I have been holding ITC since 2005, and it has been giving me 25-30% CAGR consistently. So I am pretty happy with ITC as part of my portfolio. At that point of time it was pure intuitive decision based on the cigarettes edge and the investments in Agri & FMCG business which I thought would pay off.

Today I am not in love with ITC - Capital allocation is suspect there. However I have not completed diligence on other FMCG bets to be able to say that a Nestle or a GSK will deliver better compounding over next 5 years, and why. With the rest of the economy being in doldrums - Valuations have kept getting abnormally rich in these (but with slowing growth) - giving me less incentive to finish off that work. I agree HUL seemed the least attractive of the lot - primarily being mostly me-too with little competitive pricing power. Thatway Page Industries can be a better bet with rich valuations but consistent high growth.

I do not have a FMCG pack view currently - I have to first complete the work for Marico, Dabur, Emami, etc to have a better more-complete understanding of the overall opportunity pie and individual company strength/weaknesses - the FMCG pack though has very diverse companies. And then I will finish the modeling above, present my views, and ask for critique/guidance on the same. Hopefully I will find enough time by Aug-Sep to complete this exercise, from my side.

Guys, please look at the excel worksheet provided in the model (FMCG-Decoded.xls) attached in a previous post. Apart from collated industry data, there are very concise individual sheets for Nestle, GSK, HUL, Colgate, PGHH, in there.You may like to complete details for left out companies like Dabur, Marico, and Emami etc therein - for the benefit of everyone.

You are right Donald about the valuation. Having said that normally these are never available near at a PEG ~ 1 (even during 2009). I think a PEG < 2 is reasonable. Page is in a different league in terms of consistent past growth and future visibility. In fact thats my top holding (around 25% allocation). Since this thread is about FMCG, I didn’t mention page. (The Pages, Pidilites, Asian Paints, Kajarias , Ceras can be discussed separately)

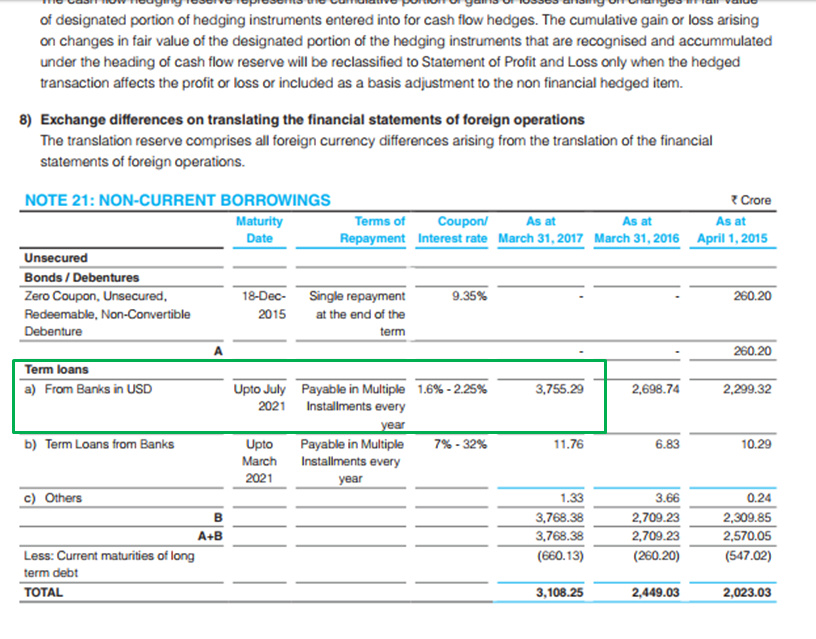

Godrej Consumer Products Ltd is a well established FMCG major. It has grown tremendously primarily through acquiring other smaller FMCG companies in a similar line of business esp in Africa & Latin America. It also has a unique customer profile - people of African descent for which it aims to be the preferred hair care company worldwide. The acquisitions have been funded by debt & It has a pretty high debt to equity ratio of 0.75 for a FMCG company - however after looking at the AR 17 , i found something that i didn’t know

Almost all of its debt is in USD & has an interest rate of between 1.6% - 2.25% , which means that its overall cost of capital is pretty low. With such a uniquely positioned capital structure , the earnings multiple of ~50 that the market is assigning to it , in my view is relatively low & it seems to me quite undervalued from this point of view.

Yes we are in a bull market but i kind of understand your point of view. Under normal circumstances , almost all large FMCG companies have very little or no debt and grow in steady double digits. They really have no need to borrow - therefore the market prices perceives its cost of capital assuming that if they were to borrow , they would at the prevailing indian interest rates and repayment capacity.

