Disappointing set of numbers; while the company has managed to reduce its loss this qtr, I was hopingfor asmall profit.

Plus, I did not like the promoter selling just before the results.

Disc: invested, but now re-evaluating.

Disappointing set of numbers; while the company has managed to reduce its loss this qtr, I was hopingfor asmall profit.

Plus, I did not like the promoter selling just before the results.

Disc: invested, but now re-evaluating.

There is a huge fall in the stock price recently. What is the reason? the profit for this company always behaved in a cyclical way…How will the company perform in the future quarters. Experts can you please give your views.

Disc: I do not hold but want to invest in Freshtrop

If you see the historical values the next 2 quarters are going to be very good quarters.

Company debt levels are coming down and considering their products always attain some premium because of high quality, one can stay invested. May be the news rains spoiling some crops is behind the stock down move.

My views are biased and invested since 31 levels and will increase the holding in a staggered manner.

Hi Chaitu: Yes. Unseasonal rainfall has had an impact. But there are other reasons too. Please find mgmt. update on this:

From BSE website: dated 21/04/2015

“Freshtrop Fruits Ltd has informed BSE that the unseasonal rainfall has affected the grape export business of the Company. The total exports of grapes for the season would be 30 to 35% less than last year but there is a significant improvement in the selling price. The unseasonal rainfall will have not any significant effect on the profit of the Company for 2014-15. The effect will be there in Q1 of 2015-16 but this could be mitigated by better price realization.”

I looked at this stock a couple of months back and was put-off by the high valuations. In the recent carnage, this stock has corrected by ~60%(from a high of 207 to CMP of 88 now).

Reasons Could be:

1). Promoter selling just before the results were declared!

2). Euro depreciation Vs INR in the last 2-3 months - This will result in lower realisations.

3). Unseasonal rains’ impact on grape to the extent of 30-35% as the management has indicated. (Here too the mgmt indicates - the selling price realisation is better.)

In one of the discussion points, someone mentioned grapes contributing ~80% of the total exports. (am not sure about this)

Chaitu/Ravjit/Ayush/Nikhil/Shak:

I have a couple of queries.

1). By any chance if any of you are still holding this, what is contribution of grapes to the total exports?

2). Management indicates food processing unit has turned around. Do they have any branded juice available/do they just sell for the biggies like ITC?

From my side am trying to find out more on this.

Known risks:

1). Low ROE/ROCE business.2. Seasonality and affected by nature’s vagaries.

Thanks,

Ravi S

Disc: No holdings. Evaluating if the recent correction provides an investment opportunity.

Ravi, if you check the AR for last year, you will see that exports of grapes to EU alone accounted for 73% of the total revenue, while food processing was 20%. Remaining 7% of revenue would be divided between grape exports to other major regions such as Middle East, and other fruits such as pomegranates and perhaps mango.

As for my holding, I hold slightly more than a tracker position on this; sold off most of my holdings around last quarter results. Recently, the stock price volatility and movement is scaring me off a little bit to reenter.

On the company disclosure, I think we already clocked eps of 5.2 in 9 months, so year end eps would be between 7-8. But the scary bit Q1 2015-16, which is their biggest quarter. Last year they had 5.6 eps in the qtr, not sure what will be a safe estimate for the next qtr.

@nikhil And now it is available at 61 @ a Mcap of 74 crores. With fixed assets at ~ 42 cr and with some cash in the books, the MoS has improved I feel(They have enough cash on books to service interest obligations for the next 2 yrs) -> This should give an investor some cause for comfort.

Yes they are going to have a difficult quarter, but not as bad as what the stock price suggests.

I have initiated a small position(~1% of my pf) @57 to track this stock. Might book out if I come across more risks vis-a-vis opportunities.

Thanks,

Ravi.S

Disc - My views may be biased as I am talking about this from a buyer’s perspective with a small tracking position. Please do your due-diligience.

Hi Ravi,

The last qtr results were really disappointing (even after the pre announcement) imho, and the way the stock has been hitting LC also does not do my confidence any good.

I did some very crude calculations, in worst case, Q4 FY 15 numbers, we saw a 20% YOY decline in sales; extrapolating 25% decline YOY for Q1 FY 2016 (the management said that they were really concerned about the numbers in Q1), we arrive at 52Cr (70cr * 0.75). The net margin numbers for Q4 2015 were an abysmal 3%, while historically it has been between 8-12% for Q1 and Q4; assuming a 5% net margin for this qtr, we get 2.6 cr in NI, or Rs. 2 in EPS. Assuming 2nd and 3rd quarter cancel each other out, and Q4 2016 will match 2015 qtr (worst case), we get EPS of Rs 1, and full year EPS of Rs 3. Assuming a good Q4, I take the numbers from Q4 2014, which gives an EPS of Rs. 2 for the qtr, and full year EPS of Rs. 4. So all in all, the next year EPS numbers could be between 3-4 under pessimistic conditions.

