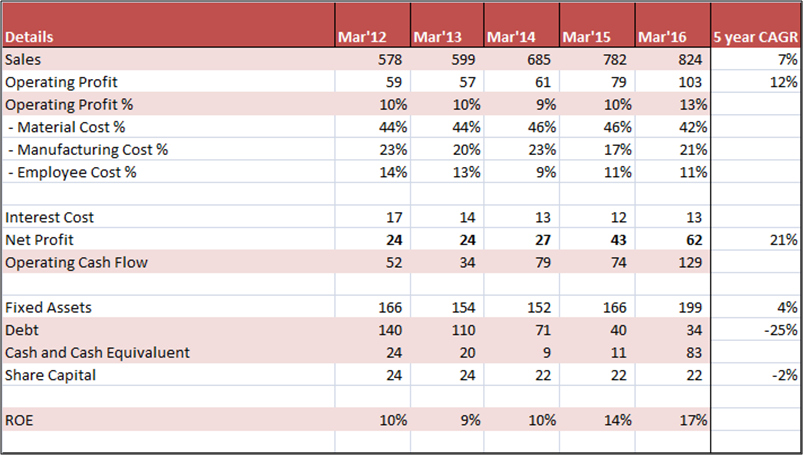

- Despite Crude Volatility, material costs have remained stable at ~45%,

- Manufacturing Costs/Conversions costs have remained stable around 20%

- Debt Free

- Throwing up Operating Cash

3 Likes

5 year sales CAGR is only 7% which is less than interest rates in the country! In the long run, sales growth is more important than bottomline growth. Margins increase have a limit. After that 7% sales growth will be pathetic for a long term shareholder!

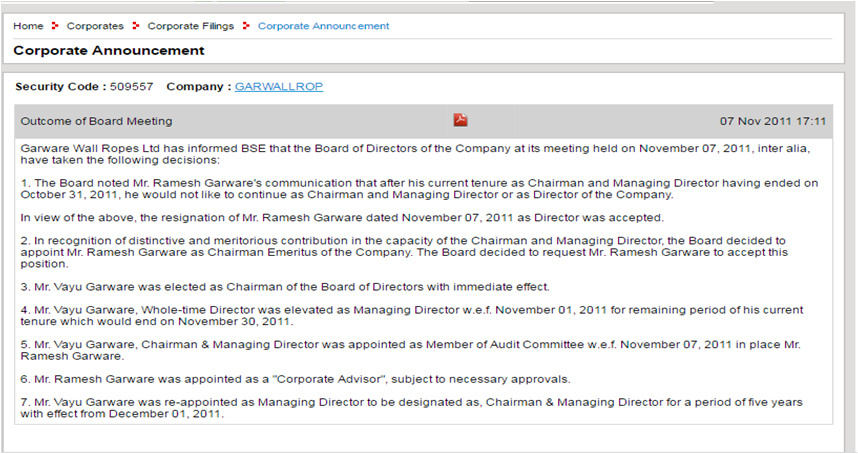

What Changed – New Generation Taking Over

Vayu Garware, took over from 2011. He holds Graduate Cum Laude in BSc Economics in Specialisation in Finance from the Wharton Business School of the University of Pennsylvania, USA.

2 Likes

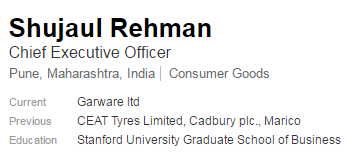

He then appointed Shuajaul Rehman - Shujaul Rehman was brought in by Vayu in May 2012.

He brings 23 years of experience with various Blue Chip Companies

The company adopted a new strategy :

-

Enter New Segments – Protected Farming, Defence etc

-

Launching newer and innovative products.

-

Increased R&D Spent from Rs. 4.8 Crores in 2012 to Rs. 9 Crores today.

-

As per Annual Report - “Garware has been able to develop various new products over last 4 years. Many of these are innovative products and Garware being the first to develop has filed patent applications too.

2 Likes

Plateena – the big differentiator

-

Garware has launched a product line Plateena

-

Plateena is manufactured using from Dyneema - world’s strongest fibre

*** Dyneema is supplied by DSM , a Netherland based supplier**

-

Garware is the only licensee of Dyneema in India

-

Garware uses Dyneema to manufacture fishing nets, shipping ropes and Industrial Products

-

Plateena has with a very strength to weight ratio which replaces the Steel Wire Ropes (SWR)

-

The Plateena Rope is 1/7th the weight of the SWR

-

The rope has minimum drag in the water, thus it helps cut fuel costs by 40%

-

Makes the boat easier to handle - and safer.

