The higher amount is because they are following a weird model of stepped amortization of their film rights revenue

As per AR:

“For first release film content, we use a stepped method of amortization and a first 12 months amortization rate based on management’s judgment taking into account historic and expected performance, typically amortizing 50% of the capitalized cost together with print and advertising costs for high budget films released during or after fiscal 2015, and 40% of the capitalized cost together with print and advertising costs for all other films, in the first 12 months of their initial commercial exploitation, and then the balance evenly over the lesser of the term of the rights held by us and nine years. Management determined to adjust the first-year amortization rate for high budget films because of the high contribution of theatrical revenue. Similar management judgment taking into account historic and expected performance is used to apply a stepped method of amortization on a quarterly basis within the first 12 months, within the overall parameters of the annual amortization…”

What this will do is that it will generate a deferred tax line item in the the FStatements. From what I have seen , it is growing every year to the tune of 50 crores per year. In the cash flow statement you would see a huge amount as reversal of depreciation/amort as the cash has not gone out of the organization ( They have neither paid advanced tax nor do they have a defined amortization policy, which is not at all according to the upcoming IFRS standards to which they have to abide to I believe as the company is listed in US).

But I do not see any covering up of information, the cash is there in the books as far as I can see.

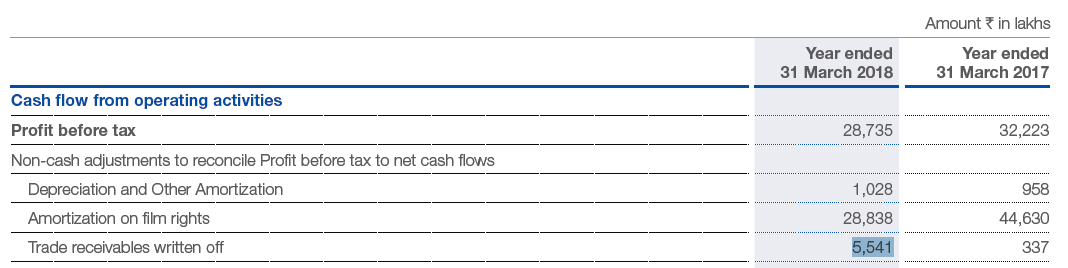

IMHO, the main reason for discrepancy is that depreciation in the p&l includes only depreciation on fixed assets which is a relatively small figure. In the cash flow statement however, it also includes amortization cost of content, which is a non-cash expense. The same appears in P&L as part of content cost (part of direct expenses). In the cash flow this expense is compensated by the fresh investment in content shown as change in working capital items, namely content advances and distribution rights and under investing activities as fresh titles created.

Yeah, seems fishy to me too. Where the cash flow is much less than reported profit, we can safely assume foul play in profit reporting. But I don’t know what sense to make of the opposite case.

Cash flow from operating activities ie, OCF is calculated as the sum of net income, adjustments for noncash expenses and changes in working capital.

Here they have lots of noncash expenses shown (under net income), which will get reverted in the OCF calculation Hence the multiplier effect. It need not be fishy if it is accounted for in the numbers. I couldn’t find any clear manipulations.

Would be helpful if someone can point out some negative facts about the company’s numbers.

Discl: I’m invested as I couldn’t find anything really fishy in the numbers after all the crash this scrip has seen.

Considering that Eros amortizes its cost over period of time - looking at EPS won’t give a clue about the right valuations. After lot of thinking to me right way to value this business should be Free Cash Flows generated after adjusting for acquisition cost of content.

In latest concall Jyoti said eros generated free cash flows of 132 cr. for 9 months ending december 2015. If we annualize it will be in region of 200 crores. Applying 10% yield- we can give valuation of 2000 crores for the business as a whole on conservative basis.

Management should make a conscious effort to generated FCF continuously otherwise this business won’t ever command good valuations

Eros International Media held conference call to discuss the results for quarter ended March 2016. The key takeaways of the call are as follows:

Highlights of the Call:

The company for Q4 FY16 has reported 40% decline in consolidated net sales to Rs 269.91crore. The resultant PAT decreased by 37% to Rs 32.72 crore.

