What is the impact of the deal with the Israeli company ? Any one has the details of how it would contribute to revenues etc

India has got a long border with Pakistan n China. Gwr has been in investment phase in defence sector for last 3_4 years without much results to show . This delayed gratification is v imp characterstics for an able mgmt n Vayu Garware best exemplifies it. Hopefully now the time has come gor these investments to bear fruit as Israeli aerostat are already deployed by Indian army. These will.now be made in India by GWR leading to lower costs n increasing the opp size for Gwr.

5 Likes

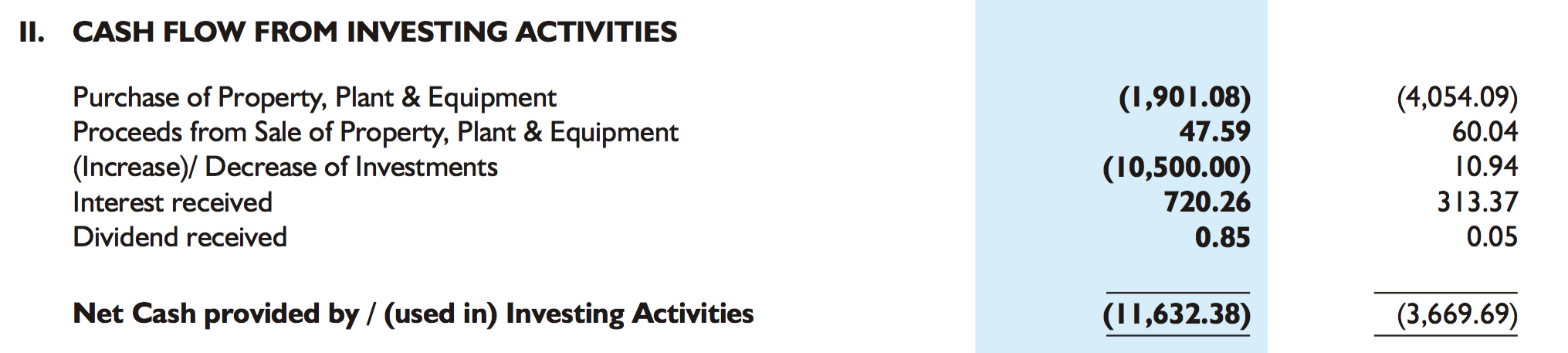

Hi Guys, I was going through AR and was trying to understand the logic of huge ‘increase in investments’

And when we go into details of it, they have significant investments in Equity of other companies and Bond/Debentures too.

What could be the logic behind this ?

Investors have put their money for the core business and not for a proxy investment in other companies where Garware has further invested.

If they don’t have means to invest the surplus cash in their own business and hence investing in other companies, why cant they buyback their own shares and reduce overall equity. That will benefit the shareholders.

Disc : Invested

1 Like

Here is my take -

-

This is now a net cash company, they can retire debt in one single shot if they want to but they will not. They can borrow at LIBOR + 100 bps through the packing credit route, do not need to hedge since exports will anyway cover the FX risk. The arbitrage here by investing cash in India market securities is upward of 4%

-

The investments that you are referring to are into structured products (ELD’s) with Reliance Capital etc. That is once again a financial investment into a fixed income + kind of security, approx 42 Cr here if I remember right. All other investments are into short term and ultra short term MF’s which most corporate treasuries anyway do

I do not have any concerns with how the company is deploying cash into investments. Where I do have a problem is with some tax liabilities where the logic seems to be a bit fuzzy.

We will soon have a scenario where the management gets accused of not being aggressive enough in doing capex, this year approx 80+ Cr will get added to their investment portfolio. The nature of the business is application specific products which needs minimal R&D, existing capacity appears good enough for next 2 years.

Free cash flow engine this is for sure, would actually love to see higher dividends and another buyback (they did one in 2014) once the stock price settles down to some saner levels

9 Likes

@zygo23554 , Thanks for your response.

