look at the state of affairs in mumbai,delhi…there is no place available to even park cars. driving in the traffic is a torment…and we still believe that auto companies are a buy…look around you.for how long can this sustain.

3 Likes

@nikhiu7r

You are correct. That’s why new trend will be UBER, OLA, POOL transport - instead of owning a car!!

Look the recent thought http://techcircle.vccircle.com/2017/02/07/exclusive-uber-to-take-on-ola-shuttle-soon-with-bus-van-ride-sharing/

Disc- invested in force at 1700 level

I think this concept for uber instead of cars is only for affluent people. For most Indians owning a car is prestigious. That was one of the main reasons nano flopped. Owning it meant a poor man’s car. This is the reason Tata brand consultant gave.

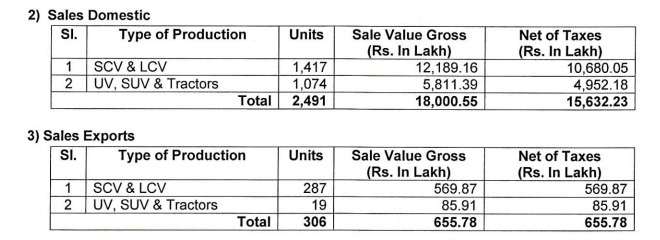

Got a basic question. From the sales figure company submits every month, which figures flows to the topline - gross number or the net number? i.e. 180 + 65 cr or 156 + 65 cr? To me, looks like it is the net amount, but just want to confirm.

Just doing this exercise to find out the contribution of sub-contracting business to automobile business. HDFC Securities reports a ratio of 37:63 for 2017.

The annual report has both gross and net figures.

Net numbers will go to balance sheet . Gross are inclusive of taxes which have to paid off .

Pls post your findings on the breakdown of businesses , company is not reporting differently

Just a few pointers from my side -

The board of directors seems to be tightly knit with the likes of Mr Pawar and Mr Mehta and Vinay Kothari. Mr Pawar is the younger sibling of Sharad Pawar, Sudhir Mehta is the son in law of the firodia’s and Vinay Kothari seems to be connected to Sudhir Mehta as well, if you do a quick google search , youll find that Sudhir Mehta and Vinay Kothari are common presence on the board of many other companies

Another thing is that the son in law, Sudhir Mehta and Abhay Firodia, (through an unlisted company) are on the board of an Israeli Irrigation company and they plan to bring this business to India as well. We need to watch out for any sort of capital diversion from force to this business

Besides, Im attaching a word doc with some other significant issues

Fudge.docx (107.4 KB)

6 Likes

What comprises the “other financial asset”, which has gone up from 17 cr last year (March 2016) to 516 cr this year (march 2017)?

Company has raised commercial paper loans and has reinvested that in the market.

@dsaraf Did you find it worth investing?

How serious charges you label on them for all things they have done?

I bought it few days back and added more today.

1 Like

Terrible result by force , is it losing the charm . Pls share your views . I exited 25%of my holding (in force) today.

I believe that these are short-term blips owing to the constraints of the CV industry from BS-III ban and BS-IV implementation from April 01. Moreover, luxury cars are slowly coming back in demand post demonetization.

Ref: Q4 FY17 reports from

Karvy.pdf (320.2 KB)

HDFC.pdf (400.7 KB)

Adding to this there was bound to be a hit on margins because of onset of GST.

All major car makers gave a steep discount to clear the stock in hand.

So mostly it will be a one off case.

1 Like

EPS growth from Karvy report does not appear to be encouraging.

My notes from annual report 2017. I am not compiling the usuals; just pointing some risks, which can be existential for this business. Would like to know thoughts of fellow boarders.

-

FY16-17 was stable with very little growth. Company says it was due to Demo, BS IV, and GST impact, which led to disruption and rhythm of the business. Effected H2 big time.

-

The program for fielding BS VI compliant engines and vehicles for 2020 is strongly underway. Dedicated facilities and fully equipped labs for engine and vehicle development are commissioned and operative. This is enormously challenging but company at the moment is confident of attaining the desired goal.

-

Electrical Vehicles - The company has initiated developments of Electrical vehicles. The first Electric Traveller is undergoing detailed evaluation and trials. The company has formulated a dedicated section for electric vehicle engineering to cover all aspects such as drive systems electronic vehicles and battery management systems, battery engineering and chemistry, installation engineering on vehicles and management of auxiliaries and peripherals, on a variety of vehicles. The focus of the company on electro mobility, remains the same as the company’s current product profile. It is expected that over the next 10 years, there will be a significant transition to electro mobility. Success of Electric vehicles depends on availability of batteries, with cost per KwH at a level which can compete with fossil fuels. It is expected that by 2020 there will be a much stronger position and possibility, for full electric vehicles.

-

The continued acceptance of diesel fuel for light commercial vehicles and for cars in under pressure, whereas for heavy commercial vehicles at the moment diesel seems to be a stable bet. This happened post controversial case against Volkswagen. In spite of promulgating the BS VI standards in India, for which FM is striving, a global anti-diesel opinion may build up. This can have very serious effects on the industry and FM won’t be any exception. We strongly believe in the virtue of diesel and also understand that at BS IV, and certainly at BS VI level, the quality of air exhausted from the engine will be superior to the quality of air ingested. Nevertheless the environmentalists who influence public opinion, as also other less than well informed opinion makers - hold a bias against diesel, which could be harmful.

