Stock also did not react negatively after a day of announcement of closure. However, unless and until your sources have direct knowledge of the matter better to wait for company announcement.

Requesting you to reveal the sources in such posts for the larger benefits of the forum.

Regards,

Suhag

1 Like

Strong set of results from GNFC.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/3faed840-6288-48cb-babf-b4ca37ce4e7a.pdf

As expected, chemicals are the key for company going forward.

PAT at 228 cr vs 67 cr

EBIDTA at 428 cr vs 203 cr

Margins 27% Vs 18%

Segment Breakup

Chemicals (62.7%) 1,085.93 Cr vs 667.31 Cr YoY

Fertilizers (-11.6%) 463.92 Cr vs 524.97 Cr YoY

Lets see what management guides on the closure of TDI Plant at Dahej.

Regards,

Suhag

1 Like

Hi Suhag, its just scuttlebutt with some of the people related to the company. However as you rightly said cant validate the authenticity of the info. Hope this clears your doubt.

Thanks!

GNFC restarts operations at TDI Plant in Dahej.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/553cac79-e544-4ac1-97d5-859eab98a630.pdf

Regards,

Suhag

2 Likes

I noticed the following points while listening to the MD on television

- Long term debt reduced from 2381 crore to 213 crore.

- Company aims to become debt free by 10th March 2018.

- TDI average utilisation at 87% and will increase to over 100%.

- Utilisation level of plants in other countries like Germany is quite low. So this price may sustain or increase in the medium term.

- With the direct benefit transfers, working capital cycle of the company will improve significantly.

- Management in previous concall had also stated that they have a habit of making provisions for contingent liabilities whenever company has a good quarter. I assume they might be doing the same this time also. (This point is my inference, MD did not speak on this)

- Domestic market share up from 49% to 63%. Company aims to achieve 75 %market share by March 2018.

Regards

Aditya

3 Likes

A couple of points on which i am finding value in the financial statements are…

- The provisions around 40cr which is being done in each quarter will not be continued from fy19 onwards… so there we can atleast expect it coming down to 25cr each quarter…

2.the contingent gain of 240cr pending to be book is growing with each quarter and going by the trend we can math it to 255cr by end of fy18 which most probably get booked in 2019fy…

- I am not at all worring about the subsidy payin after oct 2018 when the current pendings will get resolved… After that be it DBT or continuation of subsidy, from some where that is going to come, most likely in the last yr the gov will launch DBT and go, which will be a better scene for any fertilizer company, if even that doesnot happen, and subsidy gets into receivables cycle, it will not affect as the current subsidy is being used to pay off debt with that cash flow, next yr we will not beed that finance cost so we sould remain neutral on that aspect…

In this aspect as i am neutral with the subsidy inflow , going fowards in this sense i should not take the reduction in fin cost as an added advantage and that fin cost reduction will have a neutral aspect also…

4.A lot of hue and cry is happening as to what will happen if basf and sadara tdi plants come online, well as it is the company is targetting to capture 75percent of domeatic market by next quarter where antidumping duty is in action, so 75 percent of tHe revenue will continue to come in at least in a stable rate, rest 25 percent which is the export part, even if sees a reduction in topline and realization, will be minor and may be get negated by domestic demand and prices and with capex in other chemical segment coming online we can hold off the realization decrease if at all happens…

- The additional cherry is the ecophos project which will be generating atleast another 35cr to the bottomline…

6.Lets not forget the exponential growth possible in the fmcg space and also the it space…

In the segment revenue break up we saw the other part generating 21.7 percent growth yoy although the net profit from that has come down, but going forward we will see atleast

40cr more being added to the topline, what will happen to the margines heres is a question which time can answer for us only , which for now is contracting … For a good news, in q2 the distribution was in 3000 outlets which is now at 21000 outlets, a 600 percent jump, and i being in one of the biggest metro city didnt find gnfc products in big bazar, more or similar departmental stores as yet, so there is a lot to happen yet…

So going forward we can see, 60cr being added to the bottomline from point 1, 255cr plus from point 2, 35cr from point 5…

So we have a buffer of 350cr for next year in the bottom line…which is more than a quarter…

I have neutralized all the growth possible in the chemical sector and extracting figures from that…

Disc… Invested and planning to stay invested throughout the capex cycle and to the point of optimum utilization of the later…

3 Likes

Tdi, methanol, ethyl acetate and formic acid are the most produced chemicals by gnfc and most margine giving ones , that all we know at present from md saying so on cnbc awaz post q3… Acetic acid is not … so it can be expected that decrease in acetic acid price will not affect the topline and bottom line… Instead growing volumes of tdi , 10percent in q3 as per md in cnbc awaz post q3, will impart the margin deficit which may whatsoever occur due to drop in acetic acid prices…

I heard the TDI-II Dahej plant has started. There has been some channel which has reported it has not. Can anyone confirm or has any updates?

Anybody attended the GNFC Q3 concall?

Can someone please post the highlights? Was there any one-off provision in current qtr?. Any updates on capex and forward guidance in general?