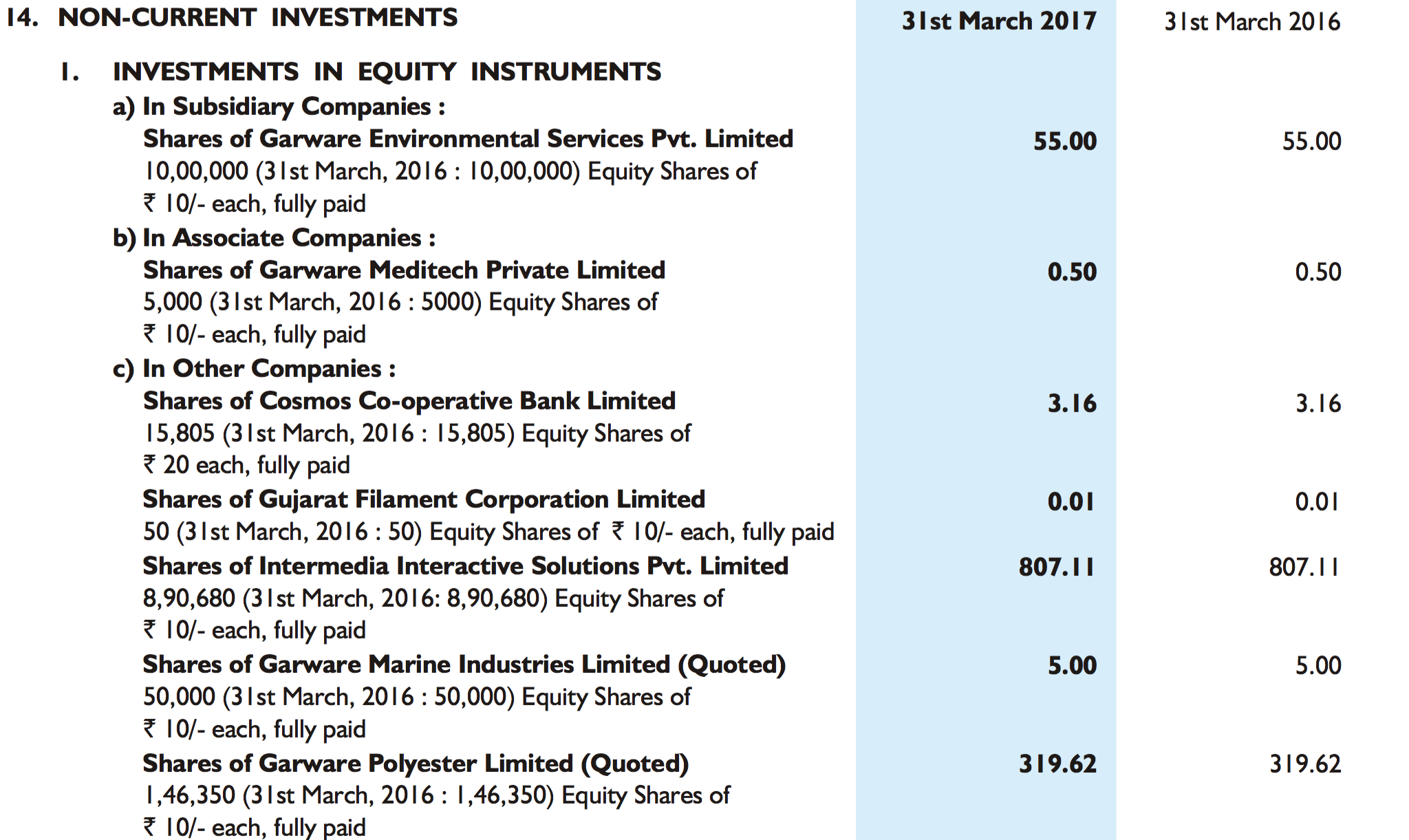

Investments that I am talking about are the following where they have invested in few other companies

Other investments which might be for fixed income are

I guess majority of other income will be from above investments only. 11 Cr from 117 Cr investments. Approx 9.4 % income. Seems average.

Other query I had was

Why they don’t disclose current value of the investments ?

1 Like

Nature of the investments is fixed income, hence market value will usually be higher that cost. MTM should ideally be done and declared but once again this is not followed usually.

You are right that the fixed income MF’s will probably deliver 8 - 8.5% gross from here per annum before taxation, hence other income will need to be calculated on that basis as a % of the amount invested

5 Likes

2 Likes

I was just browsing thru that stalwart advisors site and find that they exited this stock in june 2017. the blog was written in may 16, 2017. it might just be a coincidence. but i find it interesting. these days it has become very common. of course they have every right to exit at any time.