-

Is more durable, and requires no greasing, oiling etc – Low maintenance costs

-

Plateena rope made with Dyneema is one of the most sought after product ranges in the international market

4 Likes

Other Innovative Products

Sapphire Ultracore

- Solves the biggest problem faced by shipping community – attacks by sharks, sea lions , which attack nets and eat up valuable fish

- Sapphire UltraCore is a unique cut resistant , protection net

- It is stiff, yet not rigid – easy to handle

- Saves Fuel Costs and increases catch

- Garware has filed a patent on this product

Garfil Star

- Made from patented yarn, Garfil Star offers high tenacity and strength, with lower weight and diameter

- Helps vessel in moving faster and consumes less fuel.

- Patent Pending

StarCage

- Made using Dyneema

- Non Copper Coated Cages – environmentally friendly and also low on costs

- Fatsest growing segment with higher margins

2 Likes

And the company continues to move into new area - DEFENCE

-

Garware has forayed into the Defence Textiles Business

-

GWRL has developed a strong association as an Industry partner with Aerial Delivery Research & Development Establishment (ADRDE) an associate office of DRDO.

-

The partnership has seen successful completion of several projects, transforming the design concepts into successful products and contributing towards indigenization needs of the country.

-

Management expects turnover of over 100 crores from Defence Segment by 2020

Some products being developed are :

- Tethered Aerostat Balloons - Used for Communications, Broadcasting, Advertising and monitoring air traffic control capabilities.

- Inflated Structures for Radars - Weather proof enclosure to protect the electronic equipments from damage due to high winds, flying debris, temperature extremes, icing and sandstorms

- Flexible Helimats - Protect the helicopter and the pilot from brown-outs

- Military Camouflage Nets - to protect personnel and conceal equipment from observation by enemy forces

- High Performance Cordage - for applications in parachutes, transport, aerostat balloons etc.

4 Likes

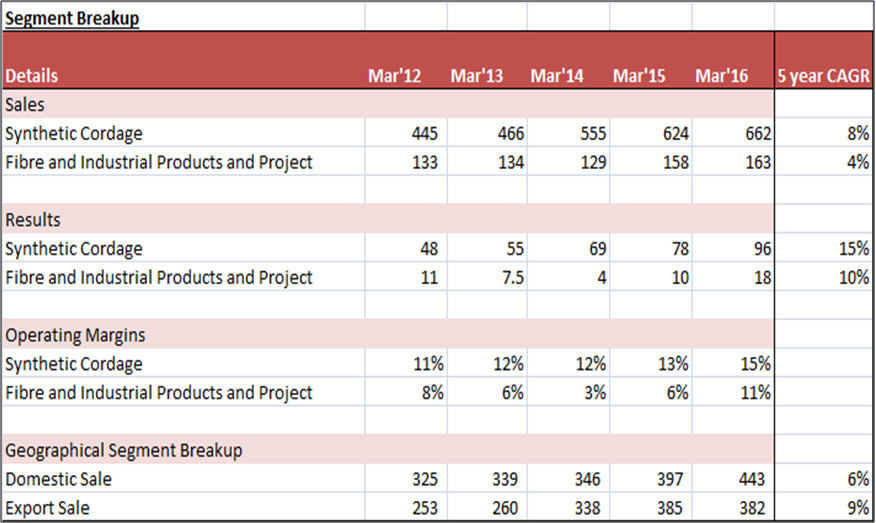

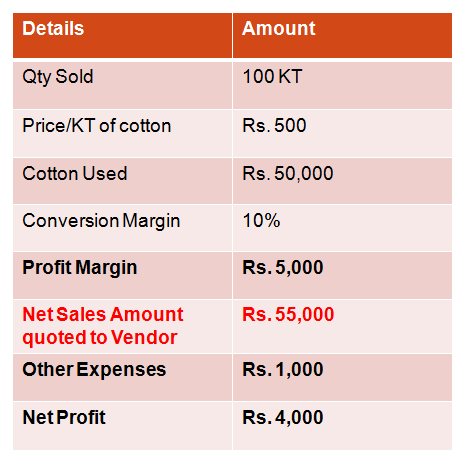

Regarding the much debated and questioned sales figure ![]()

Imagine

-

You sell Cotton after doing some specialized processing on it.

