adding my 2 cents, in general, FMCG category --a business with general purpose products with mass consumption will rarely trade at comfortable PE multiples, and when that happens it is for a very short duration. These are certainly best buy from a long-term perspective.

MNCs in FMCG comes with a lot of experience in dealing with the Global consumer base and are very competitive, and can manage to fight a fierce battle to retain market share and to stay relevant.

Disclosure: Views may be biased; Invested in FMCG businesses; no trades in last 2 years.

I, never looked at ITC seriously. Surprised to know it generates profits more than twice that of HUL and yet both are valued similar. Cash rich cigarette business funding other diversified lines of business is what is not liked by investors. But, plain vanilla numbers are staggering. At 29 PE this looks a value buy. Incase Hotel, paper or FMCG business shows a faster growth, then rerating can happen big time.

Unlike HUL , ITC believes in owning assets - Large sized factories ( with huge land parcels ) , Branch / Head Offices , employee housing , hotels etc. All these assets are @ historic valuation and if we try to assess their market value it will be very high may be several thousands of crores …

In period 2003 - 2013) when HUL was going through tough times - it shored up profits by selling its marquee properties in South Mumbai and other places … So the real estate component in HUL has reduced …It helped HUL to improve its ROCE…

That is big difference between two companies … Now is it good or bad only time will tell …

Currently ITC believes it gives them better return than liquid funds and reduces variable cost esp office space rent , employee housing ( HRA reimbursement ) in long run …

Now should ITC get higher multiple than HUL …

The answer is No becos of Regulatory Risk of tobacco

What can change the story –

Faster growth in other FMCG business - Foods , Personal care etc ,

Strategic partner/ Listing of Hotel Business - 30000 crores

Listing of ITC Infotech Business - 15000 - 25000 crores

Listing of Paper boards / Speciality paper + Paper packaging- 15000- 20000 crores

Listing Agri Business ( one of largest exporter of coffee, wheat , tobacco , soyabean , rice ) etc + Diary , wheat , maida processor - Rs 30000 - 50000 crores or more …

Listing Retail Wills Lifestyle stores -

That will leave ITC with

Cig business - 14000/ 15000 crore profits valued at 18 PE - Rs 270000 crores

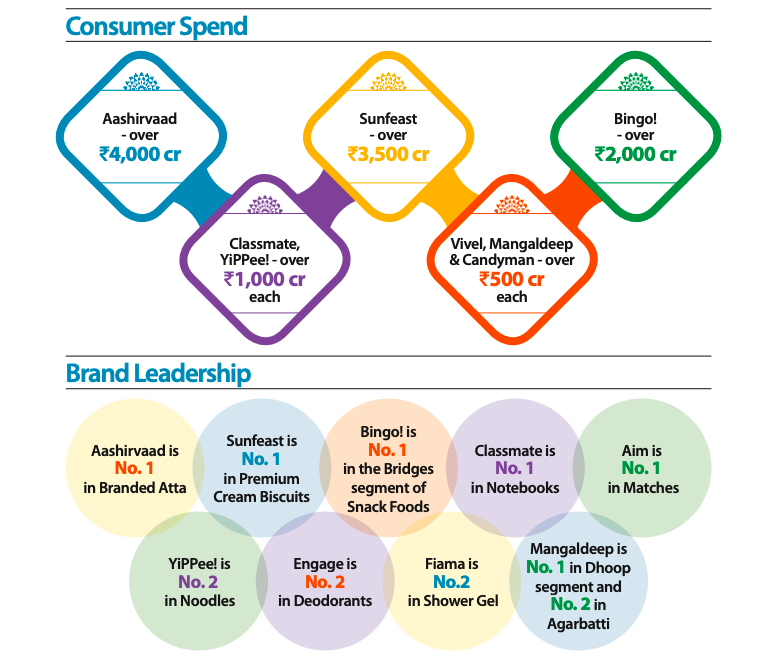

Market leading & profitable Atta & spices & ready to eat Business - 10000 crores ( 2X Brand sales Turnover )

Strong player in Biscuit / Snacks/ Noodles + profitable business - 20000 crores ( 3 X Brand sales turnover )

Children centric business - Class mate etc - 3000 crores ( 3 X Turnover )

Puja / Religious ceremonies related business - 1000 crores ( 2X Turnover )

Strong player personal care - Engage deos - 500 crores

Finally loss making personal care brands like Vivel , Juices , Ghee , Fiama , Chocolates , Coffee and may other @ Zero crores …

If you account for all you will see ITC is @ fair valuation with current structure and valuation may increase by 25% to 30% with listing of some of non core business

What analysis man… Just curious have you been an employee of ITC ever…

Now most of the positive triggers that you mentioned are demerger or listing of subsidiaries which we minority shareholders have no control. So doesnot it make a HOPE based investing…what should interest us is rather growth in these lines of business organically. Cig business commanding 80% revenue will not do any good for PE rerating… If it comes down to say 60% in next 5 odd years, then we can expect a 50 PE x 2EPS =3 times share price growth. Just my 2 cents.

