A latest interview

Discl invested since 2015

A latest interview

Discl invested since 2015

The Annual Report 2015-16 (available at:link) is a good read. The emphasis on people and community development is something that is slightly reminiscent of great organizations like ITC.

Notes from AGM:

There is a continuous shift from traditional businesses to the new businesses like Aquaculture, Agriculture and sports. Fishing now contributes about 20% of revenue.

New products taht have been launched in Aquaculture segment has been well received and is doing well in the export market. It is likely to do well for next 2-3 years. Product development and innovation is critical. Company is able to tap new geographies to cater to growth.

There is a possibility to grow exports at double digits in FY17. Company exports to more than 75 countries with North America, EU and US as prime focus. Brexit impact is limited as the company does not directly to UK.

On geosynthetis and defense side, things are going slow. Infrastructure activities are yet to pick up.

The company has sufficient capacities and latest technology to meet the growing demand in the sector and does not think it will require any additional capacity. Focus is now on spending on R&D and on increasing the reach and distribution, rather than on capacity addition. The company wants to play a value game more than a volume game.

In FY17, the company expects the momentum to continue with major gains coming from increase in margins. Sales growth may be muted due to lower raw material prices. The value per unit is rising which will lead to higher margins.

Overall, management expects the momentum in the business to continue and higher margins will lead to higher bottom line in FY17.

I apologize if this is slightly off topic, but a good read of the Baseline survey really shows Garware in good light.

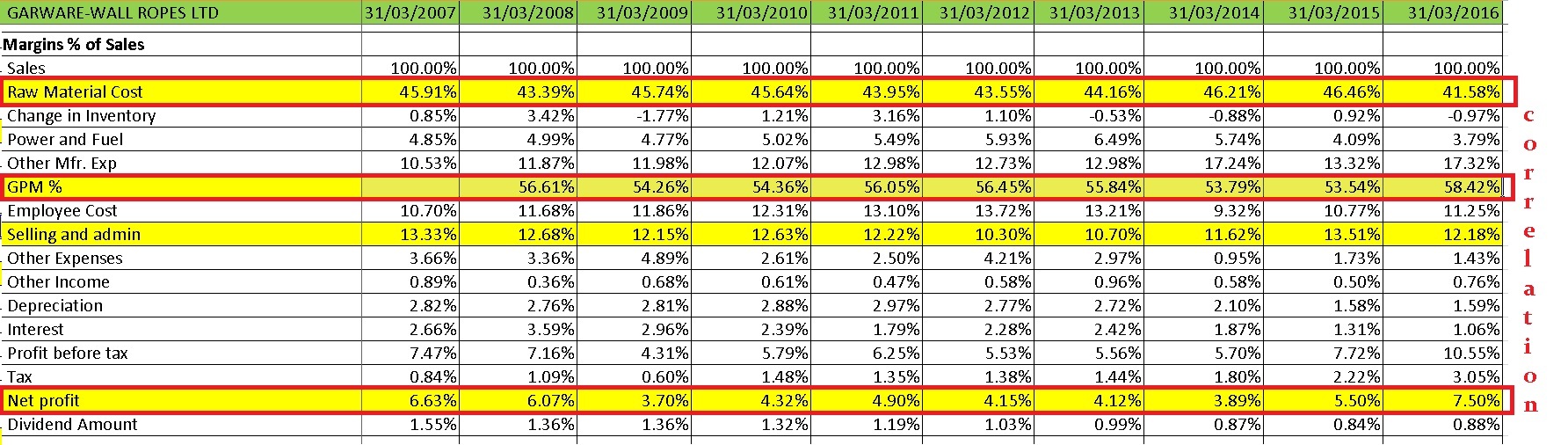

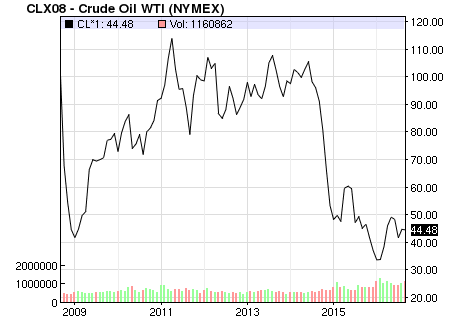

Garware Wall Ropes has been doing well. Margins and Cash Flows have shown very good improvements In FY16. If we see concurrently the absence of topline growth, that might point to a direct correlation with crude for the 2-3% improvement in margins in FY16 (historically at 10-11%). Not sure if we should read more and attribute more to change in higher-margin product mix than to crude pricing - those investing/tracking Garware should be able to throw more light.

The slightly dated Technical Textiles Baseline Survey 2014 (posted in Shiva Tex Yarn thread) referred to by Tushar

@basumallick/@ashwinidamani/@aveekmitra

I don’t know this business. Had a quick look through the thread.

Can certainly see it’s one of those diligent, efficient businesses, run very well. However can’t expect big margin variance to historical 10-11% levels on a sustained basis. Any segments which are non-commoditised?