The above numbers paint pretty dismal picture. But again caveat remains, that these are extremely crude approximations, and the margins/sales of the firm has tended to vary greatly. Second, it also does not expect the food processing business to be profitable and contribute meaningfully to the bottomline.

What do you think?

PS: hold slightly more than tracking position in the stock (~1% of pf)

“I did some very crude calculations, in worst case, Q4 FY 15 numbers, we saw a 20% YOY decline in sales; extrapolating 25% decline YOY for Q1 FY 2016 (the management said that they were really concerned about the numbers in Q1), we arrive at 52Cr (70cr * 0.75). The net margin numbers for Q4 2015 were an abysmal 3%, while historically it has been between 8-12% for Q1 and Q4; assuming a 5% net margin for this qtr, we get 2.6 cr in NI, or Rs. 2 in EPS. Assuming 2nd and 3rd quarter cancel each other out, and Q4 2016 will match 2015 qtr (worst case), we get EPS of Rs 1, and full year EPS of Rs 3. Assuming a good Q4, I take the numbers from Q4 2014, which gives an EPS of Rs. 2 for the qtr, and full year EPS of Rs. 4. So all in all, the next year EPS numbers could be between 3-4 under pessimistic conditions.”

I concur with most of the approximations here. This was partially my thinking behind entering this stock. Even in a worst case scenario, the company should do an EPS of ~ Rs 3-3.5. Going by that #, the big correction from 200 to 60 has most of the bad news in the price.

The big risk - As you have mentioned these are crude approximations. 1. Can we look at fruit export #s by India to EU in the last 2 months?(approximate the company’s market share to arrive at a ball park sales) - In the other forum(avanti feeds), someone had attempted at a similar analysis for Prawn Imports by US.

2. Write to the company to understand to understand the impact?(depends on if the company is investor friendly enuf to respond to us)

3. 80% of the company’s topline comes from Grapes - someone from Maharastra(nashik,& sangli particularly) can help us understand the real impact on Grapes cultivation? - Dont know how to find this out

If we have some answers to the above questions, we will be able to build conviction on this stock to add more. As of now, to be honest, I am not able to build any opinion on this apart from the gut feeling that this is probably cheap. (but just going by gut feeling is a dangerous investing habit  )

)

I will try to do some data mining on point # 1, if you think of anyother points which can help us build conviction on this, please share.

Thanks,

Ravi S

Just throwing out some data: Needs further analysis-

Grape Exports by India till last year: Error Page

Grapes Price realisations in Europe: Check the url below

2014,17th week - http://www.freshfruitportal.com/wp-content/uploads/2014/04/week-17.pdf

2015,17th week - http://www.freshfruitportal.com/wp-content/uploads/2015/04/week-17.pdf

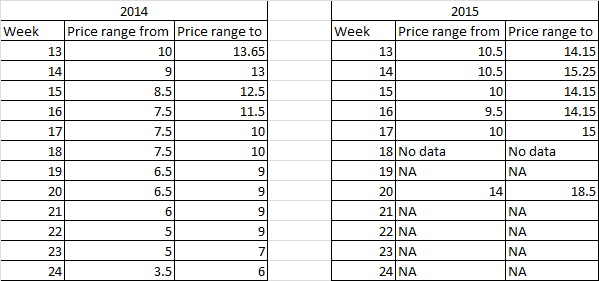

2014 2015

Week Price range from Price range to Week Price range from Price range to

13 10 13.65 13 10.5 14.15

14 9 13 14 10.5 15.25

15 8.5 12.5 15 10 14.15

16 7.5 11.5 16 9.5 14.15

17 7.5 10 17 10 15

18 7.5 10 18 No data No data

19 6.5 9 19 NA NA

20 6.5 9 20 14 18.5

21 6 9 21 NA NA

22 5 9 22 NA NA

23 5 7 23 NA NA

24 3.5 6 24 NA NA

Note - All prices are in Euros, and this data is specific for Europe.

The above table captures the data for grapes price realisations for last year vs this year for the Indian grape variety “Thomsons Table Grapes”. Yes this indicates that the price realisations were better.

