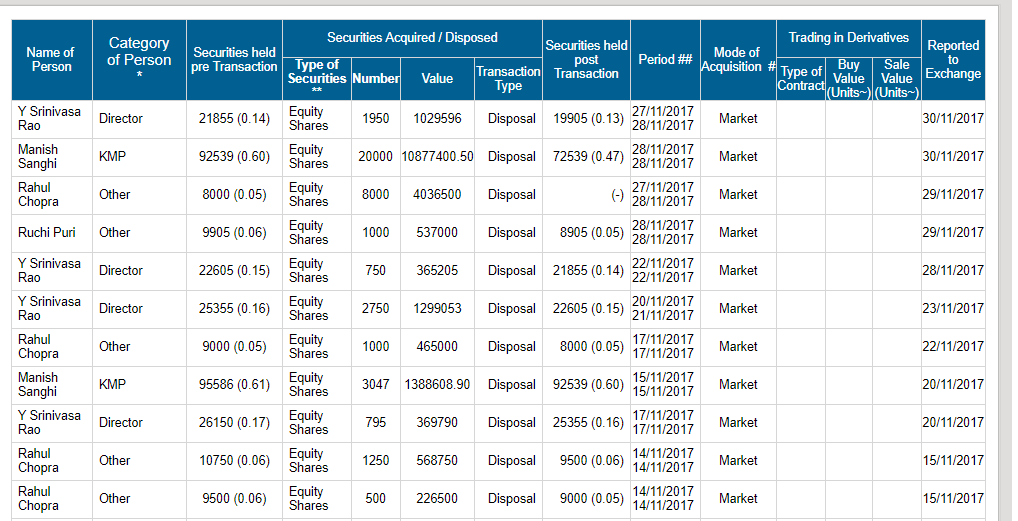

promoters selling again ???

Analyst report from Ventura on Everest Industries -

Got a chance to talk to couple of distributors of Everest Industries in Pune today. Below is the brief of the details they shared.

-

Company does not provide any credit to distributors. Distributors have to deposit amount to company as a rolling credit and they can purchase material only till the limit of their current deposit with company. Company adopted this practice after some of their distributors failed to pay money on time in past.

-

GST is helping company to garner more market. Pain of GST is almost over now and things are back to normal.

-

Rural area is driving the demand for company. Fiber cement roofs are preferred over traditional roofs due to their inherent advantages.

-

Everest’s Rapicon cement walls are in demand in rural areas due to its portability, ready and easy to use nature. I was told that small rural homes are constructed as quickly as in two days using these cement walls. These walls are also used in making toilets for various Goverment schemes like swachha bharat.

-

Mumbai is a big market for cement boards

-

Shift from plywood to cement boards and panels is clearly visible and company is aggressively targeting customers there. This can be a huge market for company.

-

Competitors in Cement roofs are Visaka and Charminar. They told that quality wise Charminar and Everest score over visaka.

-

As per them company has failed in Pre-Engineered Steel buildings. When i told them that company has turned it around and reported profit in Q2, they were surprised a little. As per them, there is no market for PESB materials in and around Pune as of now. Company is targeting big industrial orders in this segment.

-

Company provides training to them to promote their products and take them to site visits often.

-

One distributor is with the company for more than 15+ years now and he was well aware about the company finances. He told that company should do roughly 1300-1400 crores of revenue this year. Not sure how a distributor can predict company revenue but he was very confident. Interestingly, after Q2 Everest has given guidance of 1200+ crores of revenues for FY18.

Some of these details are already shared in various research reports. However, it was assuring to here it from the people directly dealing with the company.

I am planning to meet more people associated with the company in next few days. Shall share details here if i find anything extra than what i have posted above.

Views/comments invited.

Regards,

Suhag

As long as steel prices stay high , rupee is strong (raw material chrysotile is imported) and rural spending/monsoon is adequate, this stock has a lot of headroom for earnings expansion. The pricing in steel building contracts also seems to have improved as they have entered clause for price increases as per the management in one of their older concalls. Price to sales is still reasonable

Disc : Invested at much lower levels when I started the thread

Vijay Kedia has increased his holdings from 2.51% in Sep-17 to 3.89% in Dec-17.

Disc: Invested and may add more at appropriate opportunities.