@rahulshares… Yes i did, and following are the brief points…

- Aggregate tdi1 plus2 capacity utilization was 87% 9months ending and 101% quarter ending, on a breakup on 9m ending 113% tdi1 and 80% tdi2

2.production loss from shut down …1000mt ballpark

3.of the many reasons why fertilizer expense is up as already discussed by md on tv , the anp was discussed in a bit detail where the ammonia is produced from oil source and the later has increased costs now, 24% in q3 and 29% in 9m …

4.Now all the fertilizer companies are putting a case to the gov to increase the subsidy to urea in line of 50rs per metric ton on account of increased production cost…

5.although crude is climbing but on a 9m view the toluene prices have not yet gone up much, numbers not asked or answered, so on that front there is no correlation , rather benzene prices hv gone up in parallel… (my take) So that price hike in 2nd week of jan we saw is not pass through of raw mat costs only, it will affect the margines in q4 and onwards

6.as of jan, 5400mt of tdi export is pending

- 40cr of contingent loss provision has again been done in this q in the other expense, no view on q4

8.acetic acid prices have again started to climb, formic acid has softened, aniline and ethyl acetate is stable

9.all chem prices to remain so at least in q4, as per management view but they make a disclaimer chem prices are cannnot be predicted

10.it segment revenue is 38cr and neem 3.04cr in q3, it revenue has brought down the other segment revenue on q2 basis

11.management still ducks the expansion plan details, labelling it as premature, 3 participants had asked in different line of attempt…

The only thing which could be extracted was regarding methanol plant brownfield expansion…

The case here is gnfc has capacity to produce methanol from oil sources but not from coal, while the gov insists to produce it from coal, so they are in talk with the gov , if the gov decision prevails then they will expand and this is possible which the management stressed…

-

The contingent gain on account of energy norms is 247cr as on q end… And active and dilugent representation to the gov has been made to consider this… 6.301gkal pmt of urea is present norm and 6.54gkal is gnfc consumption, even after considering technical assistance, and when asked about how to bring it down the question was ducked as of now…

-

debt is 213cr q end and almost debt free by march

14.regarding capital subsidy a very imp thing is, its not booked in the other income, rather it is not at all booked in the pl statement but in the cash flow, so no effect of reduction of other income when the subsidy stops… 107cr of subsidy is left to be received

- Tdi plant aggregate capacity utilization to be increased to 90 percent, note not by expansion, but just by utilization…and no expansion plan is there at all

16.regarding the technicality of the tdi plant, they have installed automatic gas leak sensors which detect leaks in micro ppm levels and shuts the unit down, such leaks are very common in any chem plant, but last time the incident was taken seriously and was fully inspected in this oppertunity and maintainance was done, they assure that no major leaks leading to catasthrope as last time would repeat due to the advanced measures taken…

-

Capex will have a good increase in topline in coming times

-

Domestic price of tdi+ company premium charge is lesser than international price + anti dumping duty

-

International price is 4300$-4500$ in q3 and present

20.tdi domestic demand growth is 5 to 7% pa and 4% pa internationally

21.domestic tdi consumption =350000 mt pa + in specialized form 10000-12000mtpa

22.9m IT revenue is 123cr

- Tdi shall be marketted in auto sector in the form of a blend with MDI, and “commercial market is currently being explored”…

24.150,000 mt is annually produced hcl as a by product of tdi and lifting cost of 2500 to 3500rs per mt (depending on demand supply situation) will be saved, that amounts to 37.5cr to 52.5cr savings on expense plus the revenue from ecophos jv…

I think thats 90 percent of the transcript actually…

9 Likes

Hi everyone, fellow group member’s discretion and opinion is required on this post

As a disclaimer, the following content is just an hypothesis, no official confirmation has been received from gnfc office…

