Thanks a ton for sharing this view.

The key issue is whether NHAI is good debtor. Prof Bakshi says that it has to borrow to pay its interest and principal, and this will worsen with reduced Govt support. A death spiral, in my view.

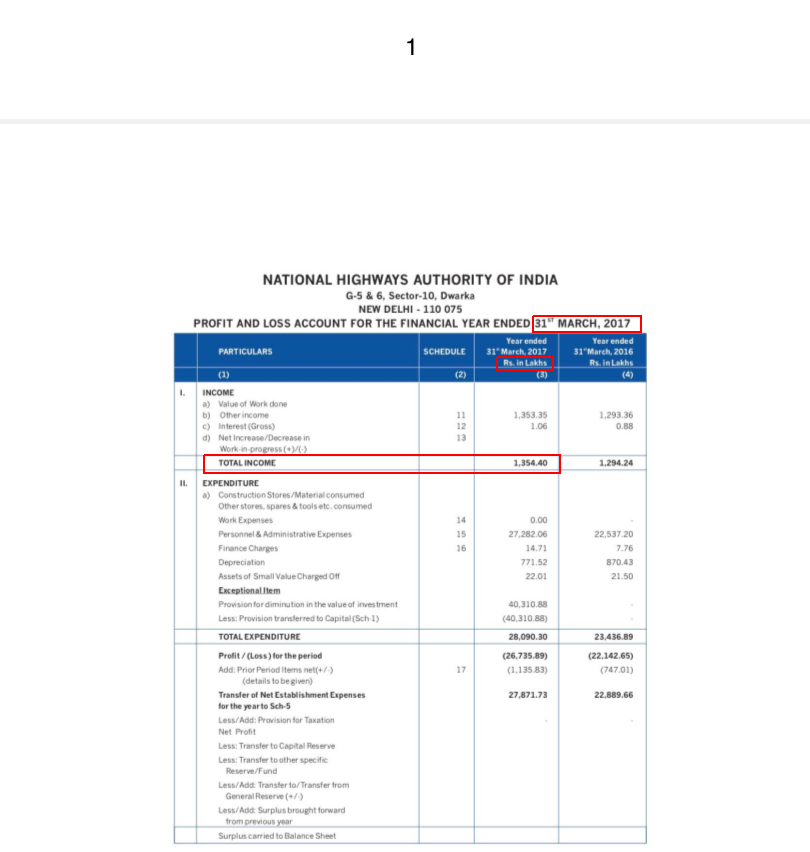

I think the essence of what Deepak is saying is that NHAI collects about Rs 7,000 crores from operations as tolls and this is more than the interest due in FY 17. Principal can always be always be rolled over (aka Govt) and the debt is quasi guaranteed.

In my view these are very tenuous. Take the first, Rs 7,000 crores toll is the gross amount. Cash flow from financing shows the net amount to be Rs 6506 cr. But not all of this is available for interest payments. Operational cash flow sucked about Rs 1932 cr, leaving Rs 3576 cr to deal with interest. Interest paid however was Rs 4068 crores, higher than what it got via tolls net of operational cash outflow. Thus toll collections are not covering interest. Additional funds are needed and provided by the Govt / market to clear interest.

Now this was with an average debt of Rs 50,000 crores. The debt now is about Rs 150,000 cr, which means an interest of Rs 12,000 cr at the same rates. Now we don’t know what the net toll collections are, but it is unlikely it would have gone up in the same proportion because toll takes a longer time to ramp up than debt ramp up. Thus it is likely that toll collections are yet not enough to cover interest payments after operating cash outflow.

On the assumption that principal can be continuously rolled over, I think Herb Stein’s quote Prof Bakshi put out says it best - “If something cannot go on forever it will end”. I am tempted to think rhyming histories like discom restructuring, where the music does change if not stop.

On the last assumption that the debt is quasi guaranteed, the answer is no. There is no guarantee of the Govt in NHAI’s borrowings including the famed 54EC bonds. We are conditioned to think that way because of Govt association with NHAI and it obviously suits the Govt and NHAI to encourage it.

There is also an inadvertent error in the piece - it says Govt borrowings in FY 17 was 61 lakh crores. That is incorrect, the net borrowings in FY 17 were about 4.268 lakh crores (Source: RBI). So if the Govt were to assume this debt it would add to more than 35% of its borrowing - can’t even think of it!.