Donald, thank you for moving the post here. There is definitely some migration to higher margin products based on a recent detailed report by ICRA on Garware Wall Ropes. Please see the report here: http://www.icra.in/Files/Reports/Rationale/Garware-Wall%20%20-R-14072016.pdf

The report has good insights in almost every paragraph, so I refrain from quoting any sections and invite you to read it in entirety.

Thanks Tushar for the report.

It does provide some more details on value-additive segments.

But am unwilling to read too much into it, because the contribution from these segments must be pretty small presently - else the needle would have moved much more.

The report stresses a lot (in tone) on value-additive migration and under-emphasises crude benefits (given the extent of the fall in 2016) being the needle mover is a first-cut reaction. The other aspect we need to think about - slightly over 50% of the business has this characteristic whereas 46% (Exports) they are needing to pass on the benefits.

Need to chew more on this. Tracking company performance will tell us more.

Hoping old hands will throw some insights.

From my analysis of the financials, it seems to me that the company is able to retain some benefits of crude price action, but not entirely. In that sense, the realizations drop, but not to the entire extent of the crude price fall. How this works on the other way around i.e. when the crude price rises is something we can ascertain only if the company were to so clarify or when the event actually takes place.

The company has indicated somewhere that their sales in India are expanding, whereas exports are somewhat stagnant on account of global conditions. Personally, I am always positive on any company that manages to do well vide Indian operations because I believe the Indian consumption story is far stronger than the global demand scenario.

I realize most of my above points are general in nature without any concrete data to back it up, so inputs from others would definitely be more helpful than my superficial comments. I am invested in lower levels though. I wrote to the company once with some queries but received no response.

Hi @Donald The things I understood about Garware are as follows

The quality management system of the company is certified as per ISO 9001:2008 standard by Bureau Veritas Quality International. Its products and solutions comply to all major global quality standards such as BSEN (European standard), EN-ISO (International Standard Organisation), ASTM (American Standards for Testing Methods), JIS (Japanese Standards) and CI (Cordage Institue of USA)., and Russia (I will check which are the other companies globally that have such numerous certifications)

GWRL has a joint market development and license agreement with DSM Dyneema

(Netherlands based) for manufacturing and marketing Plateena products despite being significantly lighter has higher strenth than Steel (Dyneema has been termed as World’s Strongest Fibre). In India Garware is the only player to get this certification, but obviously the competion is with Global players (Let me check which other companies have Dyneema association)

Summary

What Changed in the company

GARWARE WALL ROPES TRADED AT RS. 520/- SHARE. with this one year the stock moved up fastly. at 520/- IS THERE ANY MARGIN OF SAFETY.

This has been the Gross Margin Profile of the company for the past decade. (Source : MorningStar website)

Since then though Crude has fallen, Garware has only strengthened its margins

The point I am trying to make is, Garware is not just a beneficary of Crude Oil Fall.

The new management seems to have focussed on higher value addition products. At 50% Gross Margins, and no close competitor in India, there is something really special that is going on behind the scenes.

Disclosure - Have been invested in Garware for more than 6 months now and forms 5% of my portfolio

Thanks Ashwini for sharing more insights, esp the gross margin migration up in last 5 yrs, and international standing. Am still qualifying, and not made any real effort to understand,so bear with my basic questions:

Travelling till 30th. Will revert back post that.

Need to chew on a few things -

@Donald Vayu took over in 2011…It took 5 years since then and company has been consistently performing since then

So he was aged 24 when he joined Garware on the shopfloor. He mentions that company was going through a tough time during that stage, with many competitors selling at below cost.

Let me read back from 1996 and get back to you

Ok, right.

So the comment “When Vayu came back in 1996 ??..immediately went out in market …touched base with customers” …

He was an understudy, and learning the ropes from 1996-2011 (15 years), or?

Excerpts from Annual Report of 2012 (The First year when Vayu took over)

The application based value added solutions added by the company are as follows. Most of these solutions

Speed up the operations

Reduce Recurring Costs

Provide Higher strength with Lower weight, or

Provide Longer durability

GARFIL STAR

Used for trawling. Offers high tenacity and strength with lower weight and diameter. The customers vessel moves faster and consumes less fuel, the net gets opened wider and more fish gets caught. e net also has longer life. **This offering was however more a star performer during high fuel costs era

ROCKY

A netting developed for sea beds with rocky bottom, which can withstand harsh environments

SAPPHIRE ULTRA CORE

Addresses the need for protection from Sharks and sea lions, which bite into valuable fish. The company did a detailed video surveilance of predator habits and then prepared a unique net , which is cut resistant , stiff yet not rigid, easy to use.

PLATEENA

Conventionally steel wire ropes were used in trawl winches. The reopes used to be heavy (450 Kg), and difficult to handle, plus due to constant water exposure they used to get corroded fast and thus had to be greased frequently. This involved heavy labou and cost and also left oil traces in the water.

Plateena is as strong as steel, are easy to handle, require no oiling or greasing and can be easily replaced. Even the Indian Navy is testing Plateena to replace concentional polypropelene ropes.

Cost of Nets is 2-3% of overall costs, but its the most critical part of the aquaculture industry