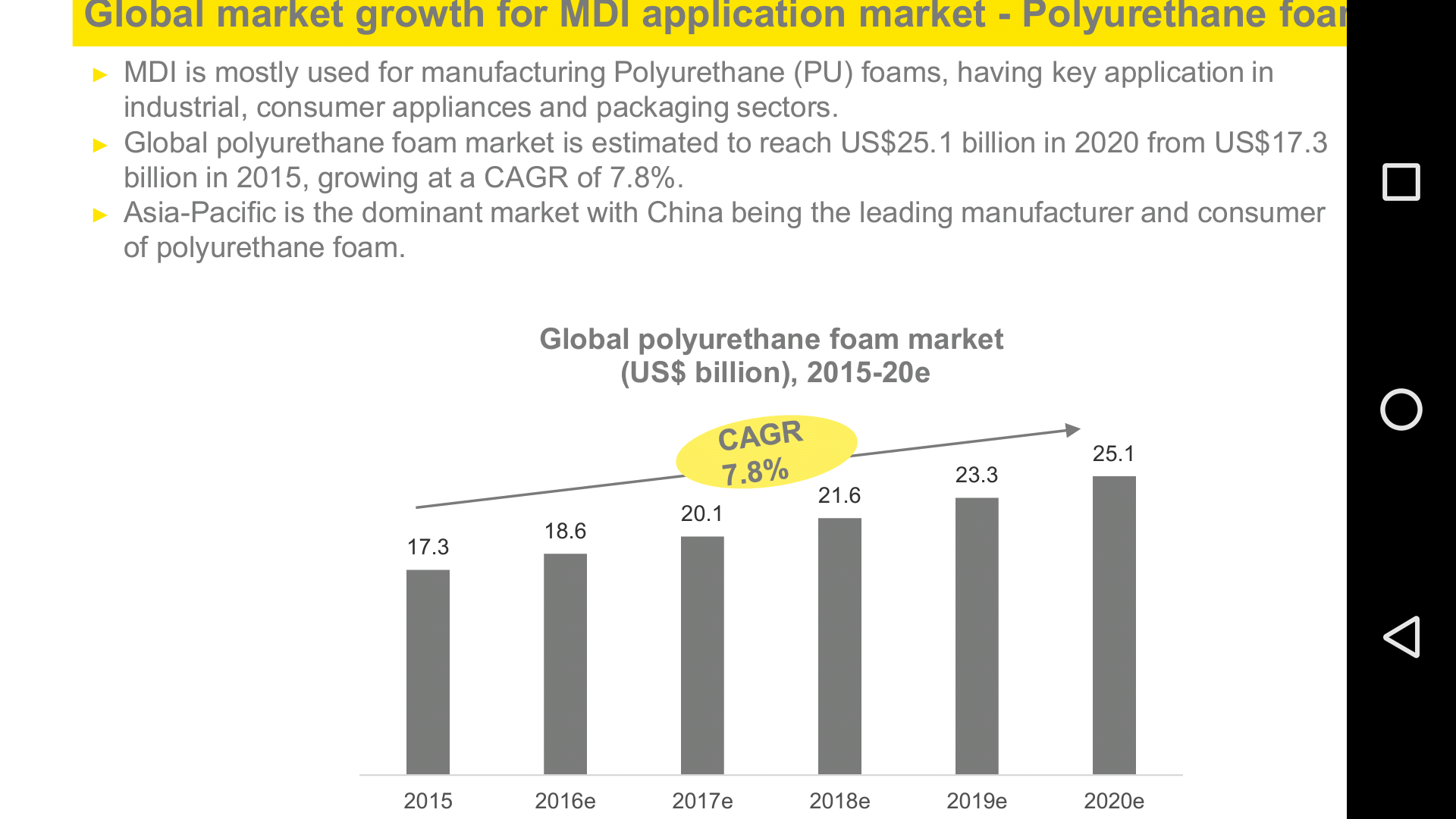

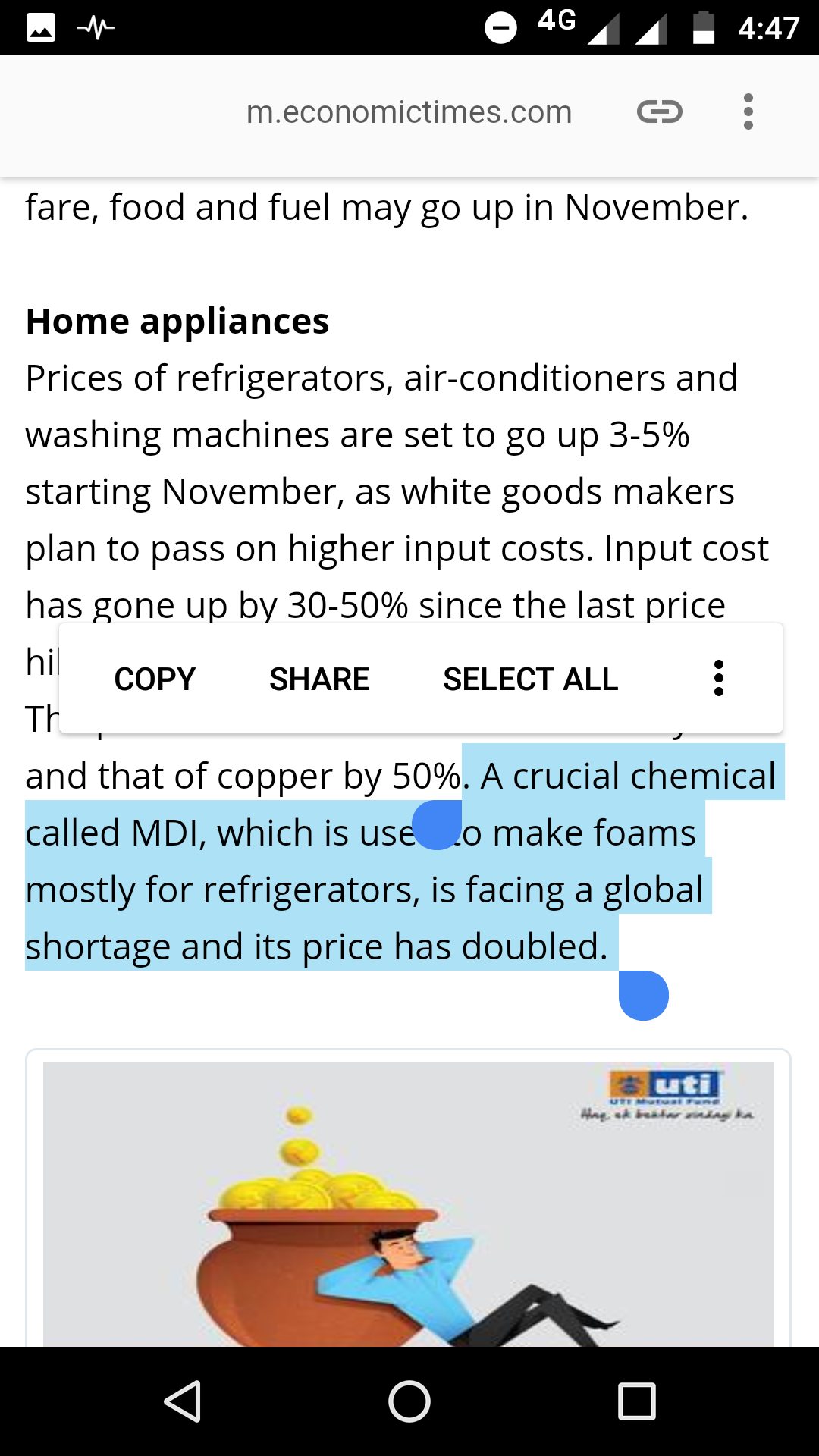

Methylene diphenyl diisocyanate, most often abbreviated as MDI, is an aromatic diisocyanate.

MDI is a chemical which is a significant value addition to gnfc and also of business interest.

