Cidade De Goa is a 5 star luxury resort owned by Fomento Resorts & Hotels ( owned by the Tiblo family ) is aptly called "Goa in a resort ). I have been there multiple times and it is a great property on the Vainguinim beach in Dona Paula. Dona Paula is the “posh area” of Goa and is very near the commercial capital of Goa - Panjim. The hotel has a lot of history attached to it ( it was designed by Charles Correa the architect of Navi Mumbai) going back to the time goa was under Portuguese rule but since its unrelated to the main business i wont get into it. In March 2016 the Supreme court dismissed a case against Fomento and upheld the validity of the construction of 54 rooms that was supposed to be irregular.

Coming back, the resort consists of 207 rooms and lies bang on the banks of the vainguinim beach. A part of the resort falls under the CRZ II zone ( http://www.cidadedegoa.com/downloads/MOEF-clearance.pdf) which requires not only environmental clearances but also coastal regulation clearances after you have purchased the beach facing land ( which fomento procured sometime in the 1980’s ). In short, it is next to impossible replicate a resort like cidade de goa in the heat of goa ( even if you have a great liasoning team procuring land is near impossible and even if you find one the costs are prohibitive ). This creates an unassailable moat.

Cidade has the environmental clearances and the CRZ clearances and the land not only for the the current resort but also Cidade 2 ( 300 rooms) thats being constructed there and a 5 star 32 room resort in Aravli Sindhudurg ( the land is on a 90 yr lease from MTDC agreement signed in 2005). However, the main business is on Vainguinim beach.

To be sure its not the only one with access to vainguinim beach. There are some hotels within hailing distance of the beach but Cidade is the largest one in that area by far and the kind of customers it attracts dont mind paying northwards of 12k per night. Its ARR is twice that of its nearest competitor. While others charge between 4k to 6k Cidade charges 12k+. Another non replicable advantage is size. Its a property that will eventually have 507 rooms ( 207 + 300 ) which makes it especially suitable for hosting weddings and other destination events which is one of the main revenue pullers judging by its AR.

and of course its Goa. You cant replicate Goa can you now

I’ll keep the thread running with more info on the financial numbers and other tourism statistics.

Hi,

Has this company been doing capex for past 2-3 years? Any idea, how has demonetisation impacted their hotel’ business? Cidade Daman and Cidade Diu are two other resorts. Are they also listed under Fomento?

If so, how are they as property or business?

If I understand it correctly the opportunity size is small here. IMHO there are slim chances of them showing good growth for a long time due to the opportunity size

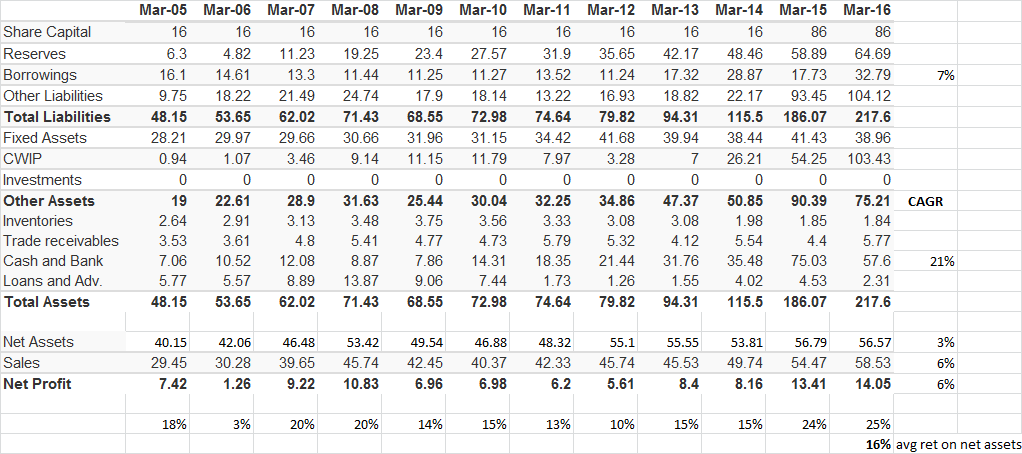

The ongoing capex is evident from the CWIP numbers that have increased from 26cr in 14 to 103cr in '16. Also they have stated in the AR about the ongoing construction works in Aravali and Cidade II

I have no clue about the long term or the short term impact of demonetization

207 rooms got in a revenue of about 58.53 cr in 2016 i.e Rs 28,27,536 per room per year. Ideally a room should have gotten in a revenue of 365*Rs 10,000 per night ( Rs 36,50,000 ) which implies that the occupancy rate is about 77% in the current Cidade. So 23% rooms are going unoccupied. So there is a possibility of increasing the revenue by 17cr if these 23% are put to use somehow. Now there are another 332 rooms in the offing ( 300 rooms in Cidade 2 and 32 in Aravali ). Assuming that the occupancy in these new projects will also be in the region of 75% then we are looking at an additional revenue of 91 cr @75% & 121 crs @100%. That implies a revenue of 91cr+59 cr = 150 crores an increase slightly more than 250% over current revenue levels. I am not even considering the pricing power.

first off the cash balance on hand has grown at a CAGR of 21% over 11 yrs. A sure shot sign that the company is generating cash.