-

So your revenue will be =

Cotton Price + Conversion Margin. -

So lets take this scenario, where your usual margins are 10%

FY 2015 Numbers in this imaginative scenario

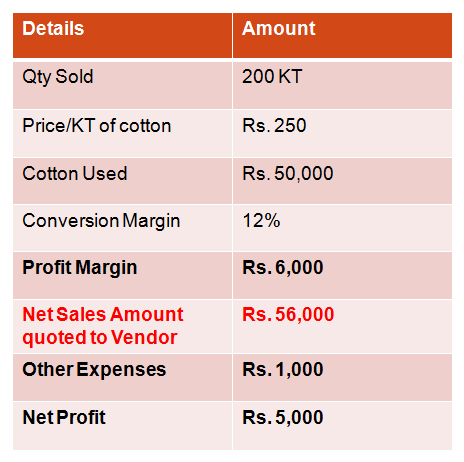

Next year, cotton price falls by half…but because of some good work done by you, you are able to command, 200 bps extra margin…

FY-16 numbers look like this now

-

So Sales, look at same level…but profits speak something else

-

But look at what volume growth did to your bottom line

Cotton, in this example is Crude in case of Garware - from 120 dollar/barrel to 50 dollar/barrel

- Why is volume growth happening - Go back to my point where I mention about Garware’s new strategy under Vayu

6 Likes

Pulling your attention to a beautiful interview with Vayu Garware

3 Likes

- Market Cap of 1400 Crores

- As per ICRA Research , the market size of Technical Textiles is ~90,000 Crore. Within the space of Technical Textiles

- space where Garware operates, the Opportunity Size of the Business ~9000 Crores

- vs current Turnover of ~800 Crores

- Not done any Equity Dilution, infact did small buyback in FY14.

- Never skipped dividend.

- Has maintained consistent margins – in wake of unusual volatility of Raw Material

- At expected earning of Rs.40 for FY 16- Available at a PE of 15 times FY16

- Debt Free

4 Likes

They are creating new markets - where none existed before…

2 Likes

@ashwinidamani

Thanks for taking the pains to update everyone. It’s obvious that you are pretty enthusiastic about the business/management.

Am caught up in many things at the moment to do justice to above, straightaway.

Let’s do a 15-20 min call tomorrow?. PM to let me know your convenience

That will equip me to shoot off some questions - to play a good devil’s advocate

1 Like

I have some queries on the financial statement of 2015-16. If you look at the cashflow statement , under the cash flow from operations, their cash flow after working capital changes have gone up( from 105 crores to 135 crores). Being a working capital heavy industry shouldnt they have lesser CFO after working capital changes ( also note that their trade payables have decreased by 14 crores, receivables gone up by 16 crores and inventories reduced by 12 crores YoY), They should have their CFO decreasing by 14 crores instead of increasing by 30 crores. please point out if I have commited blunder

Other query is cash flow statement says total tax paid is only 5 crores whereas P&L shows 20 crores of taxes paid.

ALL these effectively inflates their CFO.

please clarify

could explain above two queries on their financial statements of AR 2015-16

Thanks Ashwini for your call and the crisp update on aspects to notice in GWL business.

Here’s a summary of the observations again - to expose my “assumptions” behind decision-making in a case like this. Hoping this encourages more folks to enagage deeper - by exposing the “assumptions” in their mental-models.

Things we like, that we can spot in this business:

- Dominates some niches, moving up the products value-chain, Good mix of Domestic/Exports

- Ability to command a premium over competition (in some segments)

- Stable & improving margins, returns profile, and cash flows (despite crude cycles)

- Consistent reduction in debt, with growth

- Managing growth without equity dilution

- Conservative Management, solidly consolidated over past decades

Things we find interesting – take note/keep track of - disproportionate building blocks??:

- Investments being made for developing Defence Textiles segment

- Consistent new product introductions/backed by increasing R&D spend/Patents

Normally a business/management that has solidly consolidated over the last decade (and more), addresses global opportunities successfully, and exhibits a robust business model throwing out cash - would be “hungry” - would be aiming for “above-average growth”.

