Been holding this since Sep last year, done well for me and have good hopes from this going forward as well. Things that appealed to me when I researched this (am listing only the crux of my investment thesis here)

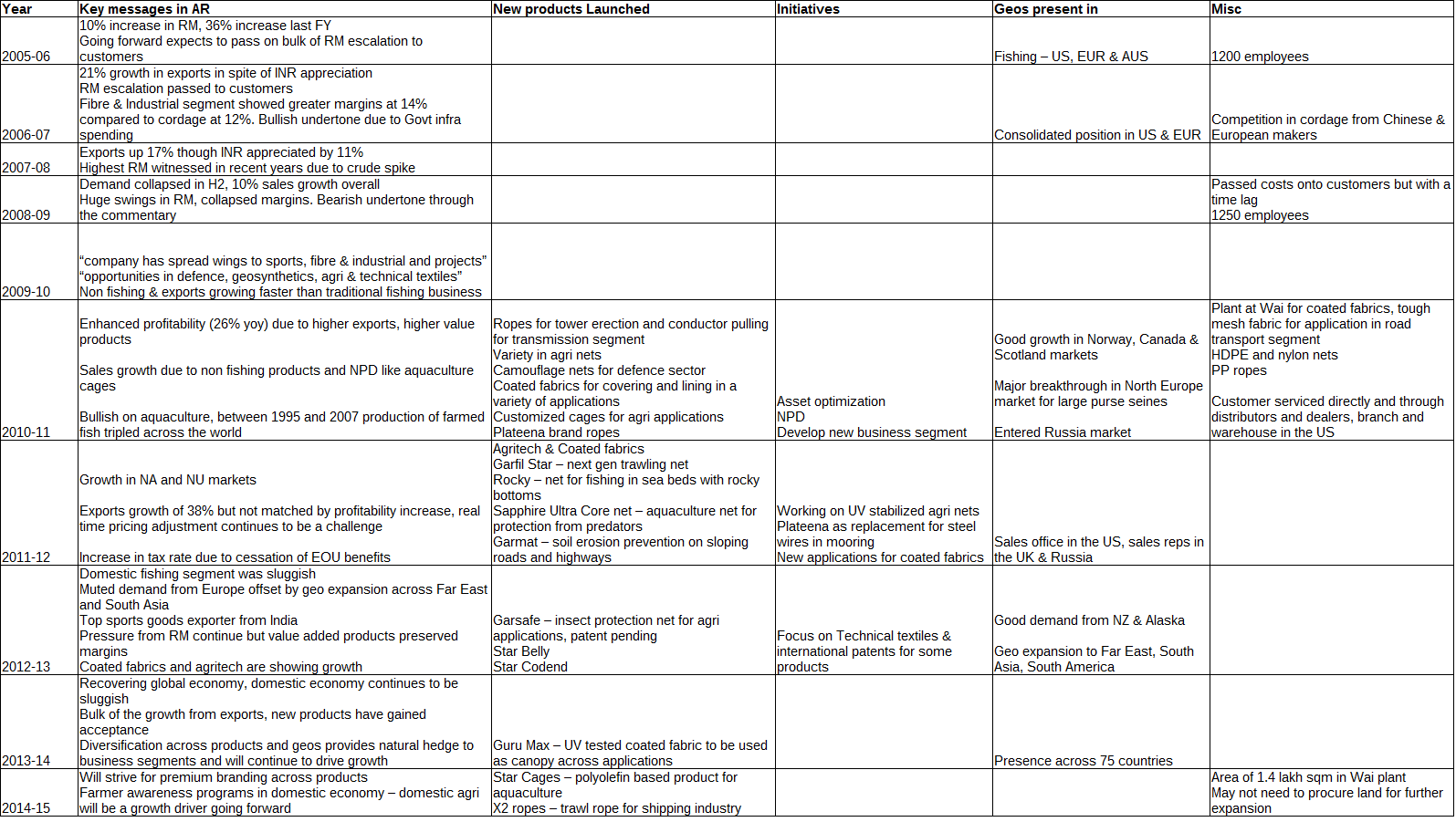

While this has not been a high growth business over the years it does not take too much effort from here to build products for new avenues. Technical textiles is a huge industry worldwide, though GWRL is playing only in some segments (Sportech and Agrotech) they have demonstrated the ability to build customer specific products without too much investment in R&D. Attaching a snapshot from my research note, the R&D and New prod Devpt appears to be well managed. Possibilities appear very exciting though there is quite some distance to go before the company can demonstrate the ability to tap into an addressable market size of 50,000 Cr per annum.

Very good financial discipline, it was very evident from the cash flow analysis that profit/incremental capital would be high over the next 3-4 years. They have spare capacity in the industrial segments that can be put to good use in Govt and defence based domestic orders. Positive FCF at an OCF yield of almost 9% meant that downside would be very limited even if things were to go wrong. Met my criteria of an asymmetrical payoff matrix, upside to downside ratio clearly in excess of 3:1

Dominant position in most of the segments (fishing nets, sporting nets) with aquaculture showing promise going forward. Incremental growth expected to come in due to tapping into newer geos initially before the NPD cycle assumes critical mass

Demonstrated ability to ride out commodity cycles without too much variability in margins, a management that appears very reticent to run after publicity and believes in focusing on what’s happening on the ground

This was one of those cases where the possibilities looked promising though the path to glory wasn’t very apparent to me. The final decisive factor for me was the valuation at which this was going, I was willing to put in a bet that would yield multibagger results for above average results and keep my principal intact in case things continued to be average. At CMP it looks fairly valued for the prospects unless something fires which can tip the medium term growth rate to over 15% yoy

I had presented this to a couple of funds/investors and none of them were willing to buy this based on my logic. Guess that’s the advantage that we retail investors have - we can be agile, stay under the radar and take time to build our positions.