The Company released 12 films during the quarter. In Q4 FY16, 6 medium & 6 low budget films were released as against 1 high budget, 4 medium & 17 low budget movies in Q4 FY15. Theatrical revenues during the quarter were driven by releases such as Dictator (Telugu), Rajini Murugan (Tamil), Guru (Marathi), Sanam Teri Kasam (Hindi), Aligarh (Hindi), Phuntroo (Marathi), amongst other releases. Revenues from the satellite segment further contributed to the financial performance during the quarter

During the quarter, 12 films were released consisting of 3 Hindi and 5 Tamil/Telugu films and 4 Regional film as compared to 22 films during Q4 FY2015, which included 17 Hindi and 5 Tamil/Telugu films

The company for FY16 has reported 11% incline in consolidated net sales to Rs 1582.68 crore. The resultant PAT decreased by 13% to Rs 214.15 crore.

Profitability was marginally impacted by holding back of high-margin catalogue revenues in the second half of the year to focus on working capital efficiencies and due to the postponement of some Q4 releases to FY 2017.

Revenue for FY16 saw a significant growth on account of global releases of Bajrangi Bhaijaan, Bajirao Mastani, TanuWeds Manu Returns, Welcome Back, Srimanthudu amongst others, across theatrical, overseas and satellite revenues, and overseas releases of Dil Dhadakne Do, Singh is Bling and Gabbar is Back reinforcing the portfolio and film mix strategy. In FY16, 6 high budget, 16 medium and 41 low budget films were released in as against 6 high budget, 11 medium and 47 low budget movies in FY2015. In FY16, 63 films were released consisting of 33 Hindi and 30 Regional films as compared to 64 films during FY2015, which included 45 Hindi and 19 regional films

Revenue breakup FY16 - Theatrical revenue was 44%, television & others was 30% and overseas revenue was 26% as a percentage of total income.

For the period ending March 31, 2016, the company generated healthy free cash flow of Rs 300 crore as compared to negative Rs (5) crore in FY2015. This demonstrates the working capital efficiencies the company was able to effect

As on March 31, 2016, the Net Debt of the company reduced by Rs 206.6 crore to Rs 107.2 crore from Rs 313.8 crore as on March 31, 2015 and the Net Debt/Equity ratio improved to 0.06 as compared to 0.21 as on March 31, 2015

As on March 31, 2016, total receivables stood at Rs 428.2 crore as compared to Rs 525.7 crore as on 31st March, 2015. In terms of DSO days, the receivables improved to 97.5 days on March 31, 2016 as compared to 133 days on March 31, 2015. This is a significant improvement from the management guidance given earlier to bring the overall receivables down to Rs 525 crore by the end of FY2016

Based on a detailed transfer pricing study by a Big 4 Accounting firm, the following changes will be made to the existing relationship agreement between Eros International Media (EIML) and Eros International Plc. EIML will transfer the overseas rights including global digital media rights to Eros International Plc, or it subsidiaries at an amount equal to 40% of the Production Cost of each Film with an additional mark-up of 20%. So out of every Rs 100 invested in content, EIML or its subsidiaries will de-risk itself to the extent of Rs 48 as compared to the Rs 39 from the previous arrangement. Additionally, Eros India group will hold an equity stake of 10-15% of the global digital business structure. This will allow it to participate in the long term value creation of the ErosNow business, any future value enhancement, stake divestment, IPO etc. These arrangements are now board-approved and will go through regulatory and other compliances to be implemented.

Lot of analysts have shown displeasure on the ErosNow business transferring to Eros Plc and getting small equity stake. Questions were also raised how the valuation was done.

