Total income from operations rose 6% on a YoY basis in Q3FY’15 to Rs 37.19 crore while EBITDA fell 39% to Rs 5.94 crore. PBT was down 46% to Rs 4.47 crore while bottomline of the company increased 19% to Rs 2.95 crore.On a QoQ basis Total income from operations rose 11% while EBITDA grew 24%. PBT was up 19% and bottomline 19%.

For 9MFY’15 Total income from operations rose 6% to Rs 113.64 crore but EBITDA fell 11% to Rs 19.9 crore. PBT was down 11% to Rs 16.36 crore while bottomline of the company decreased 13% to Rs 10.65 crore.ADI Finechem is a specialty oleochemical manufacturing company situated near the city of Ahmedabad in the western region of India. By-product fractions of natural oils and fats generated during refining of Sunflower and Soyabean oils are company’s raw materials. ADI Finechem fine chemical products portfolio has applications in manufacturing of resins for Paints, Inks adhesives etc. The company also manufactures specialized products for neutraceutical industry.

The company is expanding its capacity from 25,000 tonne to 45,000 tonne at a cost of Rs 21 crore. Following a delay in receipt of key equipment, the expansion plan got delayed from September 2014 to December 2014 earlier and now from December 2014 to March 2015. The management is confident of selling additional volume and achieve optimum utilization of expanded capacity by Q4FY16 itself

Adi Finechem is the only producer in India of dimer acid/tocopherol accounting for 53.2% of FY14 revenue and a low-cost producer of others.The company won’t have any negative impact because of the fall in crude oil prices. There is perception in the market that oleochemical products of AFL can be manufactured through the synthetic route from crude oil. However, Linolic acid cannot be manufactured by the synthetic route, while dimer acid can be manufactured synthetically, but from toll oil. Toll oil is produced during the manufacture of paper and its prices are not correlated to crude oil prices. Hence, the sudden fall in crude oil prices won’t impact realisation of Adi Finechem

Unlike other chemicals whose prices have collapsed because of dumping by China oleochemicals doesn’t face stiff competition from China. Average realisation of various oleochemicals is lower compared to transportation costs involved, thereby restricting dumping from China. The company is selling its products at FOB price of Chinese suppliers (plus transportation costs), but is yet reporting a healthy margin. Similarly, because of high transportation costs, the company won’t be able to export oleochemicals.

Tocopherol, which accounted for 35% of revenue for Adi Finechem is entirely exported. At present, tocopherol is undergoing a downturn following oversupply. Generally, tocopherol follows an 18-month cycle. It was on an uptrend from 1QFY12 to 4QFY13, where its prices increased from Rs 155 per kg to Rs 572 per kg. Downtrend started from 1QFY14, where prices declined from Rs 572 per kg in 4QFY13 to Rs 300 per kg currently. The management expects the downtrend in tocopherol to get over by the next two-three quarters.

Thanks so much - you are doing a priceless job. Given that oleoresins seems an average commodity and tocopherol’s “super price” cycle has bottomed out, I expect returns to shrink from adi from these levels. At the CMP, IMHO, the risk reward is not asymmetric - infact, if anything, it has a fairly significant potential downside.

my research shows that adi was the beneficiary of a perfect storm - supply constraints in china, worldwide demand perk up for tocopherol. their new normal should have lower margins.

If you notice the average realizations of Adi for the last 5 years and take the lowest margins (OPM 14.5%) in these 5 years and extrapolate the top line as per capacity, the business is still looking good to increase Operating profit by 35%. This ofcourse doesnt take into account the increased operational efficiencies which are likely to kick in because of higher economies of scale.

5 years is not good enough. This was the rookie mistake I used to make - You could have said that about oil as well and look at where it is now - half of the lowest it was over last 5 years.

Thanks for providing the above links. I interpret the data that you provide in the second link a bit differently. As you probably already know, Adi is a manufacturer of tocopherol and not Vitamin E Oil. Vitamin E manufacturers such as BASF are actually customers of Adi. A shutdown by vertically integrated player DSM is likely to lower demand but at the same time due to integration lower the supply too. New capacities popping up are that of customers of Adi which IMO should bode well for the demand of the product. I am not saying that the prices will firm up any further but purely based on the articles you provided, there is no reason for the prices to fall dramatically either.

As regards oil, that is an entirely different story. I read somewhere that even at $40 per barrel, something like 90% of the global oil capacity achieves atleast breakeven on “cash profitability.” I am not sure if that is the case in Tocopherol. Further, just as irrelevant but to make a point nontheless, as Monish Pabrai says - whatever the price of oil, it probably makes sense to own Saudi oil which costs < $10/barrel. If you wait long enough, you will make money. Juxtaposing this with production of tocopherol; in a much smaller sense and scale, the low cost route that Adi adopts to produce tocopherol and oleochemicals using scrap from vegetable oil refineries makes it the “saudi” of oleo and nutraceuticals in some sense. Please dont beat me up on this - just trying to illustrate a point!