-

GST - Discrimination against vehicles with seating capacity between 9-13 attracts 43% tax due to a penal surcharge. Rest all (1-8, <13) just attracts 28%. This is an illogical anomaly and effects FM significantly in a negative manner. Industry has assumed this would go with onset of GST, but has not happened. There would be significant improvement if regulatory issues arising from GST rate on the Harmonised Tariff Code Item 8702 is simplified, as also if such vehicles are facilitated to operate freely on a pan India basis, there is enough pent up demand, and a crying need to do this.

The speed of change in regard to Electro mobility and the developing resistance to diesel fuel are twin technical challenges which threaten to bring about far reaching changes in the automobile industry.

1. Given these “existential” threats, how would one rate FM as an investment?

2. Will FM be able to mould itself with developments in Electro mobility?

3. Regarding diesel fuel, with the onset of BS VI, would the pollution rhetoric go away?

3 Likes

in their latest Annual Report, they’ve raised money through CP’s and have invested the same under "other deposits."

Any guesses?

Force Motors FY17 AGM – Key Discussion Points

Highlights of Chairman’s Speech (Mr. Abhay Firodiya)

On BS VI

• All over the world, each phase is given a 5 yrs time frame for transition

• GOI has directed all automobile manufacturers to transition directly to BS VI from BS IV currently. i.e we are working towards taking a 10 yr leap in 3.5 to 4 yrs by April 2020

• Transition from BS IV to BSVI is going to be a challenge for the entire industry; Force Motors among best prepared to embrace this change

On Electrical Vehicles (EV)

• Auto Industry is staring at a revolutionary change in the coming decade

• Electrical batteries have to increase storage capacity and reduce cost to become viable

• Today, an Electrical battery that may be costing 3.5 euros, will be on par with fossil fuel vehicle when the price comes down to 2.5 euros. At 2 euros, this would be more efficient than Pertrol/Diesel

• An EV has 10% of the parts of a current vehicle and will require 1% of current cost of maintenance

• EV are going to pose a serious challenge to auto ancillaries – they will have to look for new avenues to do business in order to survive

• The entire ecosystem of service centres, garages etc. is likely to be disrupted with onset of EV

• Force Motors in fairly advanced stages on development of EV’s

• Excellent in-house team doing R&D in collaboration with the world’s best brains

• Target spending 7-8% of sales on R&D and confident of having EV for all it’s present line-up along with future launches

• Force Motors already has a fully functional vehicle doing trials (This came as a pleasant surprise!)

General

• FY17 sales were impacted by three-way blow –

a) Demonetization – in-ability of customers to provide for down-payment which was typically done is cash

b) Transition from BS III to BS IV – GOI had earlier given one month’s time to liquidate BS III inventory, however SC ruling on 27th March 2017 struck down this window

c) Diesel Engine > 2,000 cc ban by SC

• Company has made repeated representations to various Govt. bodies to remove the anomaly of higher incidence of taxation on vehicles with seating capacity 9-13 (which accounts for 50% of their sales)

• Company looking to export the balance inventory of BS III vehicles to countries where it is still allowed. Clearing the inventory likely to take a few quarters

Highlights of Q&A

• Company has plans of spending around Rs. 1,000 cr on capex over next 2-3 yrs; renovation and upgradation of all plants to be done

• A completely new platform for the Traveller is under development and should be ready by 2020 and for Trax by mid 2018

• Outlook for contract business from Mercedes & BMW is promising given under penetration of luxury car market in India. Reasonable possibility of Force Motors increasing the scope of business with these companies with time

• On 12th Sept 2017, Force Motors signed a non-binding Term Sheet with Rolls –Royce Power Systems AG to produce engines for Power generation and railways

o Deal likely to be concluded by end of 2017 or Q1 2018

o Company to jointly setup plant in Chakan for manufacturing

o News reports suggest that company will jointly invest Rs. 300 cr to setup the plant, to hold 51% stake in JV (The company did not confirm these numbers)

o After tie-ups with BMW & Mercedes, addition of Rolls-Royce to portfolio is feather in the crown

• Company has no plans to renew corporate deposits and shall be paying them back

o Management said that they are in no need of money and prefer to stay debt free as long as possible

• Focus on R&D will enable the company to be ready when disruptions like electric vehicles, BS VI transition come

• No plans of Bonus or share split. Dividend unlikely to go up significantly in the coming years

Disclosure: I am invested in Force Motors and my views could be positively biased. The above points are to the best of my understanding

8 Likes

Thanks for sharing. I have only one question - What will happen to their

business as BMW and Mercedes will gradually shift to electric vehicles.

They will loose all of internal combustion engine manufacturing business

of these brands within few years.

5 Likes

The management did not explicitly speak on this, but here is my sense -

Partnerships with BMW and Mercedes are long term relationships involving significant capital expenditure in plant setups. It is very unlikely that they will dump FM. FM may well end up playing a role in contract manufacturing of some other system that may be required for electric vehicles. The MD did hint that as the relation with these companies matures, FM may get incremental business. Let’s wait to see how things evolve in this space!

1 Like