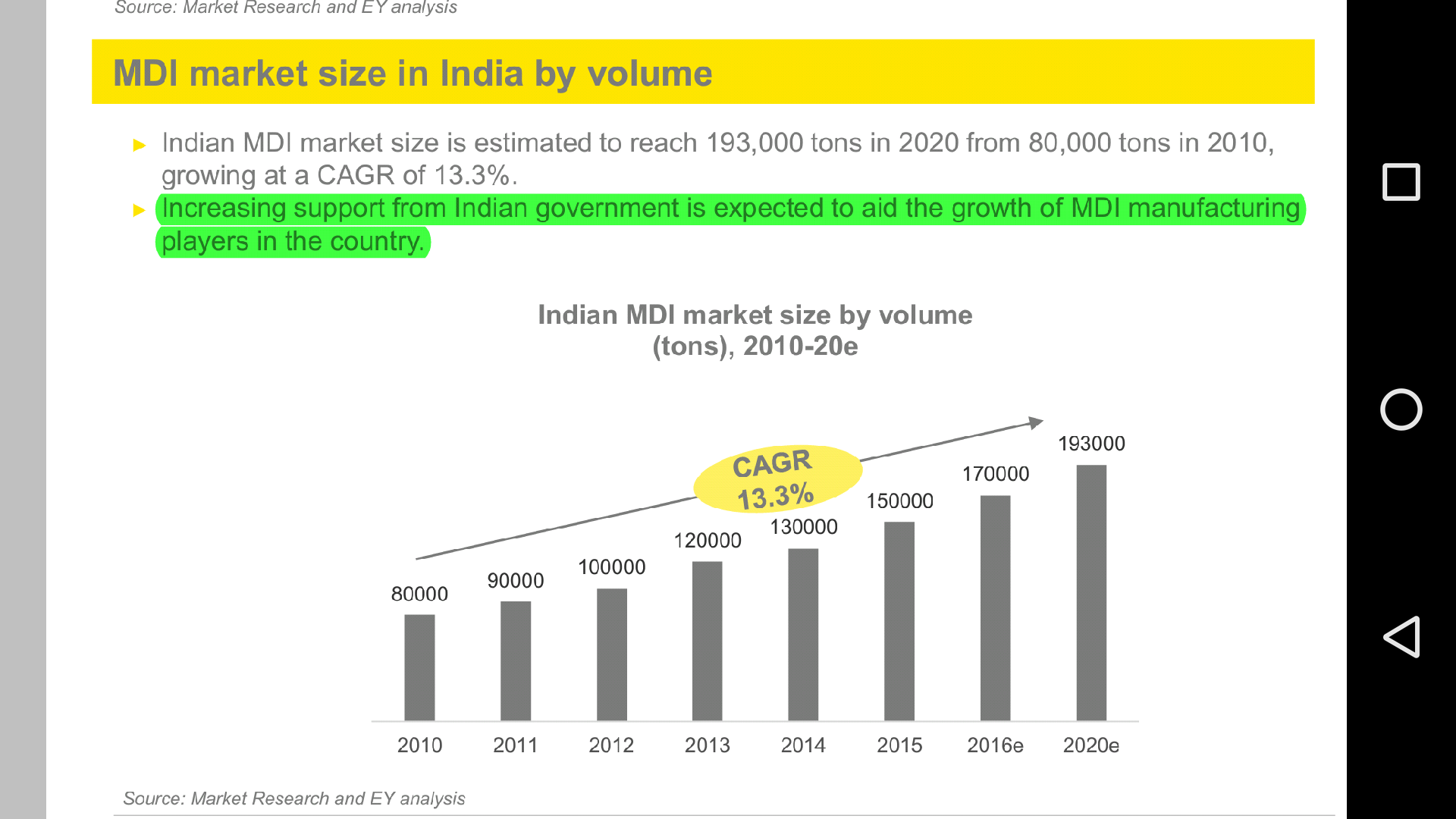

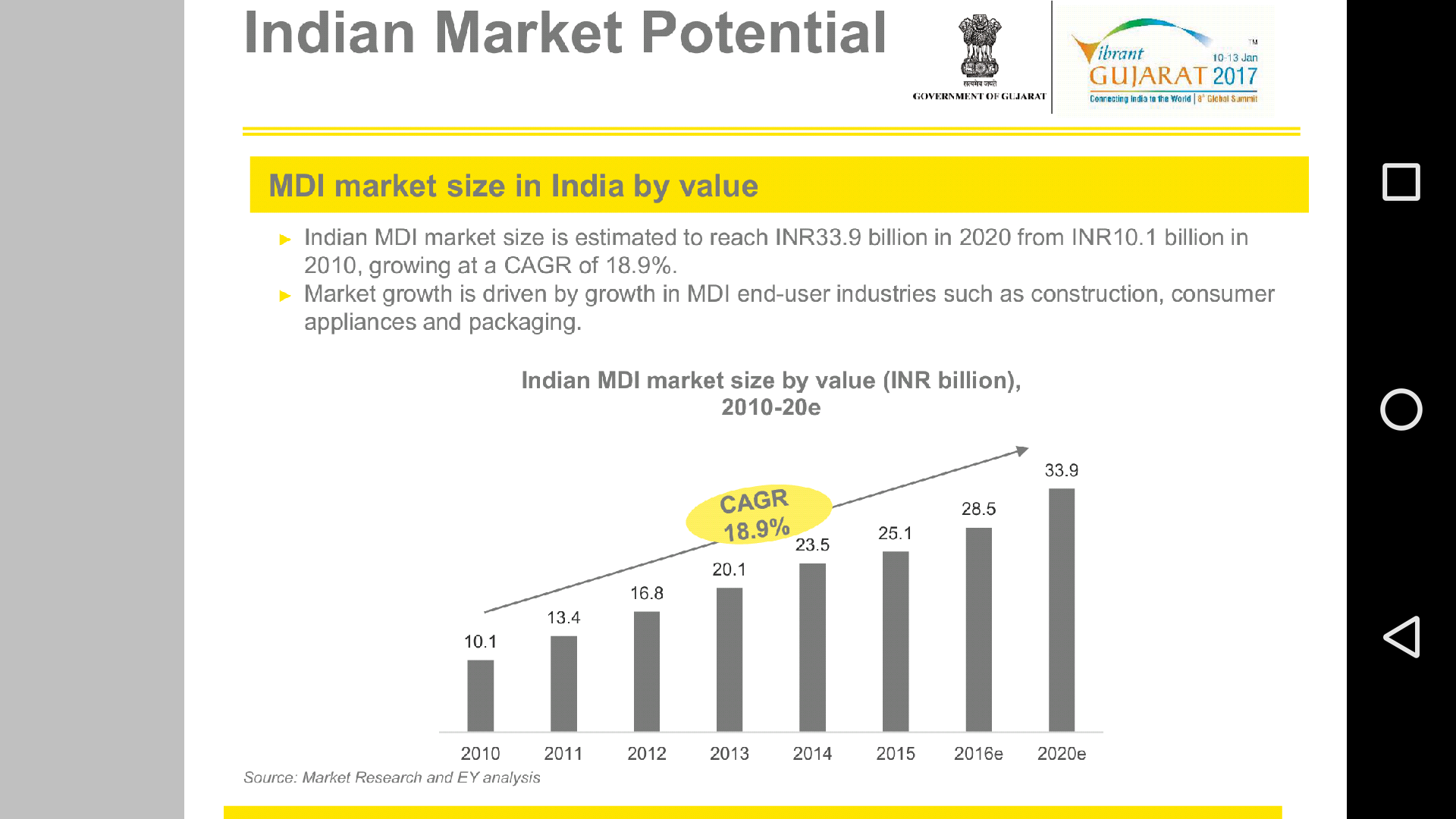

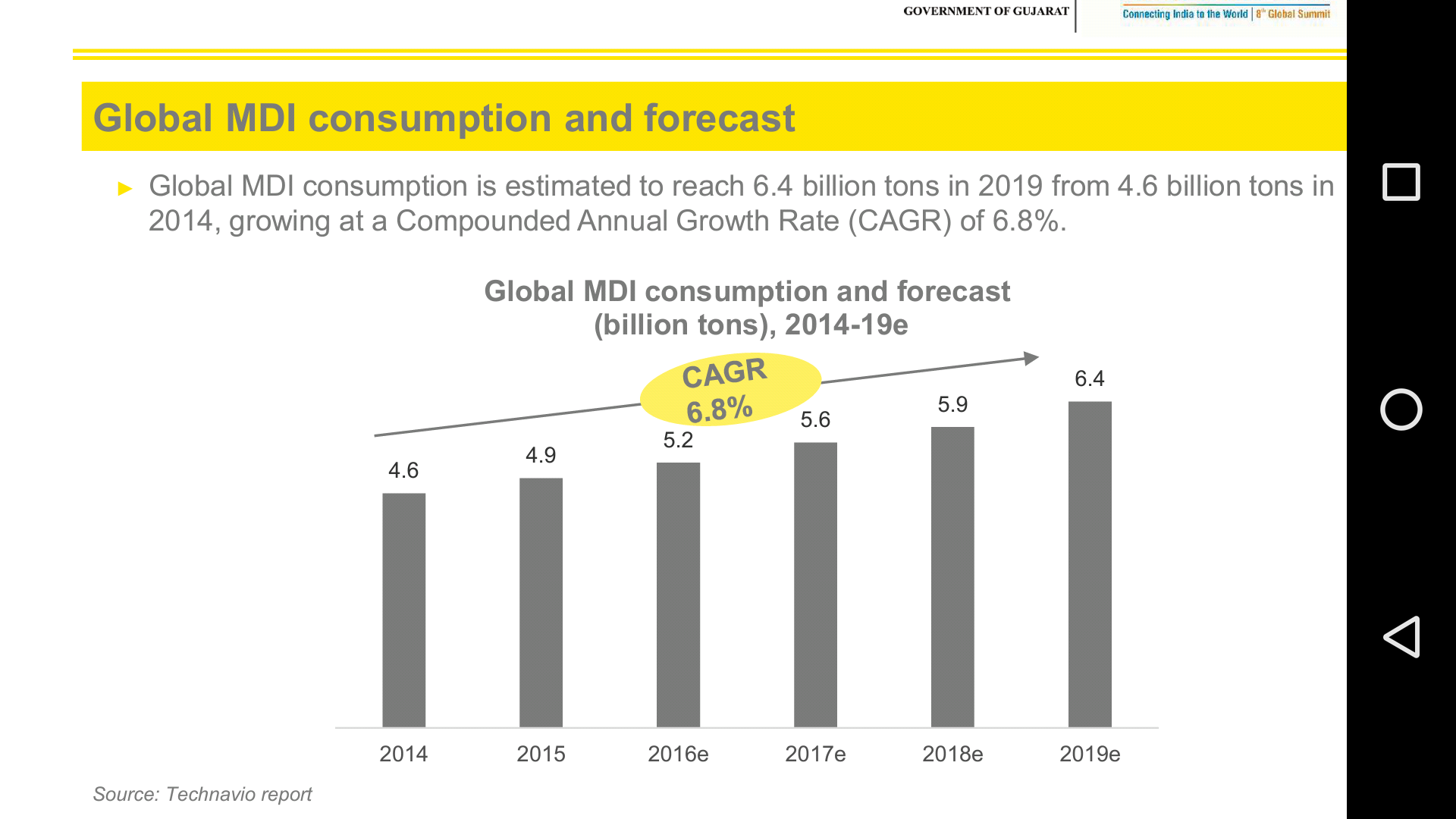

I believe the expansion plans might include MDI coming into gnfc chemical spectrum in a major way…

1.the management expressed plans both in q2 and q3 in blending tdi with mdi and marketting the blend to the global auto sector, presently the only producer of mdi in south east asia is basf india plant in dahej…And gnfc has little to no capacity for mdi as of now…

Read the exerpt from q2 concall…

As of q3 they mentioned they are exploring options in the market…

2.mean while, in 2017 gujarat gov had expressed innterest in setting up production for mdi in vibrant gujarat summit 2017…

3.historically, beside basf which set up plants for mdi as a part of 1000cr project in 2014, hocl was a gov company which used to produce mdi, in rashanyi plant, located in maharashtra, but that was closed down subsequently…the plant used to have prodution of all the raw materials for mdi and all the technologies required was present…