Here we have an uncommon situation where a large FMCG company actively borrowing to fund its growth & its overall cost of capital is way lower than that of any other large FMCG company with zero debt. Having no debt increases the cost of capital as equity is much costlier than debt.

The relative PE multiple is therefore attractive as other zero debt (higher cost of capital) FMCG majors are available at much higher multiples.

This access to super low cost of borrowing should ideally be assigned some value by the market - as reflected in its PE and hopefully it will happen in the future. That is basically the thesis , so lets see

Hi bheeshma

Real risk i see in your thesis is that low interest cost borrowing will be due in July 2021 and it has to be paid in USD only .

This is big currency risk , they are hedging it but to add on this maturity risk one more risk is there international earning currency is not only USD it is from Africa, Indonesia,Latin America,UK and they have to hedge it also

In AR they have mentioned in Risk

Sensitivity analysis

A reasonably possible 5% strengthening (weakening) of the Indian Rupee against GBP/USD/EURO/ZAR/AED at March

31 would have affected the measurement of financial instruments denominated inGBP/USD/EURO/ZAR/AED and

affected profit or loss by the amounts shown below. This analysis assumes that all other variables, in particular interest

rates, remain constant and ignores any impact of forecast sales and purchases.

Effect in INR Profit or loss

Strengthening Weakening

March 31, 2017

GBP 0.05 (0.05)

USD 2.99. (2.99)

EURO 0.80 (0.80)

ZAR 0.05 (0.05)

AED 0.06. (0.06)

CNH/KWD 0.03 (0.03)

3.98 (3.98)

So fluctuation in currency may affect interest payment and maturity payment

Second important thing for me

As per screener

ROIC of

HUL 202

Colgate 86

P&G hyg 46

Dabur. 53

Godrej consumer 19

So for me it is capital inefficient company (4000cr debt and working capital 855 cr)

Market give FMCG company higher multiple only for there capital efficiency in this company only godrej legacy is giving high multiple

Thanks

Ashit

Currency risks exist and have always existed. As mentioned they get hedged but yes they remain a threat for sure.