Disc: Invested, this is a 4% of my net worth kind of position since I am investing based on possibilities, not based on strong conviction like I have in an APL Apollo or a TCPL

How does this data show co-relation. Crude went from 40 to 120 and back to 40 and still ur table shows RM costs remained near 45 odd % and margin remained 55% odd.

the other thing to look is probably more subtle. If you read the last 4-5 year reports see the focus of company moving to Operational Excellence. That is one theme that has more and more share in AR as years progress. The same is also reflected now in way the ROA’s & FA turnover has improved.

So the margin expansion piece i think is an evolving story ( not very sure on this), the OE part is something that is visible.

This zero debt quality small cap with a ROCE of 26% has moved in a stealth manner to 536 from 2 figures when first discussed. Company has consistently reduced its debt now to zero and has been constantly increasing its ROCE over last few years.

Its the leader in its segment which itself is expanding nicely like nets for fishing,aquaculture,agriculture,sports,defense,infrastructure . The mktcap vs opp size ratio is still v attractive imho.

Both promoter Vayu Garware a Wharton passout and Shuja Rehman its COO a seasoned mktg professional having worked in several MNCs and Indian FMCG sector are in the right age bracket of 40s.

They are full of growth mindset and their focus towards building brands,distribution reach n R&D is giving great benefits to company.

Its name is a misnomer aka Peter lynch liking.

Any update on any defence breakthrough for the co?

So we recently initiated positions on Garware Wall Ropes LtdBSE -1.41 %. Now this company have not come out with the results this quarter but if you look at the last couple of years’ performance, the work the company has put in over the last five years has paid dividend. It is one of the largest technical textile manufacturers in the country with more than 1000 workers and three manufacturing facilities.

If you look at the performance of the company over the last three to four years, from a top line of less than Rs 500 crore, it is now north of Rs 850 crore and EBITDA margins have jumped up from 11-12% to close to 15% now.

This means the profits for the company have grown multifold from less than Rs 20 crore to Rs 64 crore in the trailing 12 months. This means the company has been able to become completely debt free and this they have done post two buybacks. They now command 25% market share in US in sports nets. It is close to a $3.5-4 billion market that these guys are addressing and with revenue of close to $130-$140 million, they are just scratching the surface.

The management is extremely competitive and we are very excited about what they are trying to do over the next two to three years and this is something that we own and we really like for a longer term period.

Yes. Company has good prospects. But look at Viraj Nehta in that link you referred. He was asked a different question and he just chose to answer about what he bought. Looked silly really…

Well, if his PMS did not have any exposure in any of the stocks they asked about, it makes logical sense to talk about what he does have in his portfolio.

Good results!

8.4% rise in net sales

69% rise in PAT

Top line has a slower growth, bottom line good growth.

EPS has increased to 11.89 almost 60% rise as compared to EPS for Sep 2016 last year.

Have yet to study in detail. But here are the results:

This is now an FCF engine. Cash & equivalents have now built up to 100+ Cr. Not sure if the more than expected margins will sustain going forward though

The driver for the next round of re rating will be the ability of the organization to tap into new segments and accelerate the new product development process. If the management can convince the market that they can put all this cash to good use and enhance the addressable market size through new products, this has a long way to go from here

At CMP this is fairly valued for the current scope of business, due to the free cash flow generation and cash on books the downside may not be very high from here for early entrants (those who hopped in when the market cap was below 600 Cr)

I have some queries on the financial statement of 2015-16. If you look at the cashflow statement , under the cash flow from operations, their cash flow after working capital changes have gone up( from 105 crores to 135 crores). Being a working capital heavy industry shouldnt they have lesser CFO after working capital changes ( also note that their trade payables have decreased by 14 crores, receivables gone up by 16 crores and inventories reduced by 12 crores YoY), They should have their CFO decreasing by 14 crores instead of increasing by 30 crores. please point out if I have commited blunder

Other query is cash flow statement says total tax paid is only 5 crores whereas P&L shows 20 crores of taxes paid.

@Donald So trying to re- attempt , explaining the story

About Garware Wall Ropes

Pioneers in the synthetic cordage industry in India

World’s largest producer of polymer cordages

Has shared a close bond with Indian fishermen for the last three decades, becoming a household name in the fishing community.

Has a 70% Market Share in Domestic Fishing Market

Also a very significant player Globally, with its products being exported to 75 Countries - ‘Star Export House’ status for many years running

The fishing industry looks to suppliers such as GWRL as the providers of new technology that help keep fishing a profitable business

Received the largest sports goods and sports nets exporter award from the Sports Goods Export Promotion Council, sponsored by the Ministry of Commerce, Govt. of India.

Paying dividend every year since inception in 1976