This is an old story - often dismissed by many investors saying that they had lost a lot of money many years ago . This happened due to banning of blue asbestos . The company now deals with white asbestos made out of chrysotile fibers - which is NOT a banned product and will not get banned in the future.

This is an interesting bet with main drivers being - Rural development through better incomes and Industrialization - through development of industrial corridors and Make in India.

Market Cap - 450 Cr

Debt- ~ 160 Cr

EV - Rs.610 Cr

Sales - 1300 Cr (growth ~30% in 2 bad years due to poor monsoons)

PAT - ~30 Cr

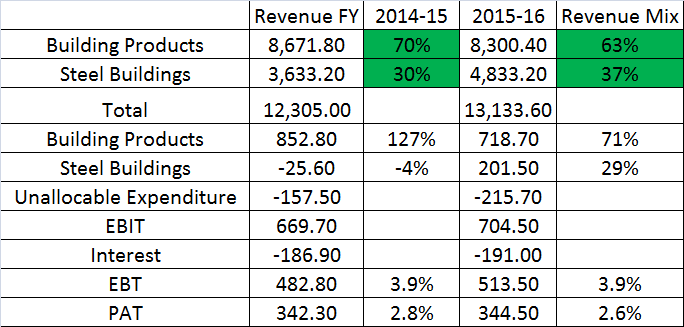

While the building products is the bread and butter business - roofing sheets - this business is dependent on monsoons . Every year there is a good monsoon - this business will give out a good EBIT of 100 Cr+

The second new line of business has grown considerably to now form 37% of revenues in FY 2015-16 . This is the pre-fab structure business - (think warehouses / large retail format stores / factories). With revenues of 483 Crores and albeit a lower profit margin at the moment. Clearly there is a case for more business from an organized - dependable player like Everest for timely execution. Most of their customers are the one’s who cannot afford a delay in execution. For others - there are cheaper alternatives. To benchmark - Pennar EBS business is at 1.3 times sales and 15 times PAT. Everest is still not as profitable - but the trend of increasing profitability can be seen

Mutual funds will also get interested once the market cap increases a little.

Key risks -

Building products - Bad monsoon , High Chrysotile prices ;

Steel buildings - High steel prices, Competition reducing profitability

Hi guys, while i do think Everest is fairly valued right now, I think there are far better companies out there in this industry that you could possibly look at

Upon implementation of GST and with better monsoon, more and more value added and eco friendly roofing solutions will be sold which has higher realization and margins

The company held its AGM on 29th June 2016 and was addressed by Mr. Manish Sanghi MD

Key Highlights

Management is satisfied with the progress of overall monsoon and rural economy. The June deficit is narrowing day by day. The rainfall is progressing as per the IMD projections. Most of the farmers and most of the industry players have already planned accordingly. This should help in overall rural economy and hence the company in FY’17.

GST will not have any major impact on the company’s sales. As most of the market is divided among the organized players.

Overall volumes in building product segment were flat in FY’16 due to lower demand, lower Middle East sales and lower monsoon and related uncertainties. For FY’17, management expects a double digit growth in building product segment through a combination of both higher volumes and better realizations. Some price increase was also made in June’16 quarter due to better demand and off take.

Steel prices are up by around 10-12% in June’16 quarter on QoQ basis. Roofing solutions is more or less now competitive compared to steel segment. Management expects overall roofing segment to be more or less to remain competitive compared to steel segment for entire FY’17, given that steel prices have bottomed out and have fallen so much in FY’16.

No major capex planned for FY’17. The company has sufficient capacity for a double digit volume growth in FY’17. It would require to do capex for H2 FY 18 production growth if the demand continues to remain strong.

Due to uncertain crude and Middle East economy, management is going slow on its green field facility in UAE for panels and boards.

The company continues to see strong traction for steel building segment with order book of around Rs 200 crore translating a visibility of around 5-6 months. Increase in steel prices can have some marginal impact on margins, but with good volumes, management expects to retain the overall margin in this segment in FY’17.