I indeed feel sad that with so good free cash from cig business and massive distribution channel network, ITC should be able to wipe out other small Fmcg players like Patanjali or emami or Marico etc. No offence to the investors of these companies… Just putting myself in ITC management shoes.

Disc. Not invested in ITC. But interested esp valuations aspect.

You are right we cannot go with Hope investing - hence current valuation is @ fair level .

Cig is @ 50% revenue contribution level and not 80% revenue , but profits still is primarily from Cig . This is becos other FMCG , hotels , paper board etc are in growth stage and hence @ different level of maturity.

ITC has two option from free cash flows - One to distribute as dividends and another is to build Indian Brands … It has chosen to follow Path No 2 … This may go on till 2030 as per management discussions in public …

Now wiping out other FMCG companies does not makes sense … as opportunity size of building products is huge …

ITC entered late in FMCG space post 2000 while most others were present right into 1990s and unfortunately ITC entered into many categories ( same mistake has been done by Patanjali ) . Now under new management it is zeroing on focus … Hope that works …

Discl … Invested in ITC since 2009 … Made my first big money through this stock …

It is one thing to use perennial cash flow of cigarette business & distribution to enter multiple categories in FMCG and other thing to use every penny generated by profits to grow distribution, enter categories slowly, innovate etc. Maybe the perennial cashflow is the reason why ITC is not able to prosper as much in FMCG as it should have. A rich parent may not always have the brightest and most successful son Having said that I respect and use the products of both ITC, Marico etc.

Disc: Invested in ITC, Marico and few other FMCG Indian companies

Completely agree on above points. Good to see you are having long term conviction in ITC. Have you sold any percent since 2009? I hold ITC in small quantity since few years but evaluate from time to time if I should increase allocation. If ITC lists all its other business then holding company discount will come into picture. Also, in such cases, for minority investors, is a demerger better or IPO of its subsidiaries?

Actually l was too concentrated in FMCG stocks around 2012/13 so I reduced it in 2012/13 and invested in other sectors . I have put across why I did so in my thread BULL in BEAR Market.

But I still hold over 7% of PF in FMCG stocks and ITC forms chunk of it …

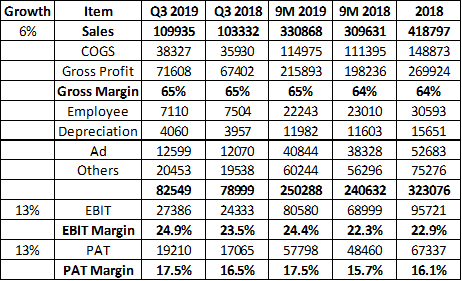

Good set of nos from Colgate. On a Quarterly basis , sales growth is 6% & Volume growth is 7% while EBIT and PAT growth is 13%. On a 9M basis the EBIT & PAT growth is a satisfactory 17% & 19%. So far it has been a great 2019 for Colgate.

I have been invested in Colgate for a full year now and it has done well through all the volatility experienced and has also given me a stable ~15% return over the period with low stress.

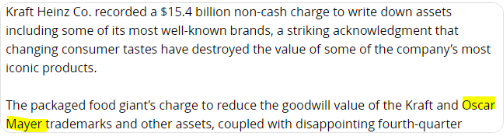

BE CAREFUL when you paying for FMCG MOAT … Kraft is great example how moats can disappear … over period of time . Over Generations people change - their Taste , their sense of Smell etc

Swadeshi movement. How do you define that? ITC is more Indian owned compared to companies such as Infosys and HDFC.

Consumer will buy quality products at reasonable prices. That is rationale behavior in long term. Swadeshi movement can be short lived emotional response but does not last. Patanjali is a good example of how this storm fizzled out slowly.

Currently ITC No1 : Sanjiv Puri ( CEO ) and No 2 Sumanth ( COO ) are both Ex ITC infotech CEO . I hope they bring their learning as IT CEOs to develop and execute digital strategies for new age consumers