While no doubt these are laudable characteristics in a business (quite like an Ambika Cotton déjà vu), from a medium-to-longer term opportunity perspective we prefer business that do not exhibit following: (would love @ayushmit to differ/and rebut here – please don’t kill me )

Things we don’t like (especially in small caps), that we can spot in this business:

-

With near-zero investments in fixed assets over last many years, the business is continuing steady-state operations. Future Value creation, as exhibited by Economic Profit Added (EPA) every year, is minimal over last several years. FCF doesn’t count for much in such situations

-

Management indications that there will not be any growth capital needed for next 2-3 years, post the 30 Cr invested last year – Is that correct? Buybacks is another pointer for better use of Cash?

-

If this is NOT an indication of lack of Management drive (seems unlikely given the excellent narrative in this thread), then is it an indication of (currently) low addressable market before it? ~roughly at 900 Cr Sales vs 9000 Cr (including exports) as per ICRA. Is that correct??

-

Given current valuations (consolidated 22x), and the lack of Incremental Invested Capital in the business in near to medium term, is there lot of “Hope” priced in versus “Visibility”?

Surely in Feb/Mar 2016 at 600-700 Cr Mcap, this kind of a business should have been a no-brainer, and congratulations to those who latched on to it. If someone is looking at a fresh investment and/or holding on for the medium term (at current valuations), one should factor-in/question more on the don’t-like data points. There are better opportunities in current markets?

Disclosure:

Not invested. My current familiarity with the business is next to zero (am willing to learn), so everything should be taken with a pinch of salt. This case should be used more for discussion on the kind of decision-making mental models we have in-our-minds, and “expose” them for others to engage deeper.

Caveats:

- Should the “Addressable Market” assessment in medium term (next 2-3 years) be different, and Management stance on Incremental investment changes – gets backed up by fresh investment, this is a re-assess

- If “Defence Textiles” segment shows signs of concrete earlier fruition, this is a re-assess

8 Likes

Donald, there is one point I would like to make - why are so many investors hung up on the defence textiles moniker? Defence textiles are not such a big market and the orders take a long time to materialize. There is little visibility on the runway for these kind of orders and they should be regarded as being a ‘bonus’ for the business than anything to rely on.

Investors (as in the Shiva Texyarn thread) should not focus so strongly upon defence products to make out a case for a long term investment opportunity (and it is long term in the absence of any current meaningful contribution from the segment). Such emphasis is misleading, whether they realize the investors realize it or not. I do a lot of work with MNCs and Indian companies in the defence space (in slightly more advanced products and not textiles) and it is my experience that defence orders are not regular and cannot be relied upon by any company as a future reliable growth field. It is only the cherry on the cake.

A few cases in point that would be readily understandable by investors would be Astra Microwave and Zen Technologies. Both are companies mostly focused on defence orders and it is plainly visible that one cannot rely on such businesses to sustain their financials in even a roughly linear manner. This is wholly admitted by the managements of these companies too.

My short point is, “defence” textiles are not as big a game-changer that is made out to be in the technical textile space. It is a bonus and little else.

9 Likes

@Leading_Nowhere

Tushar, Let’s talk sometime in the new year. On holiday from tomorrow will be good to hear from you on what you picked up.

In general I agree with your assessment of defence textiles segment shouldn’t be factored in current assessment for someone like GWL where the horizon is distant. Also that multi-year order continuity (even when announced formally in procurement docs) cannot be taken as a given. Don’t think anyone made that case in this thread.

When it comes to specifics, there are oligopoly/(actually single player) situations like as in ShivaTex NBRC suits where there could be disproportionate returns should Order Visibility over multiple years continue (for couple of more in-pipeline products).

On the same lines reportedly there are more such oligopoly niches like in high-altitude gear etc that some businesses are positioning/in-trials for. So defence textile segment is a watch - where clearly GWL has been investing in for some time. Could there be something there?

(post withdrawn by author, will be automatically deleted in 24 hours unless flagged)

Garware Wall Ropes has clearly guided that not much of revenues to come from defence and they target a max of 100 cr 3-4 yrs down the line.

The change in the company has been amazing from 100-120 cr of debt in 2013 to almost closer to 100 cr cash by March 2017.

At current levels its not cheap and it will not be a 20% topline growth company but more closer to high single digit growth.They have been able to improve margins with a lot of value addition.

In the last 3-4 years the company has consistently increased product lines and geographies. So decent growth and decent margins say around 14-16% and 6-10% topline growth is what i expect. Tough to buy it at 20 times unless one is going to stick for a real long time with an innovative company.

The big question now is what will the company do with accumulated cash. Would like more dividends or acquisitions.

Disclosure - Holding it as a core position from 250-350. Trimmed quite a bit given the current move.

5 Likes