Due to lower crysolite prices in FY’16 which is further lower in FY’17, overall working capital requirement has come down for the company. Management expects working capital requirement for FY’17 to be more or less similar to FY’16.

The inventory of higher cost crysolite raw material is over and the company already received the benefit of lower raw material prices from June’16 month onwards.

Overall, despite higher base of June’15 quarter, management expects traction and strong growth to continue in June’16 quarter as well.

Also upon implementation of GST and with better monsoon, more and more value added and eco friendly roofing solutions will be sold which has higher realization and margins. As per the management the higher realisation asbestos market is a huge market and has wide scope. Almost all the industry players have started to tap this segment and given the wide market potential, there is a scope for every player.

Its quite surprising to see Everest doing poorly in both the segments for few quarters now while competition continues to do well.

Roofing -

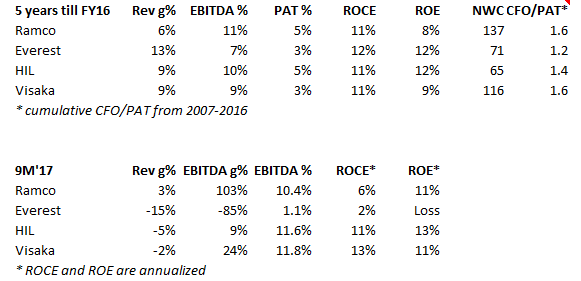

This company just like other companies in the roofing space had generated good profitability and return ratios in the last cycle 2010-2013. Last 3 years proved to be tough for the industry because of poor monsoons largely. However in FY17 so far, there are signs of revival if we look at segmental numbers of Visaka and HIL while Ramco and Everest continue to report losses. Visaka has done splendidly well because of its growing boards and panel product line. However, its not clear to me why Everest and Ramco reported losses, any idea?

PEBS -

Pennar does 10%+ margins while Everest is surviving to make profits. Its quite difficult to understand the stark contrast b/w two companies.

Overall, amongst the 4 players, Visaka and HIL have done quite well in FY17. A lot depends on monsoon as major chunk of profits still come from roofing sheets for all the companies.

Valuation -

Its a fairly mature sector and every player is trying to reduce its dependence on asbestos sheets. In last few quarters Visaka has done a great job in that. Its growing boards vertical is highly profitable (15% margins). Hil is also trying to bring its dependence on asbestos to 60% in next 2-3 years. Everest, though, has done a great job of diversification into PEBS but it always struggles to make money there.

Going by the conventional ways of valuation, pls refer the attached excel, Everest seems to be priced in line with Visaka, HIL. And both these companies, Visaka and HIL, are trading at their upper band of historical P/E. If these two companies continue to report changing mix and rise in profitability then I believe they do deserve such multiples or may be 10x-12x+ but coming back to Everest, it is very difficult to justify such high valuation unless there is clear road to profitability from here.

Management talking about better pricing of contracts in PEBS in their presentation. This should lead to a turnaround in the companies fortunes as topline is good but margins have got impacted due to poor pricing of contracts and steep increase in steel prices. Can recollect CFO/Finance director leaving - maybe this had a part to play in it.

With building products in a better space with second consecutive normal monsoons, the overall health of the company should improve.

HDFC Mutual fund reduced their holding in September quarter. They sold some more shares on 17th Oct as well. Overall they reduced their holding by 2+ % in last few months.

Last year Revenue was around Rs 1167Cr. The real question is how much more they can do than 1200cr. H1 revenue is 637cr so they are on track to hit 1200cr but that won’t excite the markets.

Also, operating margins @ 5.34 were the lowest in last three quarter.

They have many things to improve to keep the good show in the share price intact.

In the video posted above, Manish Sanghi says “One shouldn’t compare this year with last year, we need to compare this year with the year before.”. FY16 revenues were 1313 crores, if I understood him correctly then they should do better than this figure.

Though they have been cutting costs by rationalizing the logistics and they have brought down the debt and they have reduced the working capital but there is nothing in their performance which can explain the recent stock price increase. May be it is getting re-rated because of the euphoria about affordable housing but it is insane how the stock is going up.

Disclosure: I am invested in it from at a much lower price