IMO, the issue is not that of price - its more regarding thelongevityof growth - supply of RM is only going to get more and more scarce which puts a question mark on the scalability of the business. But to me, the story still looks good for 4-6 quarters atleast (its a short term bet for me anyway)

Ofcourse, I remain open to all thoughts and opinions and if Adi disappoints in March, ill start trimming my positions. For now, I think Im good but I look forward to hearing your counter thoughts nontheless.

I do agree with you - vinati 's moat has been a lot more enduring wheres with adi, giving the benefit of doubt, I do not know how much of the moat is because of a good monsoon and how much is inherent to the “castle”. Only I do not track vinati and hence do not know how much of head room they have for growth.

Abhishek

All I am saying is why pay 20 x PE “crest” earnings ( I am sure EBITDA margins will not go up from FY 14 levels) for a business which IMHO ;

)- has some immediate tail winds

)- is still a one trick pony which has performed the trick only for 3-4 years (oleoresins are low margins, as has been covered elsewhere in this thread). May be the pony will continue to improvise on the trick

Also, pabrai buys these stocks at low single digit multiples - that gives him a margin of safety and hence is sensible.

I do a fair amount of primary research and my research indicates that tocopherol prices are if anything about to decline further rather than go up in the medium run. Given that risk, think if 20 x earnings makes sense. for eg., I am invested in OCCL which has a fairly wide, enduring moat and is trading at 9 x PE and is growing at 25-30% steadily.

And you can get google and apple at sub 20 PE, for the record, each growing at 30-40 % EPS.

This point - I completely agree with. By no means is it a fat pitch. Will definitely look at OCCL but in this market (in all humour) are you able to find anything which has even a remote semblance of a fat pitch? Any ideas that you think are worth spending time on?

I would not be bold enough to venture out to buy a rapidly changing company such as google or apple though they do seem to have “fat” moats but with companies such as these, you never know where the next big blow is coming from!

it’s relative - I am looking at 2-3 stocks where I am so sure of fundamental performance that the probability of loss is low. Does’nt it make sense to add more of them than adi and hope for some luck ?

OCCL was a fat pitch at sub Rs. 300 but now now - no fat pitches now.

Adi Finechem

Expects capacity utilization of 80% from Q2FYf16

Adi Finechem held a conference call to discuss the results for the quarter ended March2015 and way forward. Senior Management of the company addressed the call

Highlights of the Concall

• Total income from operations fell16.4% on a YoY basis in Q4FYf15 to Rs 37.1 crore while EBITDA fell 50.9% to Rs 5.6 crore. Bottomline of the company decreased 53.8% to Rs 3 crore.

• On a QoQ basis Total income from operations fell0.3% and EBITDA fell5.1% while bottomline was flat.

• EBITDA margin of the company was 15.1% in Q4FYf15 compared to 25.7% in Q4FYf14 and 15.9% in Q3FYf15

• PAT margin of the company was 8.1% in Q4FYf15 compared to 14.6% in Q4FYf14 and 8.1% in Q3FYf15

• For FYf15 Total income from operations fell0.7% to Rs 151.3 crore and EBITDA fell 24.3% to Rs 25.5 crore. Bottomline of the company decreased 26.7% to Rs 13.7 crore.

• The last phase of on-]going expansion programmefrom 25,000 tonne to 45,000 tonne at a cost of Rs 21 crore is continuing satisfactorily and is expected to be fully commissioned by end of June 2015

• Although sales volumes have improved sequentially and yearly basis, the realization of Tocopherols continued to remain under pressurein the quarter under review

• The company has processed 23% higher raw materials in FY'15 at 23712 tonne compared to 19208 tonne in FY'14

• Topline fell during the quarter mainly due to subdued product prices.

• The company expects capacity utilization of 80% from Q2FYf16 onwards and more than 90% by Q4FYf16 of the expanded capacity.

Disc: Not Invested

PS: Hope @hemantbhatia does not mind in me sharing the load to provide the concall details, whenever possible.

Highlights of the Concall by Capital Mkt

Total income from operations fell9.7% on a YoY basis in Q1FY’16 to Rs 38.83 crore while EBITDA fell 57.7% to Rs 3.88 crore. Bottomline of the company decreased 88.2% to Rs 0.62 crore.On a QoQ basis Total income from operations rose5% while EBITDA fell30.9% while bottomline fell 79.7%.EBITDA margin of the company was 10% in Q1FY’16compared to21.3% in Q1FY’15 and 15.2% in Q4FY’15

PAT margin of the company was 1.6% in Q1FY’16 compared to 12.1% in Q1FY’15 and 8.2% in Q4FY’15

The last phase of on-going expansion programme from 25,000 tonne to 45,000 tonne has been accomplished and commercial production started in July 2015.Unforeseen situations impacted margins in Q1’FY16, which are unlikely to occur from Q3’FY16

