Let’s see it pans out in the coming few seasons. Country liquour is a very local phenomenon. Off late there has been an increase in excise collections in Maharashtra and severe penalties in the unorganized sector for selling illegally.

Some fieldwork from my side indicates that several wine shops have also put up boards indicating that they also sell IMIL. There is not much difference in the basic ingredients of IMFL and IMIL except flavour and colour but there is a significant cost difference. That said raw material volatility is very high making it difficult to predict margins.

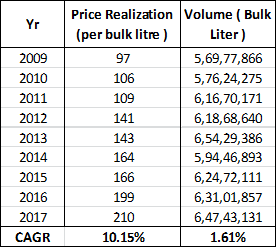

Some quantitative data on price realizations and sales volume

Source : ARs

In 2017, the price per bulk liter was Rs 210, which translates to Rs 38 per quarter ( 180 ml ). This indicates the price disparity of country liquor wrt to IMFL

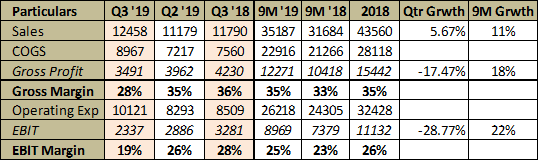

Mixed set of numbers from GM, Sales are up by 5.67% for the quarter and 11% for the 9M however raw material fluctuations has decreased the gross margin for the quarter to 28% from 36%. At a 9M level growth numbers are good and remain more than satisfactory. A Business as Usual kind of result.

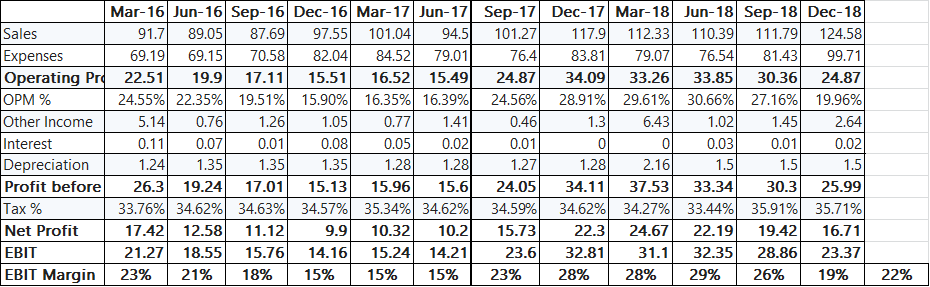

The average EBIT margin is 22% for the last 12 qtrs , so hopefully margins will revert to that in the near term.

(2018 investments is including 45Cr of property investment i.e 107Cr + 45Cr)

As per the management, the non-current investments is the quarters they have been building for the employees. Eventhough it is meant as quarters, it is built as proper residential 1-2 bedroom flats. The company is only in Maharashtra and the chances of getting licenses in other states is nil. There are uncertainties, if the changing governmnts bring an alcohol ban, the company needs a back up, and this investments in flats will server the purpose at any such adverse time.

There are around 170 employees. So if i consider around 1Cr to such a flat in that location, it amounts up to 150Crs. In 2018, they moved part of this to property investments due to the LTCG tax.

He said the quarters has been almost complete so from next year onwards they will start giving back more dividends to the shareholders.

Couple of questions arise in my mind:

Is this investments and quarters real? Can anyone in nearby locations verify this. I could not connect to any body who can give info on this.

If it is real and there is such a quarters so on, has the management really spent this much amount - 150Cr - this is almost 50% of the BS - in building it? Could this be a vehicle to channel funds off?

Some of the excess cash the co generates is used to accumulate real estate and the rest sits on the balance sheet. They do pay dividends as well but not as much as one would have liked. This is a long term issue and one will have to live with it if invested. The co is well run and has a good stable business.

As pointed out its Thane based so licenses in other states remain slim however alcohol ban while in the realm of possibility remains distant due to the excise duty collected from it which runs into substantial amounts.

As far as I understand, GMB is an excellent cash-and-carry with a wide moat (A near monopoly in Maharashtra). But the only negative I see in the company is the proverbial glass ceiling. Aren’t you worried that after a while, they’ll get too big and will run out of places to invest? I understand that this eventually happens with every company, but GMB operating largely in a single state makes it all the more quicker.

Yes I am not contesting the moat and the other points you said.

My only worry at this point is whether this investments if real, the amounts in the BS is really invested in that property/building. If it is not, that is a huge red flag, the management is siphoning off funds. No moat or other benefits can compensate it.

Just thinking aloud. Trying to verify whether what the company claims is right.

It takes a certain sort of promoter to do a certain sort of business. Liquor, Gems & Jewellery, Casino, Infra, Power etc. I have noticed don’t make much money for their shareholders and even when they do, there is many a slip. Real-estate investments of such scale aren’t going to be EPS accretive and I think should be seen worse than hoarding cash IMHO. Despite this GM Breweries has a RoE of 28% or so (on average 25% last 5 years) which is impressive but in businesses like these, promoters and shareholders interests are going to be at odds in the long run and chances of value destruction via diworsification and siphoning are high.

Just Google it mate, you get the answer. Presently, Alcohol / Liquor is banned in Bihar, Gujarat (license based easy availability) and a few north eastern states. Nevertheless, availability is there unofficially. Even in Maharashtra, liquor is banned in Wardha and Chandrapur districts.

Good catch and thanks for sharing the same.

If true, certainly raises questions like below:

It may not take 4 years from 2014-2018 years to build 170 flats, assuming they are in Thane and the land is owned by GM Breweries. Are they completed yet? Has anyone seen them? And also it may not cost 150 crores for simple 1-2 bhk type apartments, as construction costs may not be that high.

How many of the 170 employees are full-time and contract labor? Are the contract labor also getting flats?

Is there a precedent for promoter building flats for employees in recent years? Either in liquor or other industries?

The management could decide to invest in real estate, no harm in that.

Atleast they should be more clear and transparent about the same, to give confidence to stakeholders.

But they don’t seem to care much, as this issue has been raised in May-2014 by Abhishek and Vikas in 2016, earlier in this thread.

So its your choice as an investor, either you live with it or move on to better things.

It is not true that in India you can only produce ENA from molasses. Now, most of the Alcohol manufacturers has shifted to Grain based alcohol.

Here is a line:

Globus Spirits is grain based neutral alcohol manufacturer. We do not make any alcohol from molasses and all of our products - the neutral alcohol - are sold to customers who have a demand for grain neutral alcohol.

If interested then find out who are producing from grain based neutral alcohol and who are making from molasses.

Result Update: YoY quarterly

Sales: 43.7 Cr vs 42 Cr,

EPS: 13.3 vs 16.8

Cost of Raw Material: 80 vs 68.4 Cr YoY.

So, YoY Raw material price is higher.

Sales only 4% up which is not a good sign I think. The growth it was showing is not there anyone!

Any competitor taken the market from it?

Who is that?

In India about 350 distillery units of 4.0 billion litres & 100 distillery units of 1.8 billion litres are molasses & grain based respectively. Potatoes , Rice , Maize , Malt , Wheat , Barley , Sugarcane & Sugarbeet are various raw materials used in grain based distilleries.