(dicl: i am not subscribed to any paid recommendation services or pms)

Two recent observations:

1.The promoter (Mr. Vayu Garware), acquired 1,84,632 shares of Garware Wall Ropes, on 24th August, 2017. It is not mentioned that it was from open market.

Before this transaction, he had only 19,658 shares (0.09% of total)

After this transaction, he now has 2,04,290 shares (0.93% of total)

This was reported to Exchange on 29th August, 2017:

http://www.bseindia.com/stock-share-price/stockreach_insidertrade_new.aspx?scripcode=509557&expandable=2

Mr. Vayu has definitely had the most important role in turn around for Garware Wall Ropes, and I view his buying of these shares as a positive.

2.Mutual Fund Interest

March, 2017 SHP:

http://www.bseindia.com/corporates/shpPublicShareholder.aspx?scripcd=509557&qtrid=93.00&QtrName=March%202017

There were 3 MF’s holding 1300 shares (0.01% of total)

June, 2017 SHP:

http://www.bseindia.com/corporates/shpPublicShareholder.aspx?scripcd=509557&qtrid=94.00&QtrName=June%202017

There were 8 MF’s holding 3,40,039 shares (1.55% of total)

It is interesting to see that the MF holding has gone up from 0.01% to 1.55% (HDFC and SBI funds brought those shares). And of course, the retail holding has gone down by a slight percentage.