Globally, there are four customers of tocopherol and AFL sells to two of them currently. To tackle the current weakness in tocopherol, AFL plans to increase its customer base. For this purpose, it has appointed an US-based consultant. The process to get new clients is lengthy including auditing of plant etc. Currently, a new client is close to the end of due diligence process and will start buying tocopherol after 15 days, the benefit of which will be visible partially in 2QFY16 and fully from 3QFY16.To comply with the requirement of new clients, AFL incurred additional expenses to upgrade its plant, which impacted production in 1QFY16. The exercise started in May 2015 and is expected to get over by mid-August 2015. With production being lower and AFL incurring additional costs, margins were very low in 1QFY16. A significant portion of the costs has been booked in 1QFY16 and the remaining will be booked in 2QFY16. Margins are expected to return to their normal range of 15%-18% from 3QFY16.

Expenses incurred in Q1FY’16 and likely in Q2FY’16 will be one-time in nature and won’t increase manufacturing costs. Hence, AFL is expected to achieve steady-state margins in the range of 15%-18% from Q3FY’16.Price of tocopherol bottomed out in Q4FY’15 and did not decline further in Q1FY’16. For AFL, a few orders in Q4FY’15 were at a higher rate because of an old contract, which was not the case in Q1FY’16 and therefore it witnessed around 20% QoQ fall in realisation.Total volume was up 18% from 6100 tonne to 7201 tonne because of a 46% volume growth in oleochemicals from 4367 tonne to 6370 tonne in Q1FY16 Oleo chemical plant operated at its full capacity and margins were stable even in Q1’FY16. Following weak demand, volume in tocopherol declined 50% from 1,732 tonne to 864 tonne in Q1FY’16. With lower volume and lower realisation in tocopherol, export revenue declined 77.3% to Rs3 crore in Q1FY’16 from Rs13.2 crore on a YoY basis while it fell 66.6% on a QoQ basis.

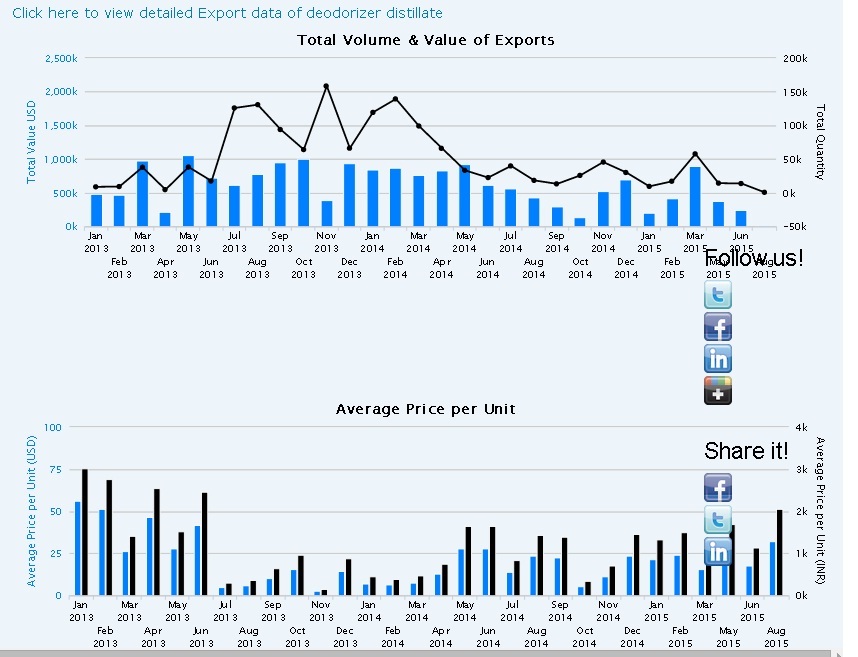

Adi Finechem exports DEODORIZER DISTILLATE (MIXED TOCOPHEROLCONCENTRATE) WITH 08.35% TOCOPHEROLS.

When I check export data it shows declining trend. Adi might be loosing market or demand for there product might be decreasing

Dont be confused mates. The situation is simple for ADI Finechem.

Their competitive advantage comes when crude oil prices are high as they make their product from edible oil waste while their competition makes the same product from crude.

So now when Crude is at multi year lows and has fallen from $100+ (this was when ADI was flying due to competitive advantage) to $40-$44 range…its has completely killed their product competitiveness internationally.

Tough days ahead for ADI…because with China’s slowdown, Iran sanctions lifted, US Shale boom…looks like Crude will be in 30-50 range for sometime.

Question is whether ADI can sustain this low crude environment. It will become interesting if the stock price goes to 100-150 odd and if Crude can rise to 75-85 range.

The issue is not with Crude but their Vitamin E market which I think has been discussed fairly extensively in the post. If that market/ realization picks up then things would be better for them. The management have been evasive on what’s happening in that market.

Rohit, thanks for this. heard the call but was unable to decide if these margins are sustainable. have decided to wait for a couple of quarters before proceeding further.