Please note…

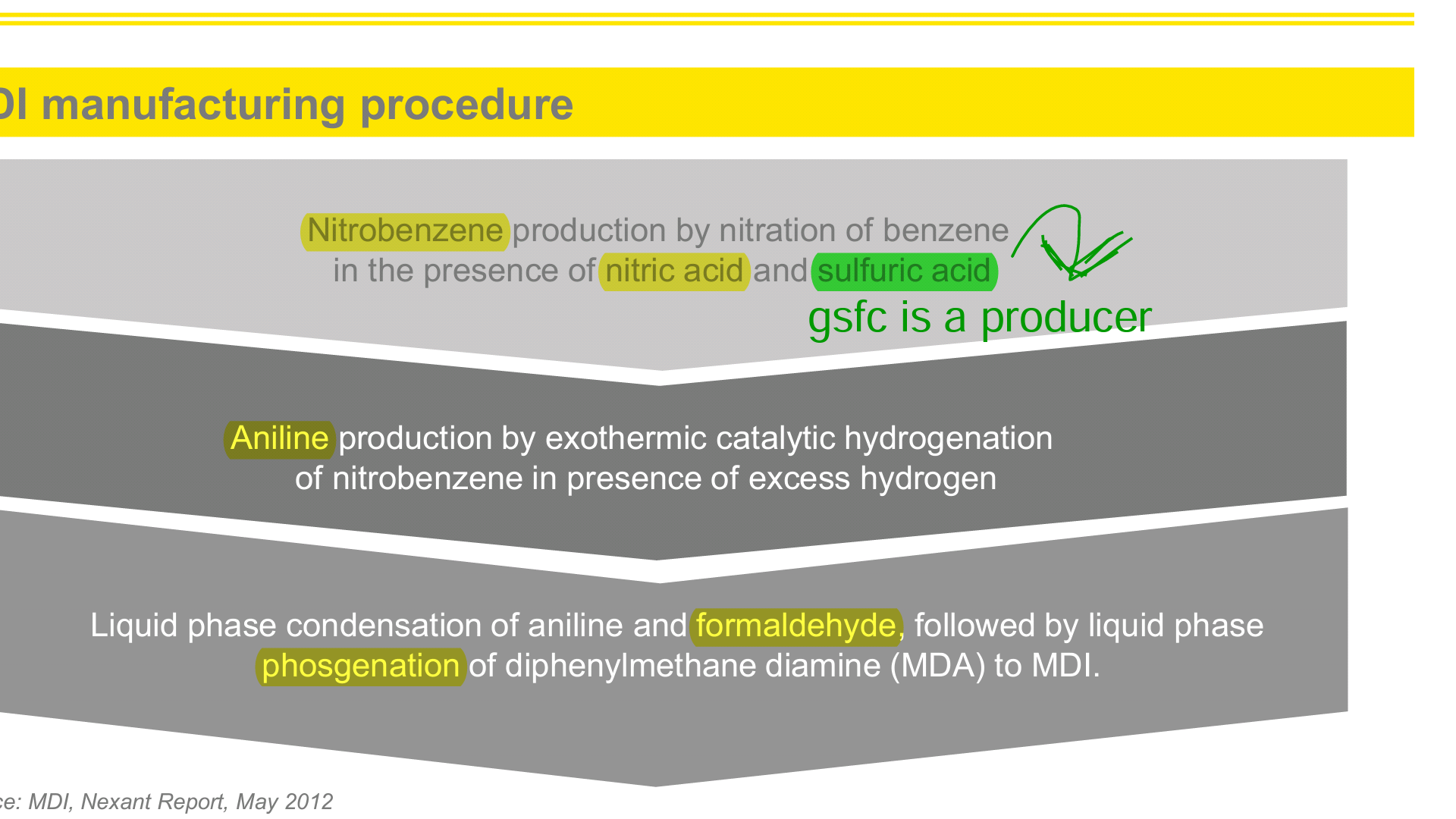

3.raw materials for mdi…

For All marked in yellow , gnfc is already a producer and uses phosgene in tdi plant already and h2so4 can be sourced from gsfc, note all the chemicals required for mdi were produ ed in hocl plant…

4.back in 2007 gnfc had expressed interest to setup capacity for mdi…

Check…

https://www.icis.com/resources/news/2007/07/05/9042895/india-s-gnfc-mulls-50-000-t-year-mdi-plant/

- Mdi prospects …

Note…

6.And mdi is in similar demand to supply crunch , even more than tdi at present…

A report on 30th oct…

Screenshot from this link…

Source…

So in conclusion, i have a conviction that expansion can be on many fronts but in mdi there is a big possibility, according to the latest concall the management mentioned the capez will lead to good increase in topline…

If hocl’s closed down plant can be taken as a brownfield i have doubts as it is in a different geographic location, although the management does not mention if expansion is going to happen exclusively in gujarat…

Also note basf indian mdi plant at dahej is running at less than 50percent capacity

And also note, benzene is a raw material in mdi, and acc to latest concall, rising crude has much more parallel effect on benzene prices than toluene…

While the brownfield in mdi may take time to come online, it will take gnfc to heights which might be only left to imagination…

I could have tried to estimate the topline impact, but without any guidance from the company it would be difficult and purely speculative, hence no attempt…

As of now we might get a methanol plant expansion if required, that has been stressed by the management in q3 call, but that ia not what the com is hiding from us…

Even in this capex plan if we do not see mdi, the company will continue to generate cash and we can expect mdi plant later on, will try to get a direct comment from the management on q4 call…