6 Likes

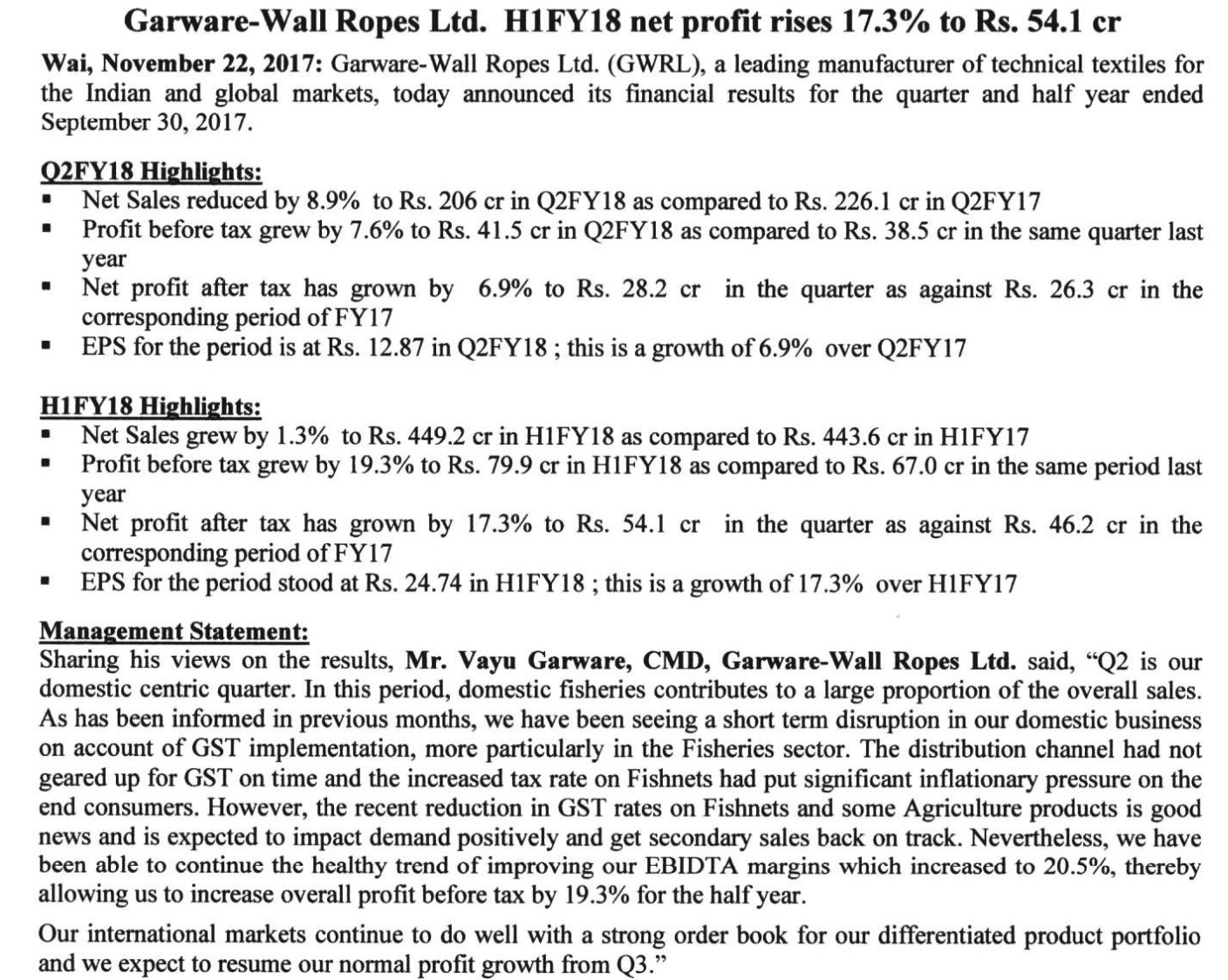

Q1-17 result

http://www.bseindia.com/xml-data/corpfiling/AttachLive/ab389c90-f792-472a-b7ff-2d0bd48049fb.pdf

1 Like

Inter se transfer, not buying

3 Likes

I noticed that 54% of revenues come from nettings segment and this is the biggest contributor to the topline growth of the company.

Does anyone have the breakup of the revenue contribution of each sub-segment under nettings? and the projected growth in those sub-segments ?

This is crucial to understand future topline growth

Hi Guys,

I was wondering why Mutual Funds have not shown interest in such a wonderful story. Can anyone think of any reason ? Do they see any risks associated ?

As per post by Sumeet Shah ( above) , MF holding only account for 1.55 %.

Will increase in Crude ( Raw material derived from crude) price affect the margins or being manufacturer of niche products it will be able to pass on the cost to its customers ?

Disc : Invested from lower level.

The later the MFs come in the better for retail investors…As they can

accumulate before the rush from MFs to buy the stock…The one key reason

possibly for the stock being out of MFs radar could be that the management

is not proactive in communication. They don’t conduct investor/analyst

concalls and they dont participate in any of the brokerage

conferences…They come in TVs that too very occasionally… Again very good

for retail investors to accumulate the stocks in its gradual rise. It is

only a matter of time before the stock comes into the limelight

3 Likes

An analysis of GWR by Dr Vijay Malik. Chief negative highlighted in this analysis is the high management compensation. Most of the report has been discussed in this thread and is broadly a positive read on GWR. Does not talk mich about valuations though.

2 Likes

Flat results on account of GST, company optimistic on H2

http://www.bseindia.com/xml-data/corpfiling/AttachLive/0d9162c1-51f6-42c6-b9b3-9c8950129cfd.pdf

2 Likes

Numbers are okay. Rather, increase in operating margins comes as a surprise.

Though, again, some heads under balance sheet are odd. They have 225 cr receivables on sale of 210 cr this qtr. 111 cr working capital loan taken (they are paying close to 10% interest on this it seems). Their long term investments are earning lesser than this. No point taking debt in that case. Rather they should liquidate some investments if they have working capital requirements for which they are taking loans. Part of the working capital may be fulfilled with 74 cash/bank balance.

Also, it looks like they do not need capex. So, they should rather increase dividend yield now rather than accumulating money which they have employed at 9% yield.

3 Likes

@Mridul , Valid points, even I am of the same opinion and against company doing investments and then paying interest on the other side.

However one thing that we retail investors are not sure about is whether company is planning for some suitable acquisition and accumulating money for that. Current management seems good and have really turned around things in last few years hence just trusting their acumen.

Two posts before there is link for Dr Vijay Malik’s analysis and he has tried clearing some doubts around the investments, you may want to review that too once.

On receivables, need to clarify if it increased on account of Govt dealing or exports. However how do we do that as their IR doesnt respond to emails and company never hosts conf calls

Regarding receivables - as long as the delta between receivables and payables doesn’t expand too much, the cash flows should remain intact. The delta is only 15 crore at the moment, which is pretty decent. The loan aspect is something they should really work on. Remember, they also take regular deposits from promoter entities and pay a nice interest on that. It’s only a few crore per year, but it’s still something.

1 Like

Nice report to understand the summary of business and some financial numbers for additional info:

Garware-Dec-2017.pdf (2.5 MB)

Dont bother too much on target price etc.

Disc : Invested

4 Likes