Trinity will be collaborating with China Film Group to coproduce two films which will be and shot in both languages to simultaneously address the world’s second largest film market, China. The first Indo-China co-production will be directed by Kabir Khan with a distinguished cast from India and China. A film by Siddharth Anand which will explore a fresh take on the spy genre in India, a global favourite with franchise potential. A bilingual project from multiple award winning Tamil director, Prabhu Solomon. A Hindi and Tamil film co-written by Shridhar Raghavan, Dheeraj Rattan and K. Subhash and directed by Telugu director, Krish and Amole Gupte’s (director of Taare Zameen Par) kids action film

Indo- china first film will come in FY18. Similar type of co-production deals may happen with Korea and Taiwan

Content capex for FY17 will be around Rs 1100 – 1200 crore

Positive cash flow at PLC level achieved.

Catalog contribution to total revenue was 15% in FY16. It is expected to be 20% in FY17 and 25% in FY18 .

Catalog business was impacted as the company used to record the revenue from sale of catalog iin that particular quarter when deal is down while payments used to come later which resulted in rise in receivables. To bring the receivables down, the company is now making multiple short deal in a year, which will help receivables to come down. This will impact the catalog revenue as deal will be multiple type. As such, in short term, catalog revenue will impact

Hello vishnu

How do u rate the business of eros as of now. To me as i shared in my few posts above:

Eros has an enviable position in industry with 3000 titles. Its dominant position can be known by the fact that bajirao released with SRK dilwale. Movie making business has of late become an easy business with strong tailwinds blowing like never before in form of increase disposable incomes, increasing need for entertainment, various ways of monetisation ( eros mostly gets its cost recovered before releasing, digitsation ( genuine and increasing subscription figures helping channels to buy quality content), eros dominant partnership with industry heavy weights. This is a big competitive advantage for eros where no one can just come and take their positon.

Of course, management quality doesn’t look to be top notch but modus operandi doesn’t suggest they are crooks.

Considering management has walked the talk post debacle and becoming FCF positive is good.

Please provide u r opinion

To be honest, i never tracked Eros so i cannot give a fair and knowledgeable opinion about the business.

Having said above, i believe people will continue to watch movies in cinema halls and multiplexes. Torrents, Filesharing and other portals have not caused a significant disruption in people’s preference to watch on the big screen, as is evidenced in developed countries.

Also agree with your assessment on the multiple ways of monetizing the content they own. My broadband provider, ACT which provides FTTH connectivity has a tie-up with Hungama/Yupp TV to provided 2000 movies and 200+ channels on a monthly subscription basis @99 Rupees/month.

Another example is the tie up between Shemaroo and Netflix.

So, there is an opportunity for Eros to tie-up with MSO’s to provide content.

Apologies, but that is the extent of my awareness of Eros.

I mean, whether Eros International Plc (listed on NYSE) owns EROS NOW or Eros International Media (listed in India) owns it. That’s the clarification I request.

It is still unclear. As per the last update from management, the majority ownership of EROS Now lies with Eros international plc and the Eros International Media (Indian entity) would be given a minority stake of about 10 percent or so. I remember that investors were unhappy with this structure to which the management responded that they want to merge both the international and indian entity in due course of time. But no timeline was given for this.

It is very unfair that Indian entity Eros international takes 100% of risk in production. Although it sells to US entity Eros PLC and gets back 40% of the cost, US entity eventually holds 90% of all IP and brand value of all their production for just 40% of the cost. This reduces Indian entity to a mere distributor with no long term benefit. US entity in the mean time is becoming a cash cow with all benefits of a huge collection of movies which is evident from Reliance agreeing to invest $1b. Very questionable management integrity and therefore deserves this low valuation.

OCF - investing cash flow is negative 610 crores over the last 10 years with a corresponding increase in borrowings while net profit shown during this period is 1559 crores with a current PE of only 5.

ROE consistently decreased over last 10 years from 51% to 13% now.

Why such huge variances and bad performance? Is it due to bad management specific to the company or are there some industry level adjustments that should be taken into account specific to the media industry? Can someone please advise?

Eros is a known case of corporate mis-governance. You can scan through entire thread to find articles which explain in great detail - the nature of mis-governance.

Was reading your views on eros. It really intresting that eros is below its book value and i see that eros worldwide is increasing its stake everyday since last month… kindly give your guidance to dig more