Secondaly , Net assets ( assets net of cash, investments and CWIP ) have grown at 3%, which is good considering that sales and net profit have grown at 6% over the same period, indicating that the company is able to grow sales & profits with little reinvestment in assets.

The return on net assets ( assets net of cash, investments and CWIP ) is 24%-25% since the last two years and is 16% on an average.

The Debt on the books is almost interest free. The only concern is the preference share liability where the dividend is Rs 7.5 per year.

All in all i think the financials are not bad and while i dont think its going to be a multibagger , it is likely not going to lose money for shareholders over time

While there are a lot of positives in my opinion - there are some key risks attached to the stock as well. Here are the ones that one should look out for -

a - The promoters are the Timblo family - in the news for their mining activities and have received some bad press over time. The family holds 75% of the equity. It is also one of the highest tax payers in State of Goa.

b - the business operations are solely dependent upon the ebb & flow in goa tourism - any adverse impact on tourism will impact their business as well

c - the investment thesis is dependent upon the successful opening of Cidade 2 & Aravali resorts. So one should do their own due diligence and get clarity on that.

d - In my opinion, the occupancy rates vary between 70% to 80%. While the AR doesn’t have any information on that, any variation in the occupancy rates will certainly impact the business adversely.

e - Competition. Tourism is one of the main revenue pullers in Goa and there are several five-star hotels competing for the same customers. There is an ever present threat of new entrants with greater resources at their disposal and innovative business models. A case in point is Airbnb.

Disclosure : I am invested (about 9% of my portfolio)

Bad press was about Radha Timblo. Although they may all be related in some way, they are different families when it comes to business. See the clarification part in below link.

Even I was interested earlier but this time I purpose fully stayed in the property for three nights and it was way below even 3 star standards on all counts and 70% occupancy in peak dec. I enquires about th new construction and nothing was happening as mentioned in aṛ for the 300 room new hotel secondly they were earlier trying to delist also now withdrawn because of sebi regulations I would better wait and watch. Corporate governance will be an issue with this promoter IMHO

REGARDS

discl invested earlier but sold as of now.

any new update on the same? the company took postal ballot approval to Raise Rs.750cr in March 2017. FY 17 numbers looks good and the CWIP stands now at 166cr. Net debt still at Rs.33cr.

Also can anyone share more details about the family? Both Anju and Auduth Timbolo are old and who is the second generation?

Also a careful analysis of shareholding says may things, such as

Promoters sold 25% stake in 2013 to Ajmera’s to reduce the stake to 75%.

2.approx 3.38% shareholding is in Demat.

so only 1.19% od the share holding or 1.9lakh shares are available.

But also a related question is, if shareholding is so much concentrated, why they are not able to delist?

I trimmed my position in fomento because i wasn’t sure about the promoter intent and felt they were not very shareholder friendly. However, the business thesis remains unaltered and my opinion is that its very stable kind of business with great margins and a steady sales growth available at reasonable valuations.

@bheeshma I was also interested in this counter (fomento) but gave up due to 2 reasons. One mentioned by you and second due to legal troubles for some of their property where they can not do further expansion

For a long term bet, firstly, the management has to be ethical. Hoteliers are a shady bunch. 9% exposure is a daring move. Plus it’s a very asset heavy business, tough to see growth which comes with enormous risk.

As mentioned in my previous post, I have trimmed the position. There were some doubts about whether the promoters were shareholder friendly or not. Upon further reflection i decided they were not. Barring that I think the business is decently growing and nothing has changed in the thesis.

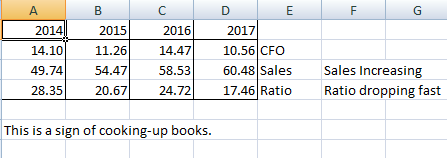

Check its Sales versus Cash From Operations for past few years. Sales is steadily increasing, like clockwork. But, Cash From Operations is in fact down. Why should this happen in a Hotel, they get paid in advance. This divergence is dangerous.

It has had seriously negative numbers in Free Cash Flow for past five years. Normally, one would say “Asset heavy companies have that requirement”, but in this case it is a little dubious. Moreover, five years is a very long time to not have +ive FCF. Why so much aggression?

FCF is pretty much required to conclude that a company is growing and healthy.

I need to ask a question… In case of Fomento

Cash from opertions = Net Sales - Increase in account receivables

Increase in account receivables = Net Sales - CFO

=60.48 - 10.56 = 49.92

Increase in Account Receivables is 50Cr… a hotel is getting cash payment of only 17% of its Net Sales… that is a googly.

It is possible that I do not understand these terms correctly. Pls guide. Am from Engn background, learning Accounting as and when required

Good to see one making a sincere effort to understanding the books before investing. Keep it up!

Sales increasing and CFOs decreasing is as good a metric as any to understand whether the business is doing well or not however it doesnt automatically imply cooking of books. Both advances from customers ( a current liability) & receivables have sharp negative movements causing a fluctuation in the cash flow. There is also a steady reduction in depreciation over time that has also contributed to the reduction in CFO.

The other flags were related party transactions and the preference share dividend of Rs7.5 per share. With a general increase in my investment knowledge i realized these things mattered and over time i have reduced exposure to a now negligible level. On the plus side the entire travel, tourism and hospitality sector seems to have come out of a 3-5 year consolidation and should do well in the future.