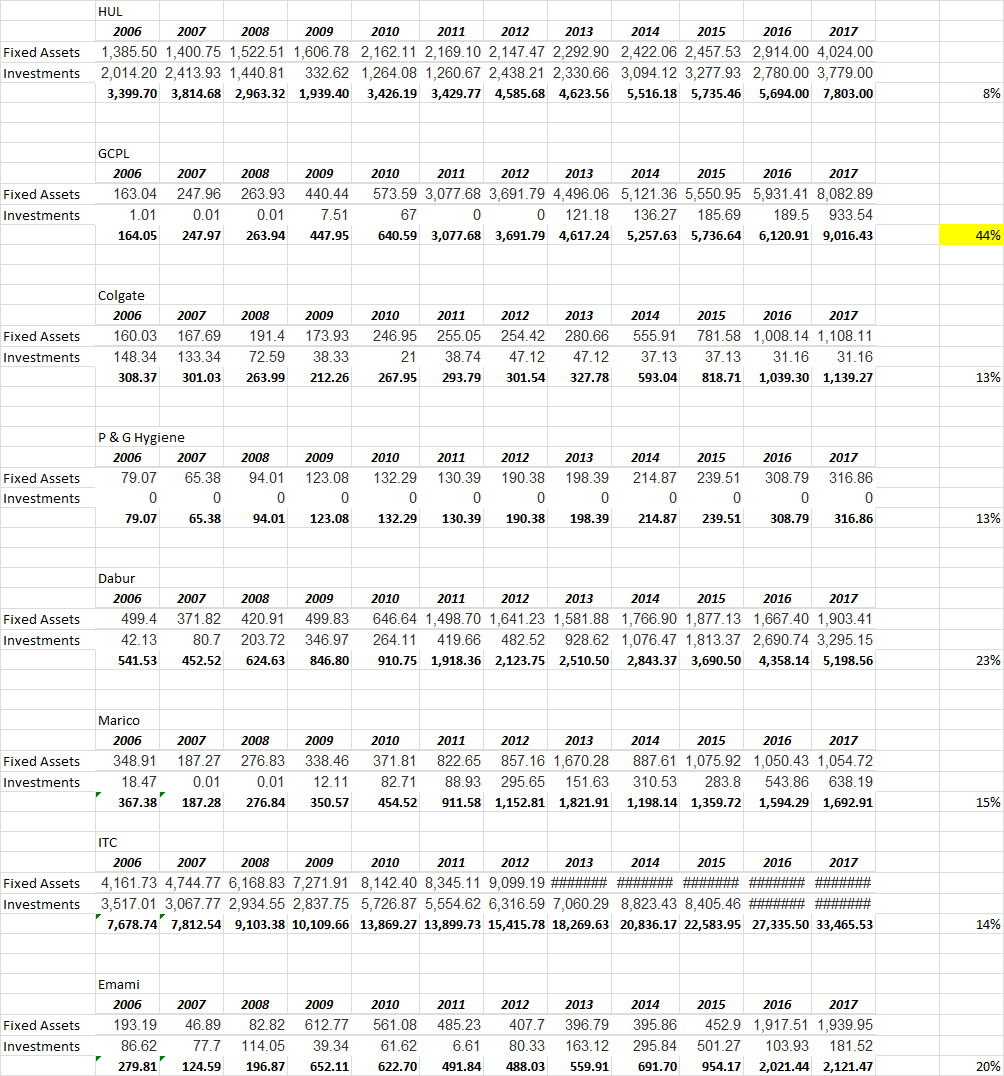

The ROIC that you have mentioned may not be strictly comparable because the reinvestment rate is different for all companies mentioned. Companies that are reinvesting faster will have a low ROIC initially and it takes time for earnings to happen after investments are made in assets that are supposed to generate those earnings. Here is a comparison of some FMCG majors that i could think of and growth rates for their investments in Fixed Assets & Investments over an 11 yr span.

As you can see, Fixed assets + Investments of GCPL have grown at a CAGR of 44% - it leads the pack by a mile , the next highest is Dabur at 23%. HUL is a measly 8%.

When you think that this astonishing investment growth has largely been funded by borrowing at an average cost of 2%, i think that that is not being priced in as much as it should by the market.

Calculating FCF for a company like GCPL which is growing its asset base at a very fast pace is a difficult task. However, most of the capex would be growth capex which would be different for HUL lets say where the asset base has grown by 8%, so most of its capex would be maintenance capex. In any case, as long as the OCF is hugely positive i wouldnt worry too much about derived numbers like FCF ( in this particular situation)

The major gain is expected to be from input credit of tax paid on advertisements.

"Under the current taxation laws, input credit on sales tax and VAT is not available as it’s not considered as manufacturing expense. Under GST, however, input credit of 18% would be available even on tax paid on the advertising expense, this would mean companies would have larger advertising budgets

In preGST , if the advertising budget of a company is Rs 100 crore, then sales tax and VAT paid under the current regime is an expense.

On the same amount, however, the GST paid could be categorised as manufacturing expense and hence the company can claim a tax credit on this expense, thereby increasing the profit. "In order to keep margins constant (to comply with the anti-profiteering clause), we expect incremental spending by industry in advertising to boost volumes.

guys,

when every company ( other than a bajaj corp) in FMCG is trading at 50,60,70,80 PE, why is gsk consumer getting only 33 PE?. sure, the business performance hasn’t been great in the recent past. but the others haven’t done anything great either. it has a wide moat. agree about the competition from patanjali. but thats there everywhere. plus the market also expands. one can argue its pretty much a single product company. but then most of the the other companies also rely heavily on their niche product.

GSK consumer growth prospects have slowed down considerably with Kellogs and other breakfast options coming to replace goodness of Horlicks. It is evident from developed world where Horlicks sales have gone downhill. Also, being a MNC they can not venture into other lines of biz. Their diversification to noodles, oats and biscuits have not worked out.

I concur with nav_1996 on his points. Just to add, we must not ignore the competition from unlisted players like MTR which has recently launched 3 min breakfast. Most importantly, these are local delicacies which are seen as healthier options (albeit the sodium levels which are present in all packaged foods would be unhealthy element) .I feel that MTR (others, if any) may provide a strong competition and grab market share from Kellogs and to a larger extent from GSK consumer…!

After recent correction in the stock price of ITC from 340 to 265 makes it look reasonably valued at current levels.

GST Taxation being on higher side will keep Cigarette business under pressure.

Current Q2 results are not showing much signs of growth in non-cigarette business but it may pick up after few quarters, based on above findings in the previous post.

For me, it is more of a steady low growth dividend yield stock.

Not sure if ITC is a pure FMCG play since it has other businesses like hotel, paper etc. In their FMCG portfolio, i dont see any niche product. All of them are a me too.

If once is treating it is a cigarette company ( which i think is the case), how about VST Industries?. their recent results have been much better than ITC. And vst has a better div yield.

After going through the thread from inception, the valuation has skyrocketed in the last five years with exception to ITC and GSK to an extent. i also note that while P&G is giving consistent CAGR of close 25% - 30% in the last five - seven years with high valuations, i am not sure whether it can be on one’s current buy list. Just wondering would it be preferable to include GSK vis-a-vis P&G considering the valuation. I have disregarded, ITC because it is not pure FMCG play as mentioned by Gauthum1. Any thoughts would be appreciated. Thanks