Will appreciate your views on this prospect…

Disclaimer… Invested

11 Likes

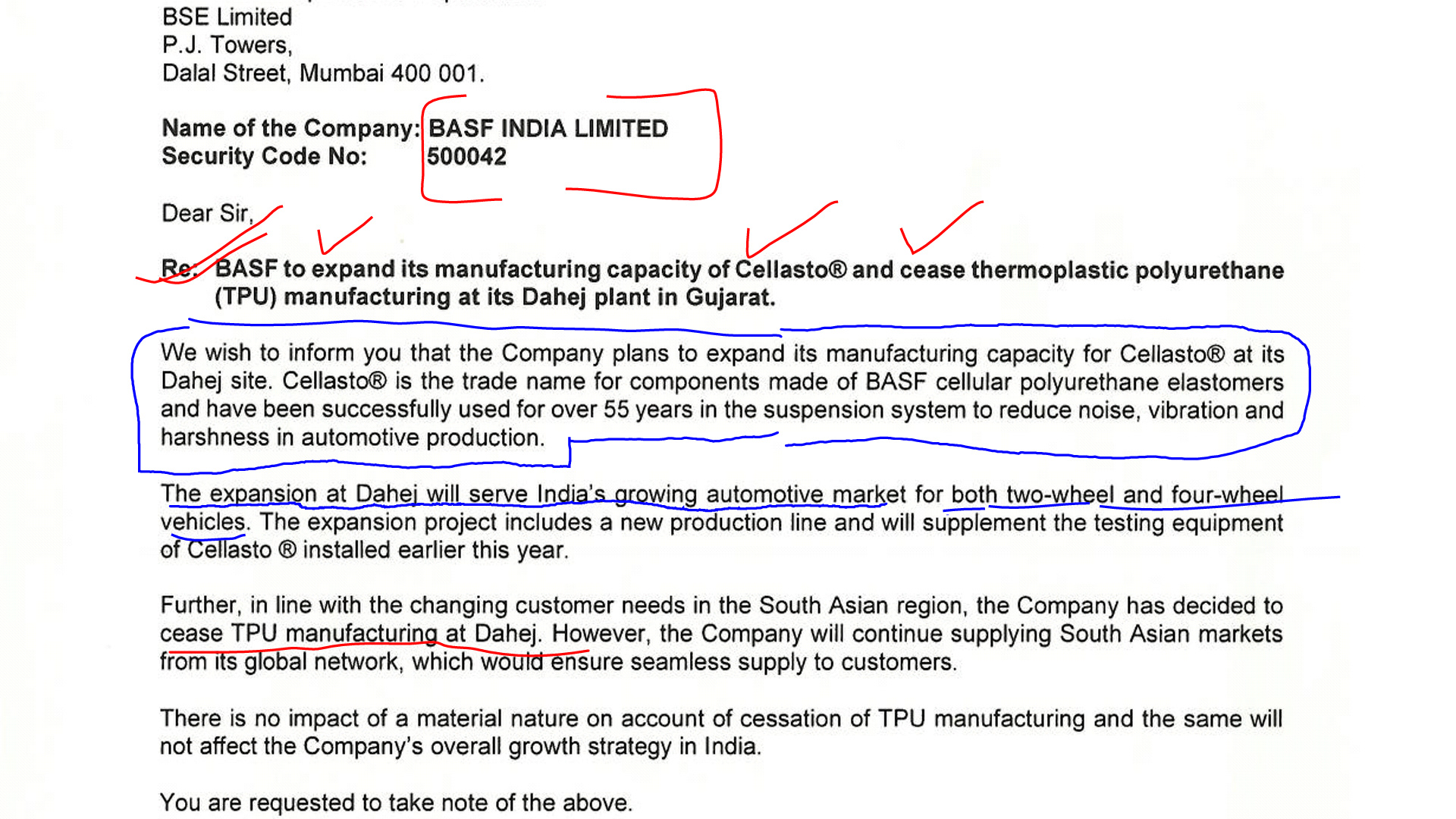

Another related point about BASF…

Tdi and mdi and polyols are used to make different polyurethanes like microcellular(cellasto) and thermoplastic polyurethanes…

Like basf gnfc also wants to cater to auto sector, and highly expect the tdi mdi blend gnfc talks about will receiev a patent and trademark…

2 Likes

Great work and analysis Sir.

The above posts are really investigative and truly help in finding future value rather than just analyse past performance.

Looking forward to reading your posts and its great to have such passionate investors on this forum!

An interesting article on the chemistry behind TDI/MDI and blending. Looks like GNFC is planning to make TDI and blend it with MDI in different proportions going forward. In polyurethane chemistry, everything depends upon how the blending is done. Different sort of foams are manufactured and the thickness, density and usage depends on the blending mix. This to me looks like the possible future direction GNFC might be taking as has been hinted by the management in q3 concall. All RM are readily available at Dahej (Some of it are being produced by GNFC/GSFC). Basic RM for MDI is benzene.

It makes sense as the two chemicals have very similar chemistry, similar RM requirements and similar set of buyers (end usage industry). One more thing which is why this seems highly probably future direction is that GNFC would again be the sole producer of MDI in India like TDI, if this project goes ahead. So, incentives can be good.

Here is a link to the chemistry behind the two chemicals -

5 Likes

@rahulshares… Thank you, but please try to add to this line of thinking as much possible…

I yet didnt find any plants in guj which produces mdi which can look as a brownfield prospect …

If you or anyone comes accross any possible lead , please post!!

1 Like

Formic Acid…

The global Formic Acid market is expected to reach USD 878.7 million by 2023 at a CAGR of 4.94 % during the forecasted period.

Acetic acid…

1.India’s Jubilant Life Sciences plans to bring onstream a 50,000 tonne/year acetic anhydride project in 2019. This would translate to an additional requirement of 65,000 tonnes/year of acetic acid. Construction however, has yet to kick off.

- Asia’s acetic acid market in 2018 is widely expected to be driven by downstream demand growth namely in the purified terephthalic acid (PTA) and acetic anhydride sectors while the lack of new acetic acid plant capacities kept producers’ sentiment optimistic.

the supply imbalance had also deteriorated in China in December due to curtailed production at several plants located in Tianjin , Chongqing and Jiangsu , as the effects of the government’s policies to combat pollution affected the supply of feedstocks such as carbon monoxide.

Spot prices across Asia subsequently hit their highest levels last seen in May 2011 and looks set to start 2018 on a high.

Looking further ahead, demand growth would also stem from the downstream acetic anhydride sector.

Some market players also anticipated improved plant operating rates in the downstream ethyl acetate sector in China next year to drive demand for acetic acid.

the demand outlook in the downstream ethyl acetate/butyl acetate sector was mixed, with buoyant demand expected in southeast Asia, with an increase in plant capacity by 2021 or 2022.

Source…https://www.icis.com/resources/news/2018/01/05/10180158/outlook-18-asia-s-acetic-acid-market-to-be-driven-by-demand-growth/

To simplify…

Outlook in 2018 in acetic acid is +ve, spearheaded by

increasing demand in PtA plant, acetic anhydride plant, chinese slow down, ethyl and butyl acetate demand proposed to grow both in production and demand.

To add an indian hunger, jubilant life is also here but that is a post 2019 story…

1 Like