But to me again this raises 2 questions:

More data = more questions ![]()

Thanks,

Ravi S

Rough estimates here again, using your data: average price hike from your tables is ~20%; Company has guided for 30% less sales by volume. This means 0.7*1.2 = 0.84 times the last years’ sales figures, or 15% decline in sales for the quarter. Higher prices paid to the farmer translates into lower margins (5% if we compare against last quarter). Doing this, we end up with 59 Cr sales, 2.9 Cr in NI, and ~ 2.5 in EPS for this quarter. This means the base case will be around 3.5-4 for full year EPS for this year. So currently it is between 15-18x PE.

I think you are right to point out, that along with volumes it will also be a margins game in the end. If we assume a better margin for the company at say 10%, the EPS for next quarter jumps to 5, and full year estimates will be closer to 7ish.

Anyhow, EPS of 3-4 is big drop from the my original investment estimates for the eps of 9ish for 2015 (clearly I was way off) sometime late last year.

Hi @ravimba31,

Very good data digging! In the first link the year mentioned is the calendar year or financial year?

Also, in the discussion I’m seeing that there is a lot of focus on estimating the EPS. I think thats futile (the price decline is surely showing that the earnings would have been hit). The focus on such companies (especially after corrections like this) should be - was this a temporary problem (just a bad season) and will the competitive advantage remain?

Regards,

Ayush

Hi @ayushmit:

Thank you. The link which has weekly price realisation trends for grapes is for Calendar year, where as the link which has annual grapes exports is based on FY.

I got a response from the website administrator on what NA means (for a few weeks): Apparently, NA in the table means, Indian grapes data was not available for that week(-> Grapes not available in the market for price data).

Thanks,

Ravi S

Ravi, Ayush,

Found this data site:

https://www.zauba.com/exportanalysis-grapes-report.html

See what you make of it. The actual numbers might be a bit off, but i guess the trend is quite clear: grape exports completely collapsed this year, especially in this quarter in April. Clearly, we should not expect great things from the company for this quarter.

To Ayush’s point, on how does this impact business competitiveness, the naive me says that typically the market leader should benefit in the longer run and capture market share as smaller players get squeezed out. But then that is taking too simplistic view of things.

Freshtrop Fruits Results update:

Freshtrop Fruits’ bottomline #s look optically better than even our conservative estimates.

Topline decreased a good 38% down to 40.09 crores(q1,fy 2016) from 65.46(q1,fy 2015) crores.

PAT decline was just 7%, to 6.33 crores(q1,fy 2016) from 6.82(q1,fy 2015) crores.

Bottomline performance was boosted mainly due to contribution of other income(1.83 crores).

I liked the segment wise performance however: Looks like their food processing segments has turned around this quarter. For q2 and q3 food processing segment will be the key IMHO.

Thanks,

Ravi S

Disc: Have a small position in FF.

Looks like the tread has gone inactive during the key months relevant for grapes.

Some interesting news flow/articles worth to ponder upon.

Are Indian Grapes in spotlight?

Disc: Invested

Also,

Un-seasonal rains?

(http://www.freshplaza.com/article/154490/India-Grapes-and-mangoes-marginally-affected-by-hailstorms)

http://www.thehindubusinessline.com/economy/agri-business/maharashtra-farmers-use-new-methods-to-save-horticulture-crops-from-hailstorms/article8310051.ece

Weather boon: Country’s grape exports set to double

Very useful discussion above. Wonder how much of a threat Brexit would be to this company.

Freshtrop’s major clientelle lies in the UK and Europe. Thes include ASDA, Tesco, Marks & Spencer and Univeg fresh food chains ,The Delhaize Group and the Carrefour Group, Lidl, Aldi and the Rewe Group,Albert Heijn BV, Schuitema NV and Olympic Fruit,etc.

I think this company will be majorly hit in case Brexit happens and will be a major benefactor in the case Britain decides to remain.

Disc: Taken a small position. Waiting till 24th June.

Can you please explain the reasoning behind the company being majorly hit in case of Brexit ?

Brexit should lead to a decline in the pound and the euro (estimates vary by how much, but this is a reasonable assumption). There is also a lot of speculation on inflation growing by up to 4% (http://www.ft.com/fastft/2016/02/08/citi-brexit-could-drive-inflation-up-to-4/) . Most of Freshtrop’s clientele is in the eurozone and the UK. From a purely macroeconomic point of view, would this not imply costlier grapes and pomegranates as euro and UK suppliers would pass on the costs to the consumer.