Regards,

Suhag

According to Kenneth Andrade, rural spending would increase exorbitantly in the next 18 months. I have read the PMAY (“Housing for All- 2022”) scheme and the Govt targets to build 1 crore houses in the next couple of years. I believe Everest Industries will be a potential beneficiary through this. There is a strong reason for their revenue to double in the next 2 years.

Everest Solar business will be benefited through this project.

Overall Good Show by Everest in Q3.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/05fe4e20-d55c-4773-ae33-68ce2025639a.pdf

Can someone please advise what to make out of Steel segment EBIDTA?

Regards,

Suhag

Commodities cycle to play out in the next couple of quarters. Oil price is increasing which will drive demand in middle east countries and also in few countries in Africa. Revenues and earnings for Everest will actually up in the coming quarters.

Solar business would pick up in some time. If that is factored in, there would be a drastic increase in their top-line growth.

No doubt this stock has a high chance of becoming a multibagger.

What business they have in Middle East? They have in fact closed their subsidiary there recently.

Company never talks about Solar business. Would appreciate if you can share any info on that.

Regards,

Suhag

Read their annual report. They had mentioned that the exports are subdued because of muted demand from middle east nations. Their business will pickup in the subsequent quarters. Even if the steel prices increase, the costs would be carried over to the customer. This business model has changed compared to previous years. This puts in Everest in a competitive position to shield itself from any further increase in commodity prices.

One good thing about Everest is that they have adequate capacity and have the capability to cater to customers from all segments. This stock is not meant for traders because it requires a long way to go. Timeframe: 1 to 2 years.

About Solar Business: It is a sitting duck. It will play out in a year or so. Once the credit cycle turns up, the spending out increase.

No doubt why HDFC’s Prashant Jain and Vijay Kedia are betting on this.

This report explains that Everest Industries is one of the huge beneficiaries in PEB segement.

Earnings to go from here. A structural change is happening. Order books are filled up. Everest will turnaround from here. New orders are coming up in PEB segment coming in.

NCLT is happening in a rapid pace. There will be a turnaround in a lot of steel companies going forward. Once the credit cycle happens, it will increase the product demand.

“Housing for all” is another major driver for Everest Industries. Based on their capacity and revenues going forward, they can become a midcap company. We have to close monitor the commodity prices and how things are turning up.

I would stick with the sector leader with the high quality management. Based on my research, I find this company (Everest Industries) is catering to people from all economic segments.

@saravananb1994 as per the forum guidelines requesting you to share the source of the news of orders coming in from middle east. Also, share your rationale on how this stock is undervalued compared to its peers for the larger benefit of the group.

Just mentioning that this stock will be a multibagger will not help anyone here.

Regards,

Suhag

Thanks for pointing it out.

As oil prices are increasing, most of the oil producing countries are now moving out of their recessionary phase. Due to which, they are starting their caPEX.

Primarily, we can get this information through scuttlebutt.

“Housing for all” project is kicked off and there will be a good increase in top line for Everest going forward. We will start to see good results in the subsequent quarters.

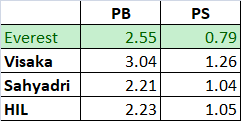

Coming to your question on how this stock is undervalued to its peers, Everest Industries is trading at a FY18 PE - 16, PS < 1, Avg Div Yield above 2% for the past 5 years.

All their plants are strategically located to cater to customers from all segments. It will save them a lot of cash due to freight.

We will have to closely watch the developments in the upcoming quarters.

Disc: Have vested interests.

Thanks. However, could not find anything substantial in the report (No intention to discourage you). Its just projection of the industry and its at a very high level on which markets will drive the demand. Nothing specific.

Coming back to the orders from middle east, i still do not see any source which confirms that they have started receiving orders. When L&T announces order, we have a media release. I know Everest does not work like that but if they receive an order then there has to be some source which can confirm that. Are you saying you have scuttlebutt for that?

Regards,

Suhag

Yes, we could get to know the information through the suppliers and distributors.

Why is the promoter selling shares.

Promoter is not selling shares. That’s a director. Regular employees and non-promoter directors typically sell shares when they’re vested under ESOP.

It’s only a red flag when promoter is selling in open market

Disc: Invested & added more recently